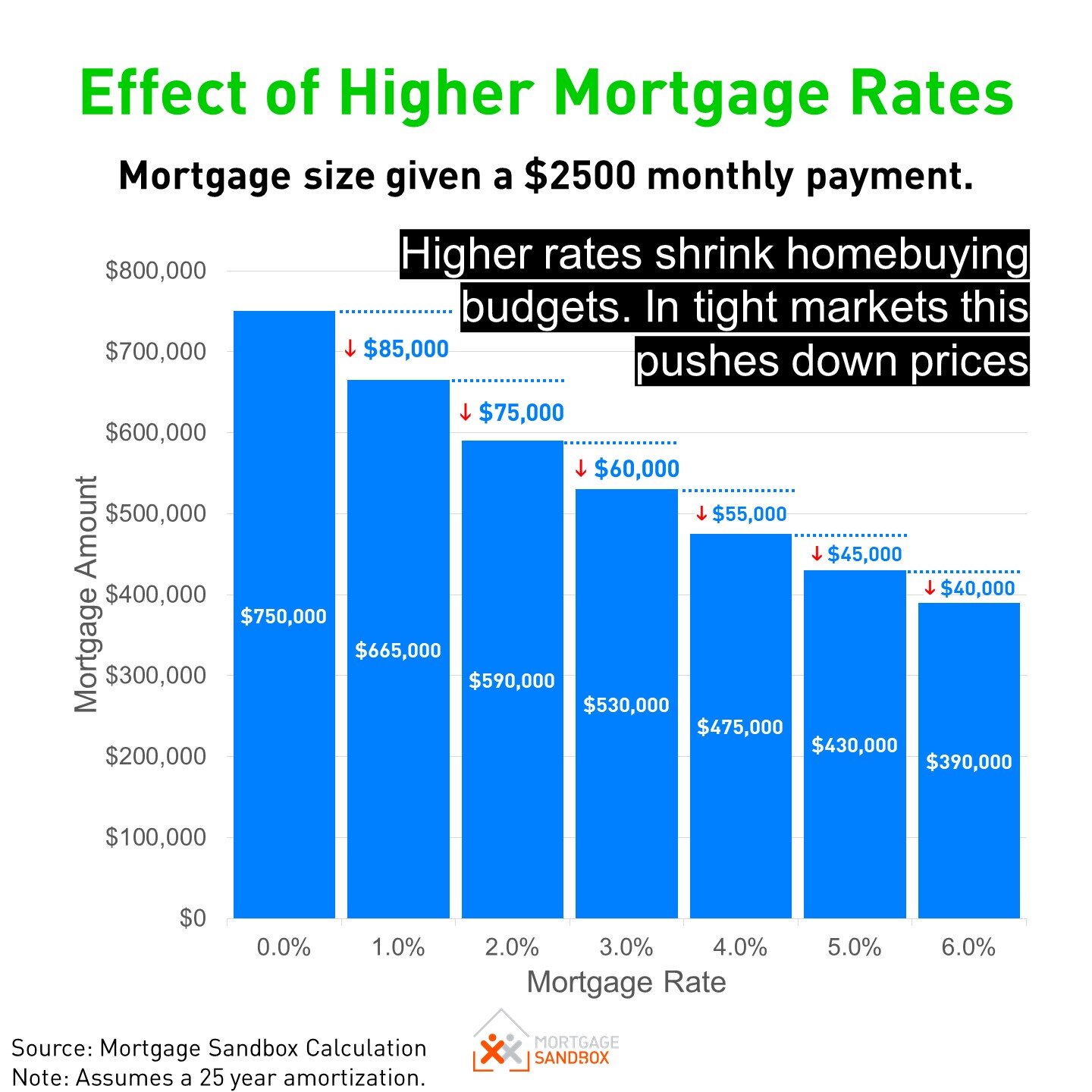

Honestly, trying to figure out what's the mortgage interest rate today feels a bit like chasing a moving target in a windstorm. You check one site, it says one thing. You call a lender, and they give you something totally different.

As of Tuesday, January 13, 2026, the national average for a 30-year fixed mortgage is sitting right around 6.07% to 6.20%.

It’s a weird spot to be in. We’re finally seeing rates pull back from those terrifying 7% and 8% highs we dealt with over the last couple of years, but we aren't exactly back to the "free money" era of 3%. Mortgage News Daily just reported a slight tick up this morning—about 0.06%—putting the daily index at 6.07%. Meanwhile, Bankrate's survey of larger lenders has the average closer to 6.20%.

Why the gap? Because "the rate" doesn't actually exist. There is only your rate.

The Reality of the 6% Threshold

For a long time, 6% was the psychological "line in the sand" for home buyers. We finally crossed under it briefly last week—hitting about 5.99% for a hot minute on Friday—but the market snatched it back. Today, lenders are being cautious.

📖 Related: Adam Neumann and the WeWork Crash: What Really Happened

This morning's inflation report showed the Consumer Price Index (CPI) holding steady at 2.7%. That’s not exactly the "mission accomplished" signal the Federal Reserve wanted. Because inflation is still acting "sticky," as economists like to say, the Fed is likely to pause its rate-cutting streak at the meeting on January 28.

When the Fed hesitates, mortgage bonds get twitchy. When bonds get twitchy, your interest rate goes up.

Breaking Down Today's Averages

If you're looking at different loan types, the numbers vary quite a bit. Here is how the land lies today, January 13:

- 30-Year Fixed: 6.07% (Daily Index) / 6.20% (Bankrate National Average)

- 15-Year Fixed: 5.59%

- 30-Year FHA: 5.75%

- 30-Year VA: 5.77%

- 30-Year Jumbo: 6.35%

Jumbo loans are still carrying a premium because banks are being stingier with those massive $750k+ balances. On the flip side, VA and FHA loans remain the "hidden gem" of the market. If you have military eligibility, you’re looking at rates nearly half a percent lower than a conventional loan. That’s massive. Over 30 years, that’s the difference between a new car and a much smaller retirement fund.

What Most People Get Wrong About "Today's Rate"

You see a headline saying rates are 6.07% and you think, "Great, I'll take that." Then you get your Loan Estimate and it says 6.45%.

You feel lied to. You weren't.

Those national averages are based on a "perfect" borrower. We're talking a 740+ credit score, a 20% down payment, and a single-family home that isn't a condo. If your credit score is 680, you’re likely looking at a "hit" to your rate. If you're putting 3% or 5% down, you're paying for that risk.

Also, points. Be careful with those. Many of the lowest rates you see advertised online include "discount points." Basically, you're paying thousands of dollars upfront to "buy" a lower rate. Sometimes it makes sense; usually, it doesn't, especially if you plan on refinancing in two years when rates (hopefully) drop further.

The "Powell vs. Politics" Drama

There is some extra-credit weirdness happening in the market right now. Federal Reserve Chair Jerome Powell is currently in a bit of a public spat with the Department of Justice and the current administration.

The market hates drama.

When there is political uncertainty regarding the independence of the Central Bank, investors demand a higher yield on mortgage-backed securities. This "risk premium" is keeping mortgage rates about 0.5% higher than they "should" be based on historical spreads against the 10-year Treasury yield.

Basically, you're paying a "chaos tax" on your mortgage right now.

Is the 5% Mortgage Coming Back?

Fannie Mae and the Mortgage Bankers Association have been duking it out with their forecasts for the rest of 2026. Fannie Mae is optimistic, predicting we might see 5.9% by the end of the year. The MBA is a bit more conservative, eyeing 6.4%.

Honestly? Don't bet the house on 5%.

The 10-year Treasury yield is the real North Star for mortgage rates, and it's been hovering around 4% for a while. Unless we see a significant recession or a total collapse in employment—neither of which seem to be happening according to today's data—rates are likely to stay in this 6% range for the foreseeable future.

Actionable Steps for Today's Market

If you are actively shopping or even just thinking about it, here is what you actually need to do instead of just refreshing a rate chart.

1. Get a "Live" Quote, Not a "Teaser" Quote

Call a local broker and a big bank. Give them your actual credit score and down payment amount. A national average doesn't pay your mortgage; your specific quote does.

👉 See also: Average Salary in the US: What Most People Get Wrong

2. Watch the 10-Year Treasury

If you see the 10-year Treasury yield (you can find this on any finance site) drop toward 3.8%, call your lender immediately to lock. If it's climbing toward 4.2%, your window for a lower rate is closing.

3. Ignore the "Wait for 5%" Advice

If you find a house you love today, and you can afford the payment at 6.1%, buy it. If rates drop to 5% next year, you refinance. If they go back to 7%, you’ll look like a genius for locking in now. You can't refinance your purchase price, but you can always refinance your rate.

4. Check Your "LLPAs"

Ask your lender about Loan Level Price Adjustments. These are the specific "surcharges" added to your rate based on your specific profile. Sometimes, raising your credit score by just 10 points can move you into a different bracket and shave 0.25% off your rate instantly.

Rates are volatile right now. We've seen them move a full quarter-point in a single afternoon. Today's 6.07% is a decent entry point compared to last year, but in this economy, "today's rate" is only as good as the moment you hit the "lock" button.