Honestly, if you looked at the stock market yesterday, you’d think the sky was falling. The Nasdaq tanked 1% and the S&P 500 wasn't far behind. But then you look at the actual u.s. economic data today and things start to feel a bit... weird. It’s like the numbers are telling one story—one of a resilient, spending-happy public—while the headlines are screaming about subpoenas and government shutdowns.

The disconnect is wild.

We just got a fresh batch of numbers, mostly playing catch-up because of that messy 43-day government shutdown that finally wrapped up late last year. The big news? People are still buying stuff. A lot of stuff. Retail sales for November (yeah, the data is still lagging) jumped 0.6%. That’s way higher than the 0.4% most of the "smart money" on Wall Street expected.

💡 You might also like: What Do Ratios Mean? Why Most People Misunderstand These Simple Numbers

What the Numbers are Actually Saying

Basically, the American consumer is carrying the entire economy on their back right now. It's not just "needs" either. While gasoline station sales rose 1.4%, people were out there hitting the sporting goods stores (up 1.9%) and miscellaneous retailers like florists and gift shops (up 1.7%).

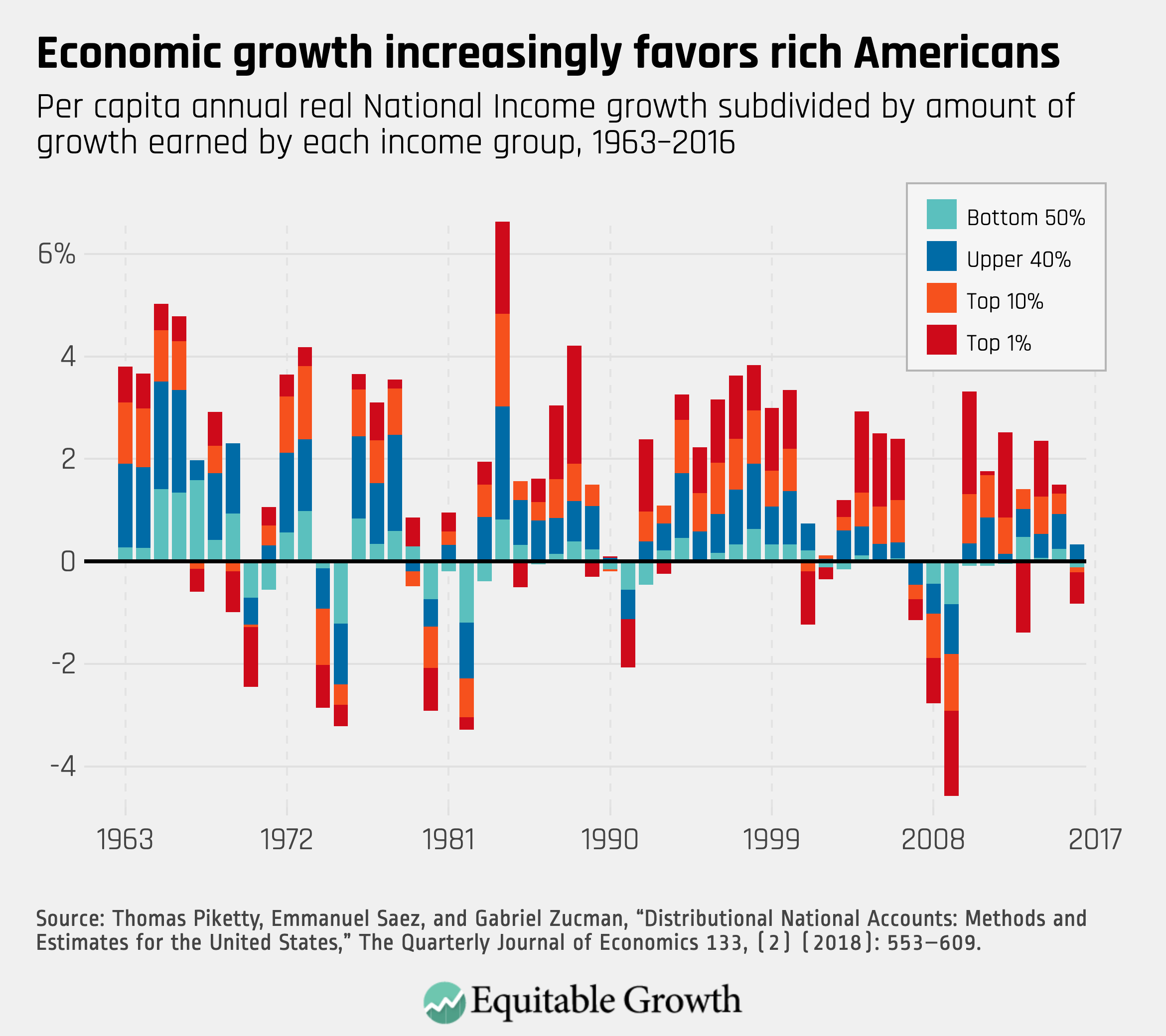

But here is the catch. This isn't a "everyone is winning" situation. If you dig into the recent commentary from the Dallas Fed, they pointed out something kind of depressing: the top 20% of earners are now responsible for roughly 57% of all consumer spending. The bottom 80%? They are mostly just trying to keep the lights on and the tank full.

The u.s. economic data today and the Fed's "Shadow" Problem

You can't talk about the data without talking about the drama at the Federal Reserve. Usually, we're just dissecting Jerome Powell’s comma placement in a speech. Now? The Department of Justice is serving subpoenas.

On January 11, Powell dropped a bombshell, confirming the DOJ is looking into his testimony from last June regarding some office building renovations. It sounds like boring bureaucracy, but the timing is suspicious to anyone with a pulse. There is a lot of chatter that this is just political pressure to force interest rates down faster than the Fed wants to go.

- The CPI Reality: December’s inflation came in at 2.7% year-over-year.

- The PPI Twist: Wholesale prices (Producer Price Index) rose 0.2% in November.

- Wage Growth: Real private sector earnings are on track to rise 4% this year.

Technically, the "inflation crisis" that dominated 2024 and 2025 looks like it’s cooling off. The White House is already taking victory laps, claiming the headline inflation is down to 2.4% under the current administration compared to the 3% they inherited. But if you’re at the grocery store today, you know "cooling" doesn't mean "cheaper." It just means the prices aren't jumping quite as fast as they were last Tuesday.

Is a Recession Still on the Table?

It depends on who you ask. The "Index of Economic Activity" from the Census Bureau is sitting at -0.43. In plain English: things are slightly contracting. We’re in this weird limbo where the labor market is "tight but tired."

Job openings fell to 7.1 million at the end of November. That’s a drop of about 4.1%. Usually, that’s a bad sign, but in this upside-down world, the Federal Reserve actually wants to see that. They want the labor market to chill out so they have an excuse to keep cutting rates.

The biggest job losses were in retail (-25,000) and construction (-11,000). If you’re looking for work, your best bet is still health care or professional services—those sectors are still screaming for people.

The "Catch-Up" Calendar

Because of the shutdown, the Bureau of Labor Statistics and the Census Bureau are working overtime. We are getting data dumps that feel like drinking from a fire hose.

| Data Point | Latest Reading (Nov/Dec 2025) | Market Expectation |

|---|---|---|

| Retail Sales (MoM) | +0.6% | +0.4% |

| Core PPI (MoM) | +0.3% | +0.2% |

| Unemployment Rate | 4.6% | 4.5% |

| Gold Price | $4,635/oz | N/A |

See that gold price? That’s the real "fear gauge." When gold hits $4,600 and silver crosses $90, it means investors don't trust the paper in their wallets or the people running the banks. They’re hedging against the very volatility the u.s. economic data today is trying to smooth over.

What Most People Get Wrong About This Data

Most folks see a "positive" retail report and think the economy is booming. Honestly, it might just be the "Tariff Front-Run."

Back in October and November, there was a huge rush to buy furniture and electronics before new trade tariffs kicked in. Furniture sales spiked nearly 2% right before the mid-October deadline. So, part of this "strong" data is just people panic-buying to avoid paying 20% more next month. It’s a sugar high, not a healthy diet.

Actionable Insights: How to Play This

If you’re trying to manage your own money in this mess, "wait and see" is a valid strategy, but here are some specific moves based on what the data is actually telling us:

- Watch the 10-Year Treasury: It’s hovering around 4.15%. If this drops further, mortgage rates might finally give us a breather. If you’re looking to refi or buy, keep a daily eye on this, not just the "news."

- Ignore the "Headline" Inflation: Focus on the "Control Group" retail sales. This is the stuff that actually goes into GDP. It rose 0.4% in November. It means the economy is growing at about 3.4%—way faster than a "recession" would suggest.

- Check Your Withholdings: With the 2025 tax cut expansions hitting paychecks now, you’ll likely see a bit more take-home pay in early 2026. Don't spend it all on those 10.5% higher gasoline prices.

- Prepare for a Fed Pause: Everyone expects rate cuts, but with the DOJ drama and "resilient" spending, the Fed might just sit on their hands for the first half of 2026. Don't bank on cheap credit returning by Easter.

The u.s. economic data today shows an economy that is fundamentally split. You have a wealthy tier that is spending like there’s no tomorrow, a middle class that is front-running tariffs, and a government that is essentially auditing itself while trying to keep the lights on. It’s messy, it’s noisy, but it’s not a collapse—yet.

Keep your eye on the January 30th PPI release. That will be the first real look at how much those new tariffs are actually bleeding into the prices we pay. Until then, keep your hedges tight and your spending intentional.

Next Steps for Your Portfolio:

- Review your exposure to consumer staples versus discretionary spending; the "top 20%" spending trend favors luxury and services over general retail.

- Monitor the U.S. Dollar Index (DXY); if it stays near 1.16 against the Euro, import costs will remain a major headwind for domestic manufacturing.

- Check the February 12th CPI release schedule to see if the "cooling" trend holds after the holiday spending spree.