Medicare is confusing. Honestly, it’s a mess of alphabet soup that makes most people want to close their laptops and hope for the best. But if you’re approaching 65, or helping a parent navigate the system, ignoring the nuances of Medicare Part A B C D is a recipe for massive, unexpected medical bills. People think it’s just "government insurance." It’s not. It’s a fragmented collection of different funding streams, private contracts, and strict deadlines that can haunt your bank account for decades if you miss them.

Let’s get the basics out of the way. Medicare isn’t free. Even the "premium-free" stuff has costs.

The Hospital Safety Net: Understanding Part A

Medicare Part A is basically your "room and board" insurance. If you’re admitted to a hospital, Part A covers the bed, the nursing care, and those tiny cups of lukewarm Jell-O. Most people don’t pay a monthly premium for this because they spent at least ten years paying into the system through payroll taxes.

It’s simple, right? Wrong.

The biggest trap in Part A is "Observation Status." You could spend three nights in a hospital bed, talking to doctors and getting treatment, but if the hospital classifies you as being there for "observation" rather than "inpatient admission," Part A won't pay for your subsequent skilled nursing facility stay. This catches thousands of seniors off guard every year. You have to ask the staff specifically: "Am I an inpatient?"

Also, the deductible is per "benefit period," not per year. If you go to the hospital in January, pay your deductible (which is $1,676 in 2024), go home, and then get sick again 61 days later, you owe that deductible all over again. It’s brutal.

Medicare Part B: The Doctors and the "Penalty"

If Part A is the building, Medicare Part B is everything that happens inside it—and outside of it. We’re talking doctor visits, outpatient surgeries, lab tests, and even some preventive vaccines.

Unlike Part A, everyone pays a premium for Part B. In 2024, the standard monthly premium is $174.70, though if you’re a high-earner, the Social Security Administration will hit you with an IRMAA (Income Related Monthly Adjustment Amount) surcharge.

👉 See also: Apple cider vinegar for fat loss: What the science actually says vs the TikTok hype

Whatever you do, don't miss the enrollment window.

If you don't sign up for Part B when you’re first eligible (and you don't have "creditable" coverage from a current employer), you’ll face a 10% penalty for every 12-month period you waited. That penalty stays with you for the rest of your life. It never goes away. It’s a permanent tax on your retirement for a simple paperwork mistake.

Part B also only covers 80% of costs. There is no "out-of-pocket maximum." If you have a $100,000 heart procedure and only have Part B, you are personally on the hook for $20,000. This is why people buy Medigap or look into Part C.

The Medicare Part C Pivot: Is Advantage Actually Better?

Medicare Part C, commonly known as Medicare Advantage, is where things get controversial. These are private plans—think UnitedHealthcare, Humana, or Aetna—that contract with the government to provide your Part A and B benefits.

They often bundle in drug coverage (Part D) and extra perks like dental, vision, or gym memberships (SilverSneakers).

💡 You might also like: Pictures of Rotator Cuff: What You're Actually Seeing on Your MRI and Why It Matters

The pitch is great: "$0 premiums!"

But there’s a catch. Or three.

- Networks: In Original Medicare, you can see any doctor in the country who accepts Medicare. In Part C, you’re usually stuck in a local HMO or PPO network.

- Prior Authorization: Private insurers want to save money. You might need your insurer’s "okay" before getting that MRI your doctor ordered.

- The One-Way Door: In many states, if you choose Medicare Advantage and want to switch back to Original Medicare later, Medigap insurers can deny you coverage for pre-existing conditions. You’re essentially locked in.

It’s a trade-off. You get lower upfront costs and extra perks in exchange for less freedom and more administrative hurdles. For some, it’s a lifesaver. For others, it’s a bureaucratic nightmare when they get seriously ill.

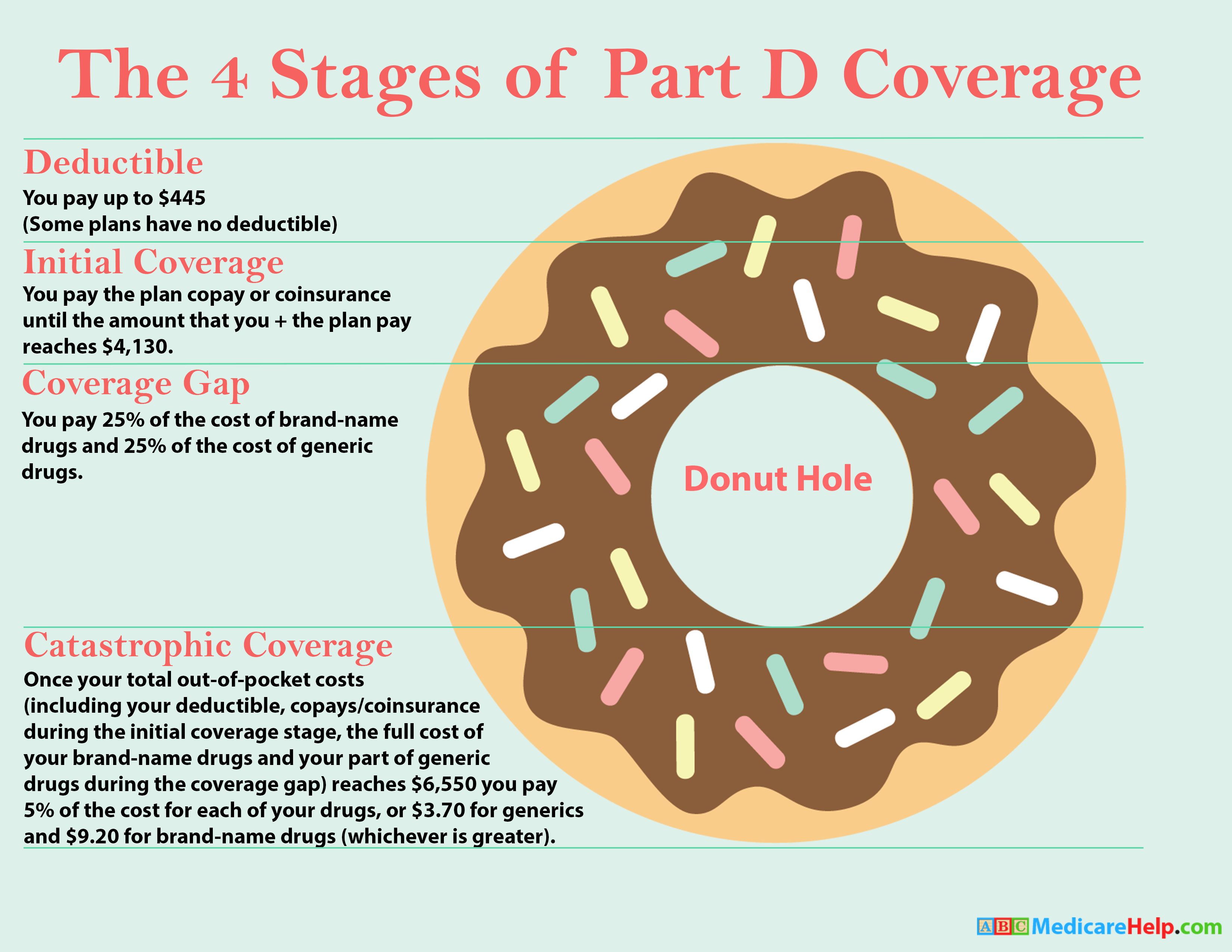

Medicare Part D: The Pharmacy Maze

Then there’s the drugs. Part D is strictly for prescription medication. Even if you don't take any pills right now, you should probably buy a cheap "placeholder" plan. Why? Because like Part B, there’s a late-enrollment penalty for Part D that lasts forever.

Drug plans change their "formularies" (the list of covered drugs) every single year. A medication that cost you $20 a month in December could jump to $200 in January because the insurer moved it to a different "tier."

The "Donut Hole" used to be a massive problem, but recent legislation like the Inflation Reduction Act is finally capping out-of-pocket drug costs. By 2025, there will be a $2,000 cap on what you pay for prescriptions. This is a massive win for seniors on high-cost specialty meds.

How to Actually Choose Without Losing Your Mind

You basically have two paths when navigating Medicare Part A B C D.

Path A: The "Traditional" Route

You take Part A and Part B. You add a standalone Part D plan for drugs. Then, you buy a Medigap (Medicare Supplement) policy. This is the most expensive monthly option, but it gives you the most freedom. You can go to any specialist in the U.S. and your out-of-pocket costs are almost zero.

Path B: The "All-in-One" Route

You sign up for a Medicare Advantage (Part C) plan. It covers everything. Your monthly premium is often $0 (besides your Part B premium). It’s convenient, but you have to stay in-network and deal with insurance company approvals.

Common Mistakes to Avoid Right Now

Don’t assume your employer coverage is "creditable." Check with your HR department. If your company has fewer than 20 employees, Medicare usually becomes the primary payer at age 65, and if you don't sign up for Part B, your work insurance might refuse to pay their portion of the bill.

Stop listening to celebrity commercials on TV. Joe Namath doesn't know your specific medical history or which zip code has the best networks. Those "free money back in your Social Security check" ads often refer to very specific "Giveback" benefits that are only available in certain areas or for people with specific income levels.

Actionable Steps for Your Enrollment

- Check your "My Medicare" account: Create one at Medicare.gov. It’s the only way to see your actual claims and coverage in real-time.

- Verify your doctors: If you’re considering Part C, call your doctor’s office directly and ask: "Are you in-network for this specific Medicare Advantage plan?" Don't rely on the insurance company's online directory; they are notoriously outdated.

- Audit your prescriptions: Every October during Open Enrollment, run your drug list through the Medicare Plan Finder tool. Plans change their pricing so often that loyalty to a specific insurance company usually costs you money.

- Look at Medigap Plan G: If you want the best coverage under Original Medicare, Plan G is currently the gold standard for new enrollees. It covers everything Part A and B don't, except for the small Part B annual deductible.

- Watch the calendar: Your Initial Enrollment Period is a 7-month window (3 months before your 65th birthday, your birthday month, and 3 months after). Mark it in red.

The system isn't designed to be easy; it's designed to be a partnership between you and the federal government. Take the time to read the "Medicare & You" handbook they mail out every year. It’s dry, it’s boring, but it’s the only source of truth in a sea of insurance marketing.