You’re staring at two government cards in your hand, or maybe you’re just trying to help your parents sort through a mountain of mail that looks like it was written by a lawyer who hates clarity. One says Medicare. The other says Medicaid. They sound like twins, they’re both funded by your tax dollars, and honestly, even the people working at the hospital get them mixed up sometimes.

But here’s the thing: they aren’t the same. Not even close.

If you mess up the distinction, you could end up paying thousands for a nursing home stay you thought was covered, or worse, missing out on "Extra Help" that could put two hundred bucks back in your pocket every single month. Let’s break down the actual, boots-on-the-ground reality of how these programs work in 2026.

Medicare: The "I’ve Worked for This" Program

Think of Medicare as the health insurance you "earn" through years of payroll taxes. It’s a federal program, which means the rules are pretty much the same whether you live in the snowy woods of Maine or the deserts of Arizona.

Who gets it?

Mainly, it’s for the 65-and-older crowd. You’re in regardless of whether you’re a millionaire or barely scraping by. However, younger folks with specific disabilities or conditions like ALS and End-Stage Renal Disease (ESRD) can get in too.

👉 See also: Magnesio: Para qué sirve y cómo se toma sin tirar el dinero

The 2026 Price Tag

Medicare isn’t free. It’s a common myth. Most people don’t pay for Part A (hospital stays) because they worked for at least 10 years. But for Part B (doctors and outpatient care), you’re looking at a standard monthly premium of $202.90 in 2026. If you’re high-income, that number can jump way higher due to something called IRMAA.

Medicaid: The "Safety Net" Program

Medicaid is the "assistance" side of the coin. It’s meant for people with limited income and resources. Unlike Medicare, this is a joint venture between the federal government and your specific state.

Because states have a say, Medicaid is a bit of a "choose your own adventure" depending on your zip code.

The Eligibility Game

In 2026, most states that expanded Medicaid allow you to qualify if your income is below 138% of the Federal Poverty Level. For a single person, that’s roughly $1,800 a month in many areas. But it’s not just about income. It’s about "assets" too—things like savings accounts and stocks. If you have $50,000 in the bank, many states will tell you to "spend it down" before they’ll help you.

✨ Don't miss: Why Having Sex in Bed Naked Might Be the Best Health Hack You Aren't Using

The Big Coverage Gap Everyone Misses

People assume Medicare covers everything because it’s "the" senior insurance. It doesn't.

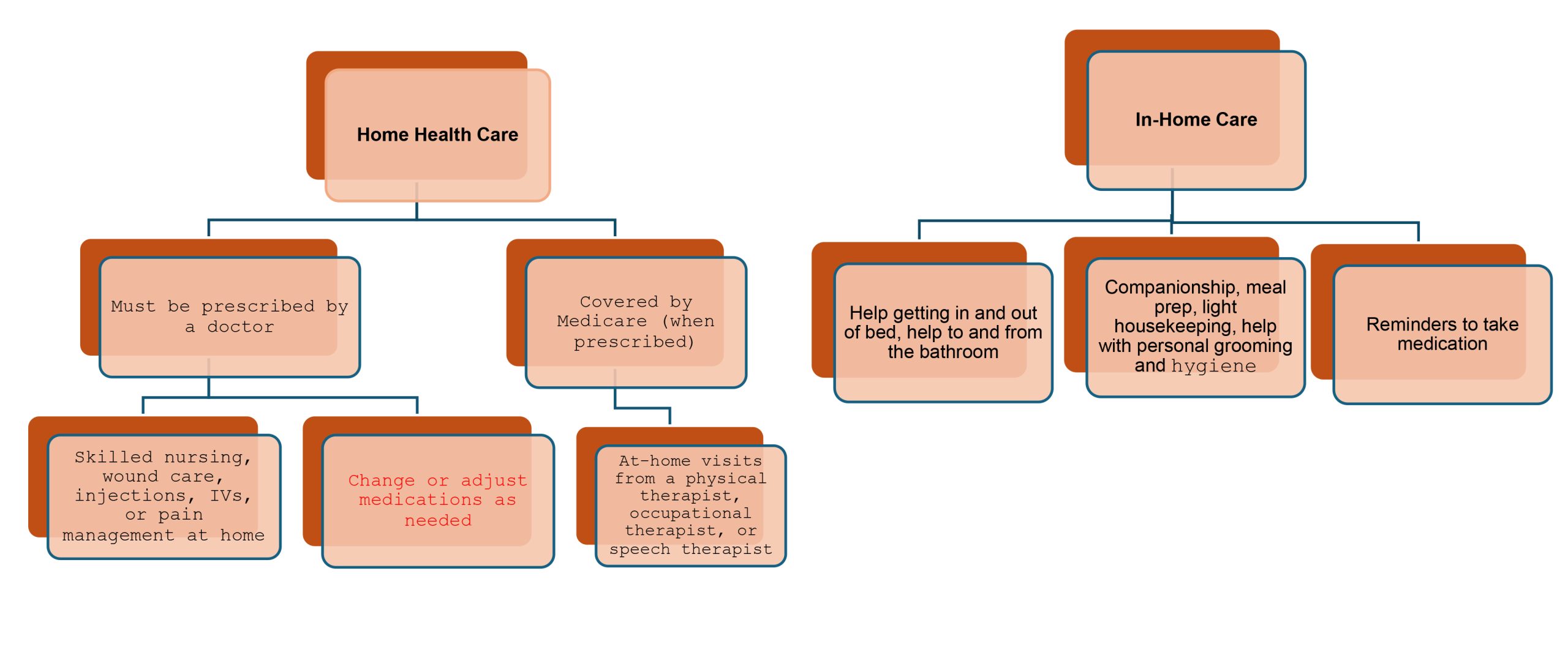

Medicare is great for a heart bypass or a broken hip. It is terrible for long-term care. If you need to stay in a nursing home for six months because you can’t walk or feed yourself, Medicare will stop paying after a short period (usually 100 days, and only if you’re "improving").

This is where Medicaid is the heavy lifter. Medicaid is the primary payer for long-term nursing home care in the U.S. It’s the reason people have to basically empty their savings accounts to qualify—once you’re broke, Medicaid steps in to pay the $8,000-a-month nursing home bill.

A Quick Reality Check on the Differences

- Administration: Medicare is Federal (one boss). Medicaid is State/Federal (many bosses).

- Cost: Medicare has premiums and 20% co-insurance. Medicaid is usually $0 or very low-cost.

- Eligibility: Medicare is based on age/disability. Medicaid is based on "need" (income/assets).

- Dental/Vision: Medicare is notoriously stingy here (unless you have a Part C Advantage plan). Medicaid often covers basics like exams and glasses, though it varies wildly by state.

The "Golden Ticket": Being Dually Eligible

Wait, can you have both? Yes. And it’s the best-case scenario for your wallet.

🔗 Read more: Why PMS Food Cravings Are So Intense and What You Can Actually Do About Them

About 13 million Americans are "dual eligible." This means they have Medicare as their primary insurance, and Medicaid acts as a "wrap-around" to pick up the slack.

If you’re dual eligible:

- Medicaid pays your $202.90 Medicare Part B premium. That’s an immediate raise in your Social Security check.

- You get "Extra Help" for drugs. This caps your prescription costs at just a few dollars.

- No more 20% bills. When Medicare pays its 80%, Medicaid usually covers the remaining 20%.

In 2026, many people use Dual Special Needs Plans (D-SNPs). These are private insurance plans that coordinate both sets of benefits into one card. Just be careful—as of this year, some of the "extra" perks like grocery credits are getting stricter. You often need a verified chronic condition (like diabetes or high blood pressure) to keep those monthly food allowances.

The 2026 Shift: What’s Changing Right Now?

You need to know that the "continuous enrollment" era from the pandemic is over. States are aggressively "unwinding" their Medicaid rolls. If you haven't checked your mail or updated your address with the state office, you might find your Medicaid canceled simply because they couldn't find you to verify your income.

Also, for the 2026 plan year, the Value-Based Insurance Design (VBID) program ended. This means some of those $0 copays on all drugs you might have seen in previous years are shifting. You’ll likely see small copays returning unless your plan specifically covers them through other means.

Actionable Steps to Take Today

Sorting this out shouldn't be a full-time job. Use these steps to figure out where you stand:

- Check your "Extra Help" Status: If your income is under $23,000 (roughly) as a single person, call Social Security and ask about the Low-Income Subsidy (LIS). Even if you don't qualify for full Medicaid, this can save you thousands on meds.

- The 5-Year Lookback: If you’re thinking about Medicaid for a nursing home in the future, remember the "lookback" rule. You can't just give your house to your kids today and qualify tomorrow. Medicaid looks at your financial transfers for the last five years.

- Update Your Info: Call your state’s Medicaid agency or log into their portal. Ensure they have your current phone number. If they send a renewal form and you don't return it, you lose coverage, period.

- Compare Part D Plans: Since Medicare Part D rules changed significantly for 2025 and 2026 (including the $2,000 out-of-pocket cap on drugs), your old plan might not be the best one anymore.

- Contact a SHIP Counselor: Every state has a State Health Insurance Assistance Program (SHIP). These are free, unbiased volunteers who don't sell insurance. They can look at your specific income and tell you if you're leaving Medicaid money on the table.