You’re standing at a Western Union counter or maybe a dusty post office desk. There is a line behind you. People are sighing. You have a small, flimsy piece of paper in your hand that represents $500 of your hard-earned rent money, and suddenly, you realize you have no idea which line is for what. If you mess this up, your landlord doesn't get paid, and you might be out the cash for weeks while you wait for a refund. It’s stressful. Honestly, it's one of those basic adulting tasks that nobody actually teaches you until you're forced to do it.

Learning how to complete a money order isn't just about filling in boxes; it's about protecting your cash. Unlike a personal check, this is "guaranteed" funds. You’ve already paid for it. If you lose it and it’s blank? Someone else just found a payday. If you fill it out wrong? Some banks won't even touch it.

💡 You might also like: 1170 Spring Street Elizabeth New Jersey: The Truth About This Industrial Hub

We’re going to walk through the specifics of the most common issuers—the USPS, Western Union, and MoneyGram—because they all look slightly different.

The Anatomy of the Document: Who Gets What?

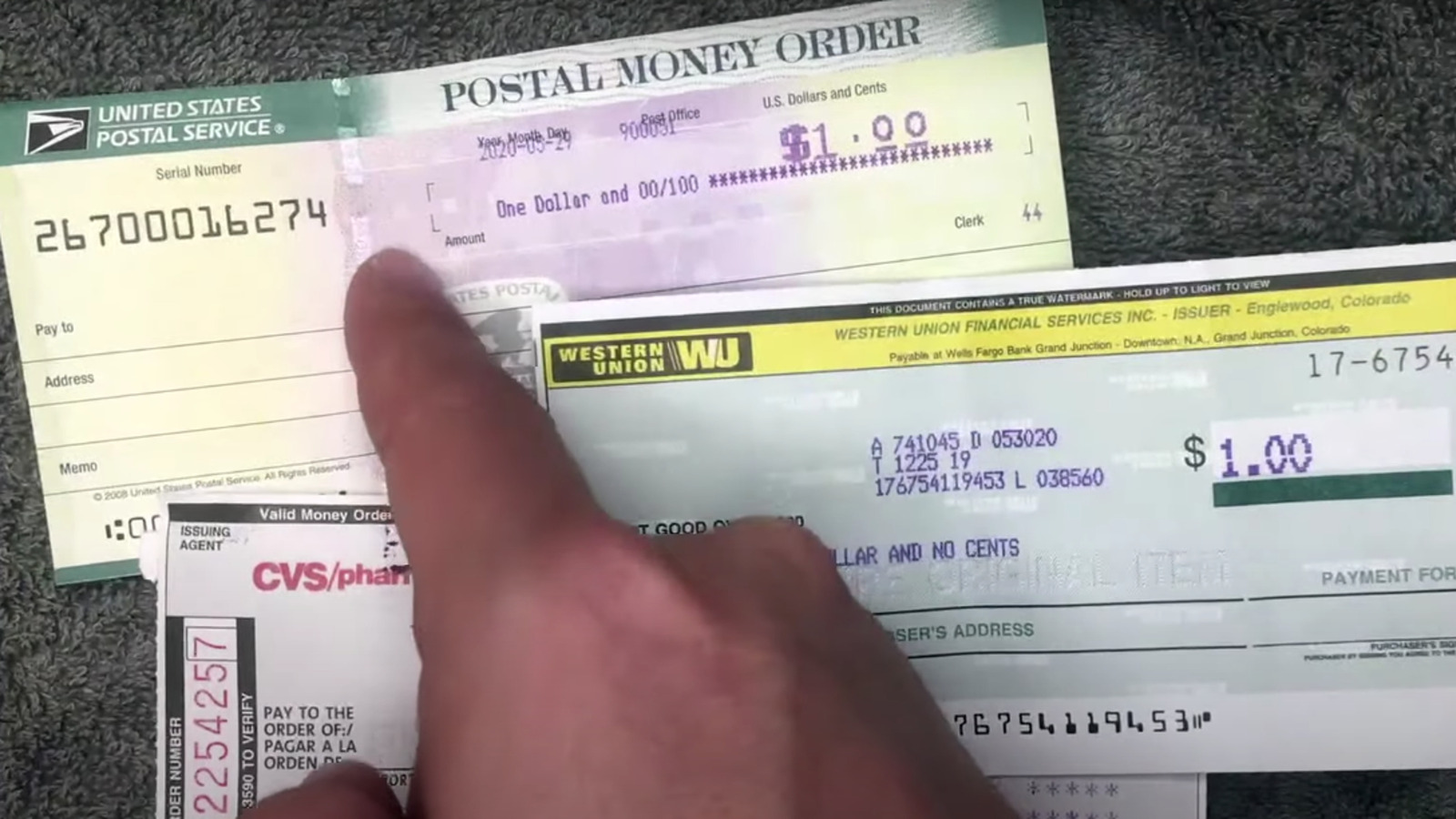

First thing’s first. Look at the paper. You’ll usually see a field labeled "Pay to the Order Of" or sometimes just "Pay To." This is where the name of the recipient goes. Don't leave this blank for even a second. Seriously. The moment you walk away from the register, that name should be on there. If you drop a blank money order on the sidewalk, anyone can write their own name in that slot and cash it at a grocery store or a check-cashing joint.

Then there’s the "Purchaser" or "From" section. That’s you. You are the purchaser.

Most people get confused by the address section. Do you put your address or theirs? Usually, the money order will ask for the "Purchaser’s Address." This is for the recipient’s records so they know where the payment came from, and it helps the issuer track the transaction if there is a dispute later. If it says "Recipient Address," well, that’s self-explanatory. But typically, they want yours.

The Western Union and MoneyGram Nuance

If you bought your money order at a CVS, 7-Eleven, or a Walmart, you’re likely holding a Western Union or MoneyGram document. They are thinner than the ones from the post office.

On a Western Union note, you might see a line for "Memo" or "Account Number." If you’re paying a utility bill or rent, put your account number or "Rent for Unit 4B" here. It’s a tiny bit of extra insurance. It tells the person on the other end exactly why they are receiving this money.

✨ Don't miss: 150 Euros to US Dollars: What the Banks Aren't Telling You About the Exchange

Why Your Signature Matters (And Where It Goes)

This is where most mistakes happen. There is a spot on the front that says something like "Purchaser’s Signature." Sign it there. Do not sign the back.

The back of the money order is the "Endorsement" section. That is reserved strictly for the person or business receiving the money. If you sign the back, you have essentially "endorsed" it over to yourself or made it difficult for the recipient to deposit it into their bank account. I’ve seen people have to buy a whole new money order because they signed the wrong side and the bank teller refused to accept the "mutilated" document.

It’s an expensive mistake.

The Receipt: Your Only Lifeline

Every money order comes with a detachable stub or a carbon copy. This is your receipt. Treat it like a bar of gold.

If the money order gets lost in the mail—which happens more than we’d like to admit—you cannot get a refund without that receipt. The receipt has the serial number and the tracking number. Without it, the money is basically gone into the void.

📖 Related: Wait, What Exactly Is an Occupation Anyway?

Keep it until you are 100% certain the recipient has cashed the money order. I usually tell people to take a photo of it on their phone the second they finish writing. That way, if you lose the little slip of paper in your car or trash it by accident, you still have the numbers you need to start a claim.

Dealing with the US Postal Service (USPS)

The USPS money order is the "gold standard." It feels more like a real check. It’s got watermarks and security threads. If you hold it up to the light, you should see a repeat of the Benjamin Franklin watermark. If you don't see that, you might be looking at a counterfeit.

When you figure out how to complete a money order at the post office, you’ll notice the fields are very clearly labeled:

- Pay To: The person or business name.

- Address: The recipient's address goes here on the USPS version.

- Memo: What is this for?

- From: Your name.

- Address: Your address.

The USPS is stricter about IDs. If you're buying a large amount (over $3,000), you’re going to have to fill out a Form 8105-A. It’s a federal anti-money laundering thing. Don’t be weirded out by it; it’s standard procedure.

Common Blunders to Avoid

- Using a Pencil: Never. Ever. Use a dark ink pen. Gel pens are okay, but a standard ballpoint is best. You want something that "bites" into the paper so it can’t be erased or altered.

- Crossing Out Mistakes: If you misspell the landlord's name, don't just cross it out and initial it like you might on a personal check. Most places won't accept an altered money order. You'll likely have to take it back to where you bought it, pay a fee, and have them cancel it and issue a new one.

- Wait to Sign: Don't sign it until you're actually ready to fill out the rest. An "open" signed money order is just as dangerous as a blank one.

The Cost of Doing Business

Money orders aren't free.

The post office usually charges a couple of dollars. Walmart is often the cheapest, sometimes under $1.50. Banks are the most expensive; they might charge you $5 or $10 for a "Cashier's Check," which is similar but functionally different. If you’re trying to save a few bucks, the grocery store or a big-box retailer is your best bet.

Just keep in mind there are limits. Most money orders cap out at $1,000. If you need to pay $1,500 for rent, you’re going to have to buy two separate money orders and fill them both out completely. It's a pain, but that’s how the system is designed to prevent fraud.

Verifying the Funds

If you are on the receiving end of a money order, you need to be careful. Scams are everywhere. A common one involves someone giving you a money order for more than the amount they owe you and asking you to wire back the difference.

The money order looks real. You deposit it. Your bank might even make the funds available the next day. But a week later, the bank realizes the money order was fake. They take the money back out of your account, and you’re out whatever "change" you sent to the scammer.

Always verify. For USPS money orders, there is a dedicated phoneline (866-456-9126) where you can check the validity of the serial number. For Western Union, you can check the status online using the tracking number.

What to Do if Things Go Wrong

If you realize you’ve been scammed or you simply lost the document, act immediately.

Go back to the issuer with your receipt. You will have to fill out a cancellation request. There will be a fee—usually between $15 and $30—and it can take up to 60 days to get your money back. The issuer has to "search" their records to ensure the money order hasn't been cashed yet. If it has been cashed, you’re likely out of luck unless you want to involve the police and file a fraud report.

Actionable Steps for Your Next Payment

- Bring a Pen: Don't rely on the one chained to the counter that probably doesn't work. Use a permanent black ink pen.

- Fill it out immediately: Do not leave the store until the "Pay to the Order Of" and "Purchaser" lines are filled.

- Snap a Photo: Take a clear picture of the completed money order and the receipt together.

- Check the Limits: If your payment is over $1,000, calculate how many separate money orders you need so you aren't surprised by the total fees.

- Mail Securely: If you're mailing it, use a security envelope so people can't see the document through the paper. Even better, use a tracked mailing service if the amount is large.

Completing a money order is a bit of an old-school way to move money, but it remains one of the most reliable methods for people who don't use traditional banking or need to provide a guaranteed payment. Just take your time, write clearly, and never lose that receipt.