Money is weird. One day your Euro buys you a fancy dinner in Manhattan, and the next, you're looking at the menu wondering if you should have just stayed in Berlin. If you've ever stared at a flickering exchange board at an airport or refreshed a Google tab ten times while trying to book a flight, you know the feeling. Currency conversion euro to us dollar isn't just a math problem for bankers in suits; it’s a living, breathing pulse that dictates how much your life costs.

The exchange rate is basically the "price" of one money in terms of another. Think of it like a seesaw. When the Euro goes up, the Dollar goes down, and vice versa. But what actually moves that seesaw? It isn't just random luck.

📖 Related: Why 48 Hours to Buy Is the New Reality for High-Stakes Markets

Why the Euro and Dollar Keep Swapping Places

Central banks are the real puppet masters here. You've got the European Central Bank (ECB) in Frankfurt and the Federal Reserve in Washington D.C. They are constantly playing a game of chicken with interest rates.

When the Fed raises interest rates, the Dollar usually gets stronger. Why? Because investors want to put their money where they can earn more interest. It's like choosing a savings account that pays 5% over one that pays 2%. Simple. If the US economy looks "hotter" than the Eurozone, money flows across the Atlantic, and the Dollar climbs.

But then there's inflation. It's the silent killer of purchasing power. If prices in France and Italy are skyrocketing faster than prices in Ohio, the Euro might lose its luster. Investors get nervous. They sell. The rate drops.

Honestly, it’s a bit of a mess.

Geopolitics plays a massive role too. Remember when energy prices spiked because of the conflict in Ukraine? Europe, which relies heavily on imported gas, took a massive hit. The Euro tumbled because traders were scared the continent would freeze or go into a deep recession. During those times, the Dollar becomes a "safe haven." It's the financial equivalent of a sturdy bunker during a storm.

The Myth of "Zero Fee" Conversions

You see it everywhere. "No Commission!" "Zero Fees!"

✨ Don't miss: Median Wage United States: What Most People Get Wrong

It’s usually a lie.

Well, it’s a half-truth. While a kiosk or an app might not charge you a flat $5 fee, they make their money on the "spread." This is the gap between the market rate (what you see on XE or Reuters) and the rate they give you. If the actual currency conversion euro to us dollar rate is 1.10, but the bank gives you 1.07, they just pocketed 3 cents for every Euro you swapped.

That adds up fast.

On a $1,000 transaction, that’s $30 gone. Poof. Just for the privilege of clicking a button. If you are moving thousands for business or a home purchase, you are basically handing over a vacation's worth of cash to a middleman.

How to Win at the Exchange Game

If you're traveling, stop using the airport booths. Just stop. They have some of the worst rates on the planet because they have a captive audience. You're tired, you just landed, and you need taxi money. They know this. They pounce.

Instead, use a debit card with no foreign transaction fees. Neobanks like Revolving or Wise (formerly TransferWise) changed the game here. They use the mid-market rate. They are transparent about their small service fee. It's usually the cheapest way for a regular person to handle a currency conversion euro to us dollar.

✨ Don't miss: On the Scene Event Services Nashville: Why Your Party Logistics Are Probably Broken

For larger moves, like if you're an expat or buying property abroad, you need a currency broker. These guys specialize in "forward contracts." This allows you to lock in a rate today for a transfer you’re making in three months. If the Euro is strong today but you’re worried it’ll tank before your house closing in Spain, you lock it in. It's insurance for your bank account.

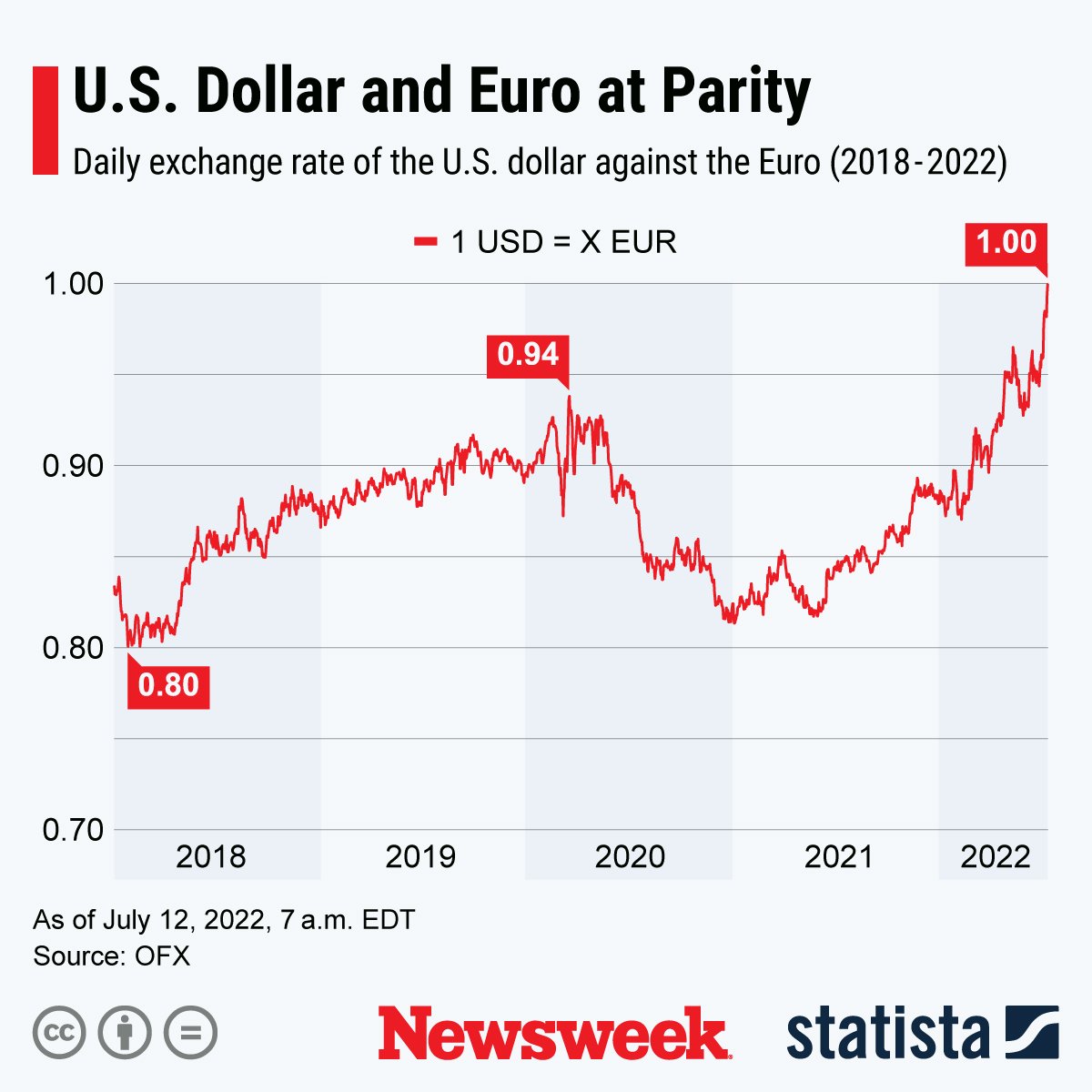

The Psychology of Parity

Every once in a while, the Euro and the Dollar hit "parity." That means 1 Euro equals 1 Dollar.

It’s a huge psychological milestone.

When parity happens, it makes headlines. It feels like the Euro is "failing" or the US is "winning." In reality, it’s just a number, but it changes how people spend. Americans flock to Europe because everything feels like it’s on a 20% discount. Europeans, meanwhile, cancel their trips to Disney World because suddenly a burger in Orlando costs a week's wages.

The Hidden Impact on Your Stocks

You might not even hold Euros, but this conversion rate still hits you if you own stocks.

Take a giant like Apple or Microsoft. They sell iPhones and software all over Europe. If the Dollar is super strong, those Euros they earn in Berlin are worth fewer Dollars when they bring them back to the US. This can actually make a company's earnings look "bad" even if they sold more products.

Investors call this "currency headwinds." It’s a fancy way of saying the exchange rate screwed them over. On the flip side, if you're a European company exporting cars to the US, a weak Euro is a gift. Your cars are suddenly cheaper for Americans to buy, so you sell more of them.

It is a never-ending cycle of winners and losers.

Real-World Strategy for 2026

The world has changed. Digital currencies and instant payment rails are making the old "3-day bank transfer" look like a relic of the Stone Age. But the fundamental math of the currency conversion euro to us dollar remains the same: it's a reflection of trust in two different economies.

If you are looking at the rates today, don't just look at the number. Look at the "Why."

- Is the Fed about to cut rates? (Dollar might weaken)

- Is the ECB worried about growth? (Euro might weaken)

- Is there a global crisis? (Dollar usually strengthens)

Don't try to time the market perfectly. You won't. Even the smartest quants on Wall Street get it wrong half the time. Instead, "ladder" your conversions. If you need to move $10,000, move $2,000 every week for five weeks. This averages out your cost and protects you from a sudden, nasty spike in the rate.

Actionable Steps for Your Next Conversion:

- Check the Mid-Market Rate: Use a neutral source like Reuters or Bloomberg to see what the "real" price is before you look at your bank's offer.

- Ditch the Traditional Banks: Unless you have a high-tier private banking account, your local branch is likely overcharging you by 3% or more.

- Watch the Economic Calendar: If the US Bureau of Labor Statistics is releasing jobs data on Friday, wait until after the news drops to convert. Markets are usually volatile right before big announcements.

- Use a Multi-Currency Account: If you deal with both currencies often, keep a balance in both. Don't convert unless you absolutely have to. This lets you wait for "strong" days to move your money.

- Verify the Small Print: Some "fee-free" cards actually have a limit on how much you can convert per month before they start hitting you with 1% or 2% surcharges.

The relationship between the Euro and the Dollar is the most important exchange rate in the world. It’s the bedrock of global trade. By understanding that it’s a price—and like any price, it can be shopped around for—you keep more of your money where it belongs. In your pocket.