Tax season is usually a headache, but the look back at the 2023 tax tables 1040 is particularly weird because of how inflation started messing with the math. You probably noticed it. Maybe your paycheck stayed the same, but your take-home pay drifted up just a tiny bit, or perhaps you realized that "standard deduction" everyone talks about suddenly jumped by a massive margin.

It wasn't an accident. The IRS doesn't usually move that fast, but for the 2023 tax year, they had to adjust the brackets by about 7% just to keep up with the cost of living. If they hadn't, millions of people would have been pushed into higher tax brackets without actually getting "richer" in real-world terms. That's a phenomenon called "bracket creep," and honestly, it’s a stealthy way for the government to take more of your money without passing a new law.

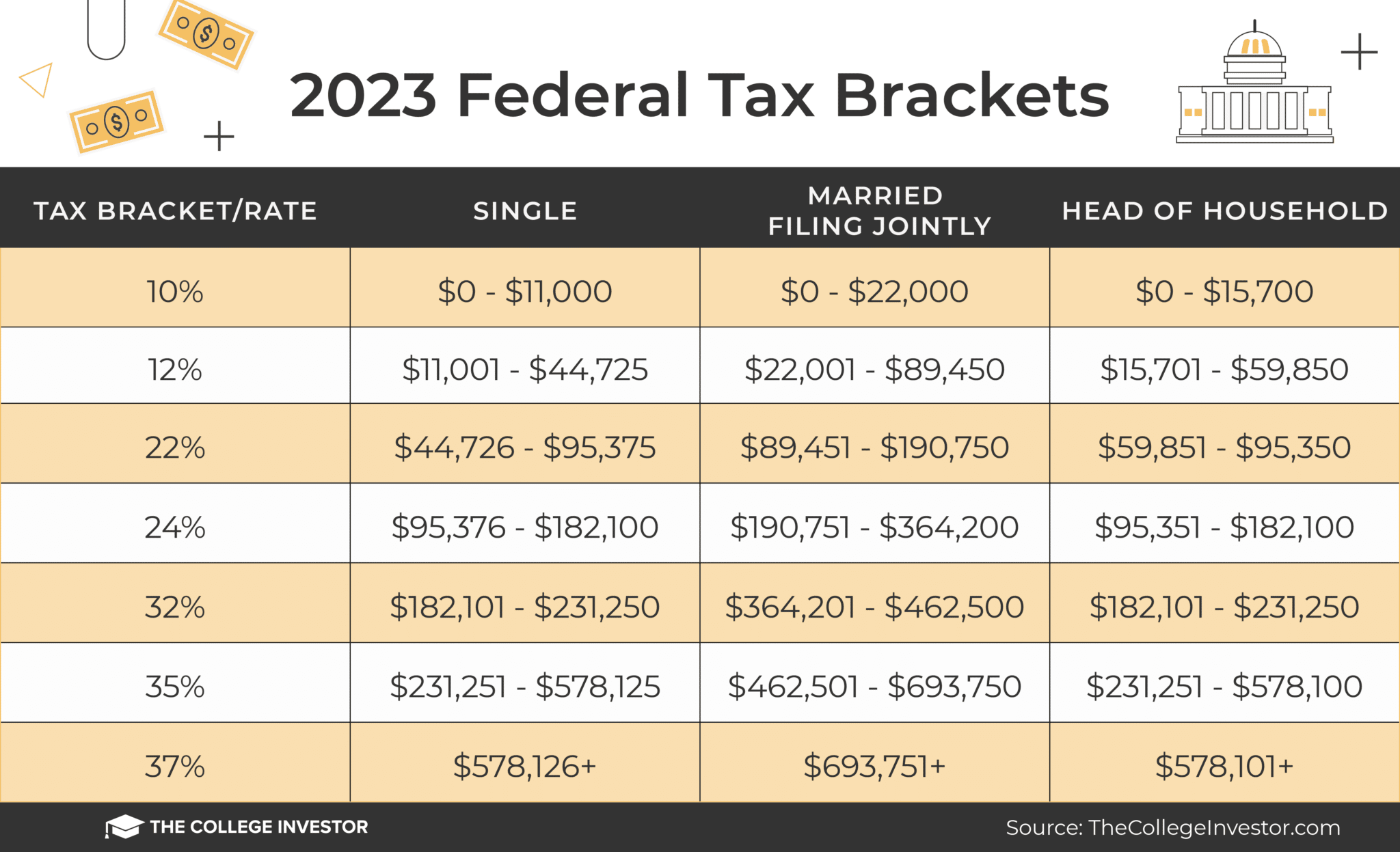

Understanding the 2023 tax tables 1040 and the Seven Brackets

The IRS uses a progressive system. That's a fancy way of saying your income is like a bucket that overflows into different pools, each taxed at a higher rate. For 2023, those rates were 10%, 12%, 22%, 24%, 32%, 35%, and 37%.

Most people think if they hit the 22% bracket, all their money is taxed at 22%. That’s wrong. It's a common myth that keeps people from asking for raises. You only pay the higher rate on the dollars that actually fall into that specific bucket.

For a single filer in 2023, the 10% rate covered everything up to $11,000. If you earned $11,001, only that one extra dollar was taxed at 12%. Basically, the 2023 tax tables 1040 were designed to protect your first few thousand dollars from being decimated by the tax man. Married couples filing jointly saw these thresholds doubled, with the 10% bracket topping out at $22,000.

The Standard Deduction Jump

This was the big story. For 2023, the standard deduction for single filers went up to $13,850. For married couples, it hit $27,700.

📖 Related: Kuwait Dinar to Indian Rupee: Why Everyone Is Watching the 294 Mark

Why does this matter? Because it’s the "free" money you don't pay taxes on. If you earned $50,000 as a single person, you weren't actually taxed on $50,000. You subtracted that $13,850 first. Most people don't itemize anymore—ever since the Tax Cuts and Jobs Act of 2017, the standard deduction is so high that keeping receipts for pens and paper just isn't worth the effort for the average W-2 employee.

Credits vs. Deductions: The 1040 Breakdown

Deductions lower the income you're taxed on. Credits are better. Credits are a dollar-for-dollar reduction in what you owe.

In 2023, the Child Tax Credit remained at $2,000 per qualifying child. However, there was a lot of confusion because the "extra" pandemic-era boosts had long since expired. Many parents opened their tax software expecting a $3,000 or $3,600 credit like they saw in 2021, only to realize the 2023 tax tables 1040 had reverted to the old rules. It felt like a pay cut. It sucked.

Capital Gains and the "Secret" 0% Rate

A lot of people don't realize that the 2023 tax tables 1040 also apply to investments, but in a totally different way. If you held a stock for more than a year before selling it, you were looking at long-term capital gains rates.

Here is the kicker: if your total taxable income was under $44,625 as a single filer, your capital gains tax rate was 0%. Zero. You could sell a stock, make a profit, and the IRS wouldn't take a dime of it as long as your total income stayed under that threshold. Once you went over that, the rate jumped to 15%, and eventually 20% for high earners. It's one of the most powerful tools for building wealth, yet most middle-class families don't realize they might qualify for that 0% bracket.

Common Mistakes People Made with 2023 Filings

The 1040 form itself is deceptively short, but the schedules (Schedule 1, 2, 3) are where things get messy.

One major pitfall in 2023 involved the "Side Hustle" tax. With the rise of DoorDash, Etsy, and freelance gigs, many people received 1099-K forms. While the IRS delayed the $600 reporting threshold, many platforms sent them out anyway. If you didn't report that income because you thought the "rule changed," you probably got a letter in the mail later. The IRS knows. They always know.

Another nuance? The Earned Income Tax Credit (EITC). This is specifically for low-to-moderate-income working individuals and families. For 2023, the maximum EITC for those with three or more qualifying children was $7,430. That’s life-changing money for a lot of people, but if you don't check the right box on your 1040, you lose it.

👉 See also: Emily Newton Flemington NJ: Why This Name Keeps Popping Up in Local Property and Tech Circles

The Reality of Effective Tax Rates

Don't confuse your "marginal" rate with your "effective" rate. Your marginal rate is the highest bracket you touched. Your effective rate is the actual percentage of your total income that went to the IRS.

For instance, someone earning $100,000 in 2023 might have been in the 22% marginal bracket, but after the standard deduction and the lower 10% and 12% tiers, their effective rate was likely closer to 13% or 14%. It feels better when you look at it that way. Sorta.

Actionable Steps for Reviewing Your 2023 Data

If you’re looking back at your 2023 tax tables 1040 info now—maybe because you’re amending a return or applying for a mortgage—here is what you need to do.

First, pull your tax transcript directly from the IRS website. Don't rely on the "preview" PDF from your tax software; the transcript shows exactly what the IRS has on file for you. It’s the source of truth.

Second, check your "Adjusted Gross Income" (AGI) on Line 11. This number is the gatekeeper for almost every financial benefit in the US, from student loan repayment plans to qualifying for certain housing. If your AGI seems too high, look at "above-the-line" deductions like HSA contributions or student loan interest that you might have missed.

Finally, verify your withholding. If you owed a lot of money when you looked at the 2023 tax tables 1040, your W-4 at work is likely set up wrong. You’re giving the government an interest-free loan if your refund is huge, but you're risking penalties if you owe too much. Adjust your withholding now so you aren't surprised by the 2024 or 2025 tables.

The tax code is essentially 7,000 pages of "it depends," but staying on top of the actual tables is the only way to make sure you aren't overpaying. Even if 2023 is in the rearview mirror, the lessons about bracket creep and standard deductions are still the foundation for every dollar you earn today.