You’ve probably heard the rumors at the local diner or seen the frantic headlines on Facebook. Taxes in Michigan have been a moving target lately. If you’re living on a fixed income, specifically Social Security, the big question is always: how much of my check does the state actually get to touch?

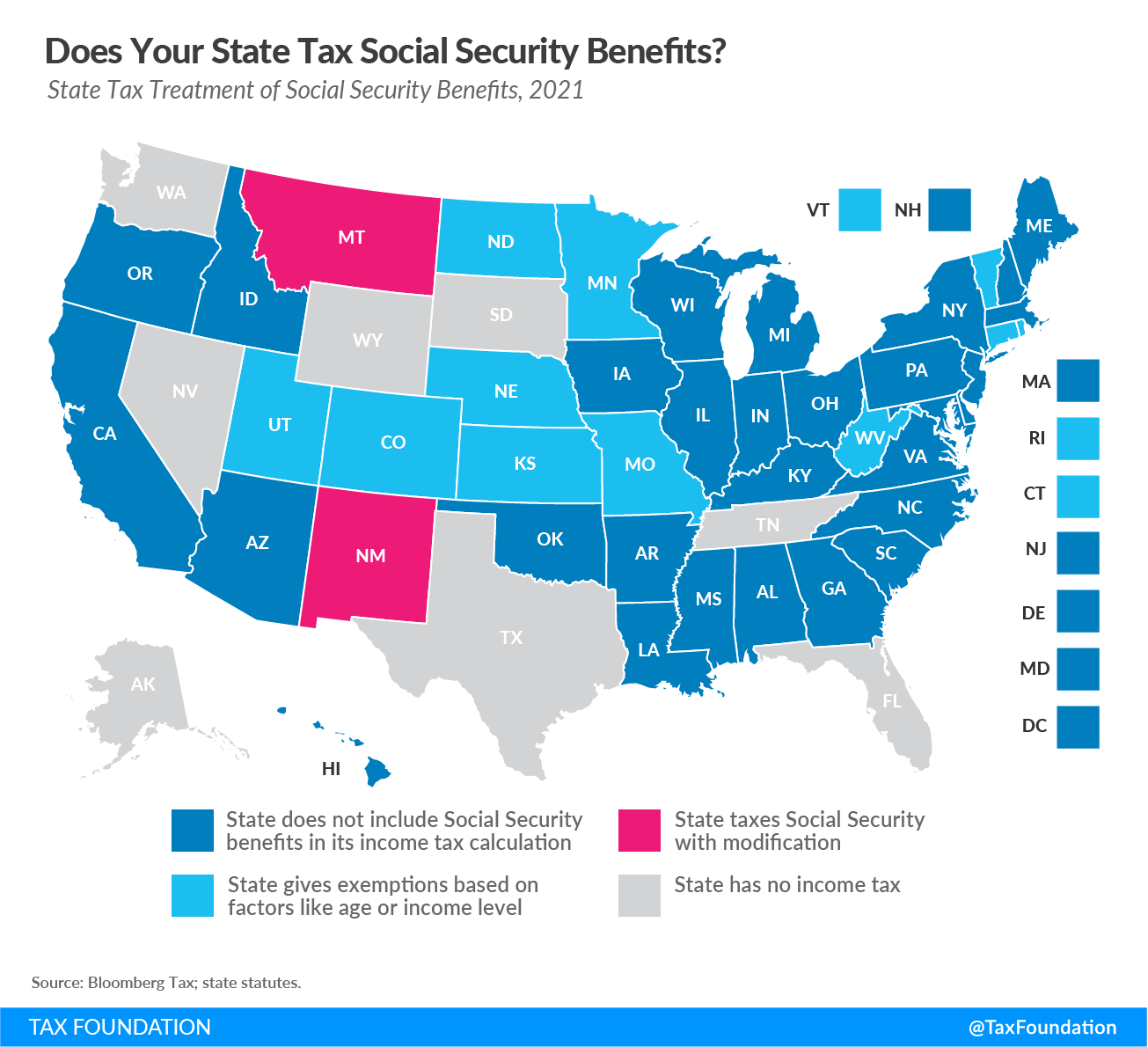

The short answer? Michigan does not tax Social Security benefits.

Honestly, it’s one of the best parts about retiring in the Mitten. Whether you’re collecting retirement, disability, or survivor benefits, the State of Michigan gives you a total pass. No matter if you’re pulling in $15,000 or $50,000 a year from the Social Security Administration, that specific bucket of money is 100% exempt from state income tax.

But here is where things get a little "Michigan-complicated." While the state doesn't take a bite of your Social Security, they’ve spent the last few years arguing over how to tax your other retirement income—like 401(k)s and pensions. And those rules actually affect how you report your Social Security on your tax forms.

💡 You might also like: PA State Tax Percentage: What Most People Get Wrong

Does MI Tax Social Security? The 2026 Reality

If you’re filing your taxes this year, you need to know about Public Act 4 of 2023. People in Lansing call it the "Lowering MI Costs Plan." Basically, it was a massive overhaul designed to undo the old "pension tax" that started back in 2011.

Before this law, Michigan had a weird, three-tiered system. Your tax rate depended entirely on when you were born. It was basically a "birth year lottery." If you were born before 1946, you were golden. If you were born after 1952, you got hit the hardest.

But as of tax year 2026, the phase-in is officially complete.

- The Phase-Out is Done: We’ve reached the 100% mark.

- Universal Equality: For the first time in over a decade, your birth year doesn't dictate your tax rate as much as it used to.

- The Choice: You can still choose between the "old" system and the "new" system if one saves you more money, but for most folks, the new rules are the clear winner.

Even though Social Security itself isn't taxed, it "interacts" with your other deductions. For example, some older rules required you to reduce your standard deduction by the amount of Social Security you received. Luckily, Public Act 24 of 2025 recently stepped in to fix some of those "double-dipping" penalties for seniors aged 67 and older.

A Real-World Example

Let’s look at "Gina." She’s 73, living in Grand Rapids. She makes $23,000 from a part-time job, $5,000 from a small pension, and $12,000 from Social Security.

- Total Income: $40,000.

- The Michigan Rule: Michigan ignores that $12,000 of Social Security immediately.

- The Deduction: Because she's over 67, she gets a standard deduction. In the past, the state would make her subtract her Social Security from that deduction (which sucked).

- The New Law: Now, thanks to the 2025 updates, she gets to keep her full deduction and the Social Security exemption. Her taxable income drops significantly.

The "Federal Catch" You Can't Ignore

Look, just because Michigan is playing nice doesn't mean the IRS is. This is the part that trips most people up.

Uncle Sam uses something called "Combined Income" to decide if they want a piece of your Social Security. They calculate it like this:

Adjusted Gross Income + Nontaxable Interest + 50% of your Social Security benefits.

If that number is over $25,000 (for individuals) or $32,000 (for couples), you’re going to owe federal taxes. Michigan will still let you deduct those benefits on the state return, but you’ll see the impact on your federal 1040.

What About the "Senior Bonus Deduction"?

There’s been a lot of talk about the One Big Beautiful Bill Act (OBBBA). This added a "Senior Bonus" for people 65 and older. If your income is under certain thresholds ($175k for singles), you might be able to claim an extra $6,000 deduction on your federal return. This is huge because it can lower your overall taxable income, even if it doesn't change Michigan's "zero tax" policy on Social Security.

🔗 Read more: 54 dolares a pesos mexicanos: Lo que realmente recibes tras comisiones e impuestos

Why 2026 is a "Cliff" Year for Many

While we’re celebrating the end of the pension tax, there’s a catch. Some of the newest tax breaks—specifically the exemptions for tips and overtime—are currently set to expire after 2028 unless the legislature renews them.

For retirees, the most important thing to watch is the withholding.

Since the law changed so much recently, your pension administrator might still be taking out Michigan state tax based on the old 4.25% rate. If you don't update your MI W-4P, you’re basically giving the state an interest-free loan until you get your refund.

Expert Tip: Check your January 1099-R forms. If you see "Michigan Tax Withheld" and your total retirement income is under the new, higher exemption limits ($65,987 for singles in 2026), you’re overpaying.

Actionable Steps for Michigan Retirees

Don't just leave it to chance. Taxes are boring until you realize you're overpaying by three grand.

✨ Don't miss: Why the Blue Ocean Strategy Book Still Makes Most Managers Cringe

- Update your MI W-4P: If you have a private pension or a 401(k) distribution, tell your provider to stop or reduce withholding if your income now falls under the exempt thresholds.

- Keep your SSA-1099: You still have to report the Social Security amount on your Michigan return even though you’re going to subtract it later. Don't skip this step or you'll get a "math error" notice in the mail.

- Claim the Senior Bonus: If you're 65+, make sure your tax preparer knows about the federal OBBBA deduction. It's brand new and easy to miss.

- Look at the Homestead Property Tax Credit: Since you aren't paying tax on Social Security, your "taxable income" is lower, which might make you eligible for a bigger property tax credit. It’s a double win.

Michigan has become one of the more tax-friendly states in the Midwest for seniors. Between the 0% tax on Social Security and the total phase-out of the pension tax this year, the "Mitten" is finally living up to its name—staying warm and protective of your retirement nest egg.

Next Steps for You:

You should pull your most recent pension statement and check the "State Tax Withholding" line. If they are still taking out 4.25%, visit the Michigan Department of Treasury website to download the 2026 version of Form MI W-4P and submit it to your pension administrator to keep more of your money in your monthly check.