You've probably seen the mailers. Or maybe you already have the card tucked in your wallet because you're trying to drag your credit score out of the basement. Whatever the case, the Credit One Bank app is usually the first thing people download the second they get approved. But honestly, using this thing isn't always as straightforward as the marketing makes it sound.

It's a polarizing tool. On one hand, you have over 10 million downloads on Google Play and millions of ratings on the Apple App Store, many of them hovering around 4.7 or 4.8 stars. On the other, if you spend ten minutes in the review section, you'll find people absolutely fuming about payment delays and glitchy logins.

So, what's the real story? Is it a lifesaver for credit rebuilding or a digital headache?

The "Invisible" Friction in Your Pocket

Most banking apps feel like a sleek glass of water. This one? It feels more like a sturdy, slightly older toolbox. It’s functional, but you have to know which drawer the wrench is in.

🔗 Read more: Images of Alan Turing: What Most People Get Wrong

The biggest thing people get wrong about the Credit One Bank app is assuming it works like a traditional "Big Four" bank app. It doesn't. Because Credit One focuses heavily on "rebuilders"—folks with less-than-stellar credit—the app has some built-in guardrails that can be incredibly annoying if you aren't expecting them.

Take the payment verification.

You go to pay your bill, thinking it's a two-second job. But wait. If you’re using a new bank account, the app might make you verify it, a process that can take three to five business days. During that window, you might not be able to use an alternate payment method. If your due date is tomorrow? You’re in for a stressful 24 hours.

Features That Actually Matter (And Some That Don't)

Let’s talk about what the app actually does well. Because it’s not all doom and gloom in the review section.

- Biometric Login: You can set up Face ID, Touch ID, or fingerprint recognition. In 2026, this is basically the bare minimum, but the implementation here is actually quite stable. It beats typing in a complex password every time you just want to see if your Starbucks transaction posted.

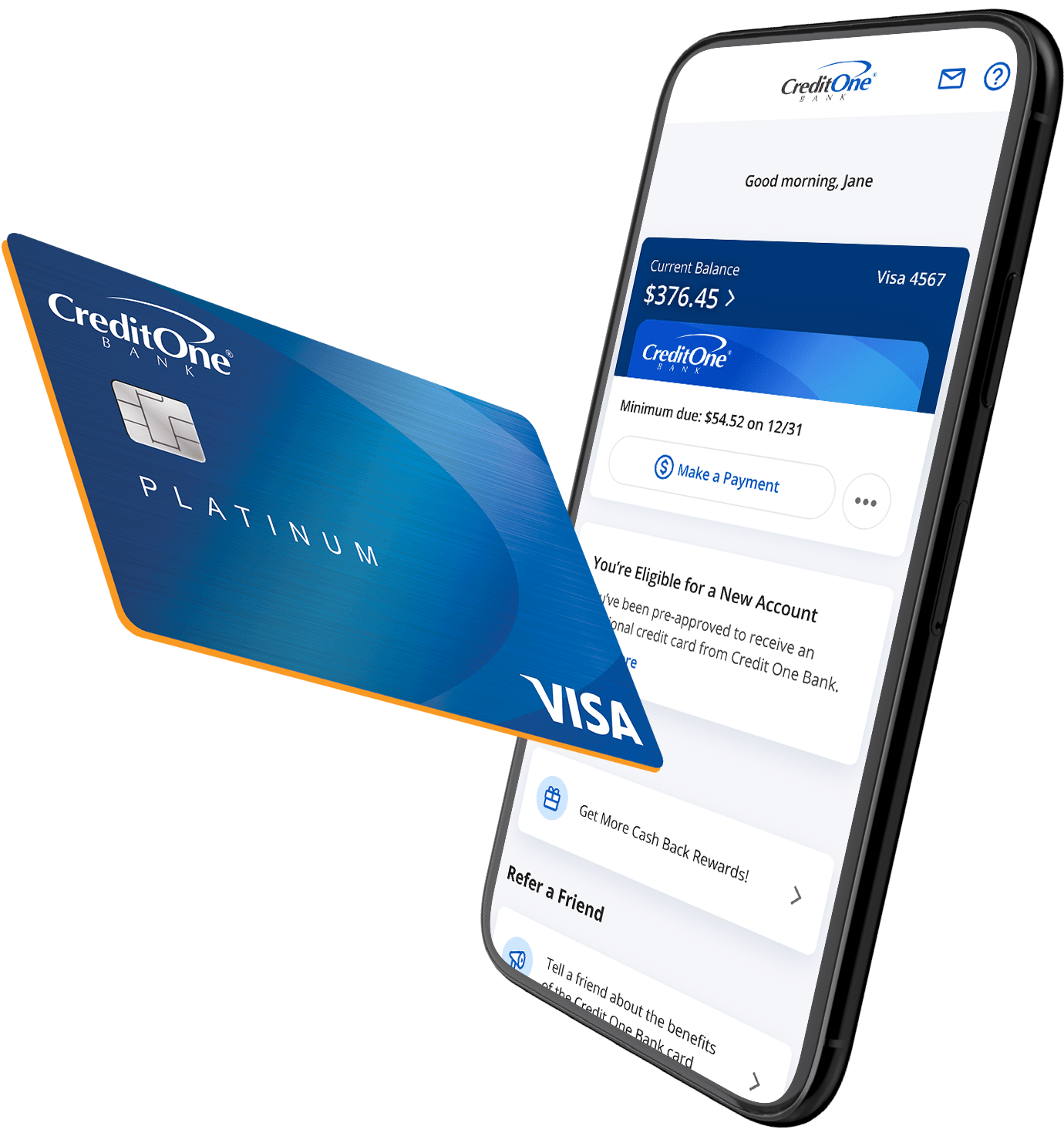

- The Credit Score Gauge: This is the big draw. You get access to your Experian credit score for free. It’s not just a number; it shows you a summary of what's actually moving the needle. It’s updated monthly, which is fine for most, though some modern apps now update weekly.

- Quick View: This is a neat little feature. You can see your balance and available credit without even signing in. Great for a quick check at the grocery store checkout line.

- Notifications: You can toggle alerts for everything. Payment due? Ping. Balance hit a certain limit? Ping. Fraud suspected? You get the idea.

Why the "Express Payment" Fee exists

Here is a detail that catches people off guard. If you’re rushing to make a payment on the due date, the app will offer you "Express Payment."

It sounds like a courtesy. It’s actually a paid service.

Standard payments are free but can take longer to reflect on your available credit. Express payments post faster but usually come with a fee. This is a common point of contention. Most modern fintech apps have moved away from this "pay-to-pay-fast" model, but Credit One still leans into it.

The Security Reality Check

Is it safe? Yeah, mostly. The app uses standard encryption and the bank is FDIC-insured.

But "safe" doesn't mean "seamless."

Users often report that if they travel, the app can get a little trigger-happy with the security blocks. If you're planning a trip, use the app to set a travel notice. If you don't, you might find yourself stuck at a gas station in a different state with a "declined" message and a locked app.

Managing Multiple Cards

Kinda surprisingly, the app handles multiple Credit One accounts better than some of its competitors. If you have a Platinum Visa for rebuilding and later get an American Express version for rewards, you can toggle between them without logging out.

It’s a small win, but for someone juggling different due dates to optimize their credit utilization, it's a massive time-saver.

Dealing With the "Glitch" Factor

Let’s be real: no app is perfect.

Common complaints in 2026 still center around "ghost" notifications—where the app says you have a payment due even after you've paid it. Or the dreaded "system maintenance" screen that seems to appear at the most inconvenient times, like 11:00 PM on a Sunday when you’re trying to check your balance.

If the app hangs, don't just keep tapping. Close it out. Clear your cache. Honestly, sometimes the mobile website is more stable than the app itself during high-traffic periods.

💡 You might also like: How to Delete a Page on Facebook Without Losing Your Mind

How to Win with the Credit One Bank App

If you want to use this app without losing your mind, you need a strategy. You can't treat it like a "set it and forget it" tool.

- Don't wait until the due date. Seriously. Because of the potential for payment "holds" or verification delays, aim to pay 3–5 days early.

- Set up AutoPay, but watch it. AutoPay is great for ensuring you never miss a date, but sometimes the app's sync with your external bank can be finicky. Check it once a month to make sure the money actually moved.

- Use the locking feature. If you misplace your card, the "Lock Card" toggle in the app is instantaneous. It's way faster than calling customer service.

- Check the "More Cash Back" rewards. This is often buried in the menu. You can find offers for specific merchants that give you extra percentages back. If you're paying an annual fee for the card anyway, you might as well claw some of that money back through rewards.

The Credit One Bank app is a tool for a specific job: rebuilding. It isn't going to win any design awards, and it might frustrate you with its rigid payment rules. But if you know the quirks—like the verification wait times and the express payment fees—it becomes much easier to manage.

Next Steps for New Users

If you just downloaded the app, your first move should be enabling biometrics in the settings to avoid the login fatigue. Then, go straight to the "Account Notifications" section. Turn on "Payment Posted" and "Payment Due" alerts. It sounds like overkill until the day it saves you from a $39 late fee.