You’ve probably heard people talk about "owning a piece of the company." It sounds fancy. It sounds like something people in tailored suits discuss over overpriced espresso in lower Manhattan. But honestly? For most of us, owning common stock and dividends is just a way to make sure our money isn't rotting away in a savings account while inflation eats it alive.

Common stock is the bedrock of the retail investing world. When you buy a share of Apple or Coca-Cola on an app, you’re buying common stock. You get a seat at the table—sorta. You get to vote on who runs the place, though your 10 shares won't exactly topple the board of directors. But the real "juice" for a lot of people isn't just the price of the stock going up; it’s the dividends. Those are the little "thank you" checks the company sends you just for hanging out.

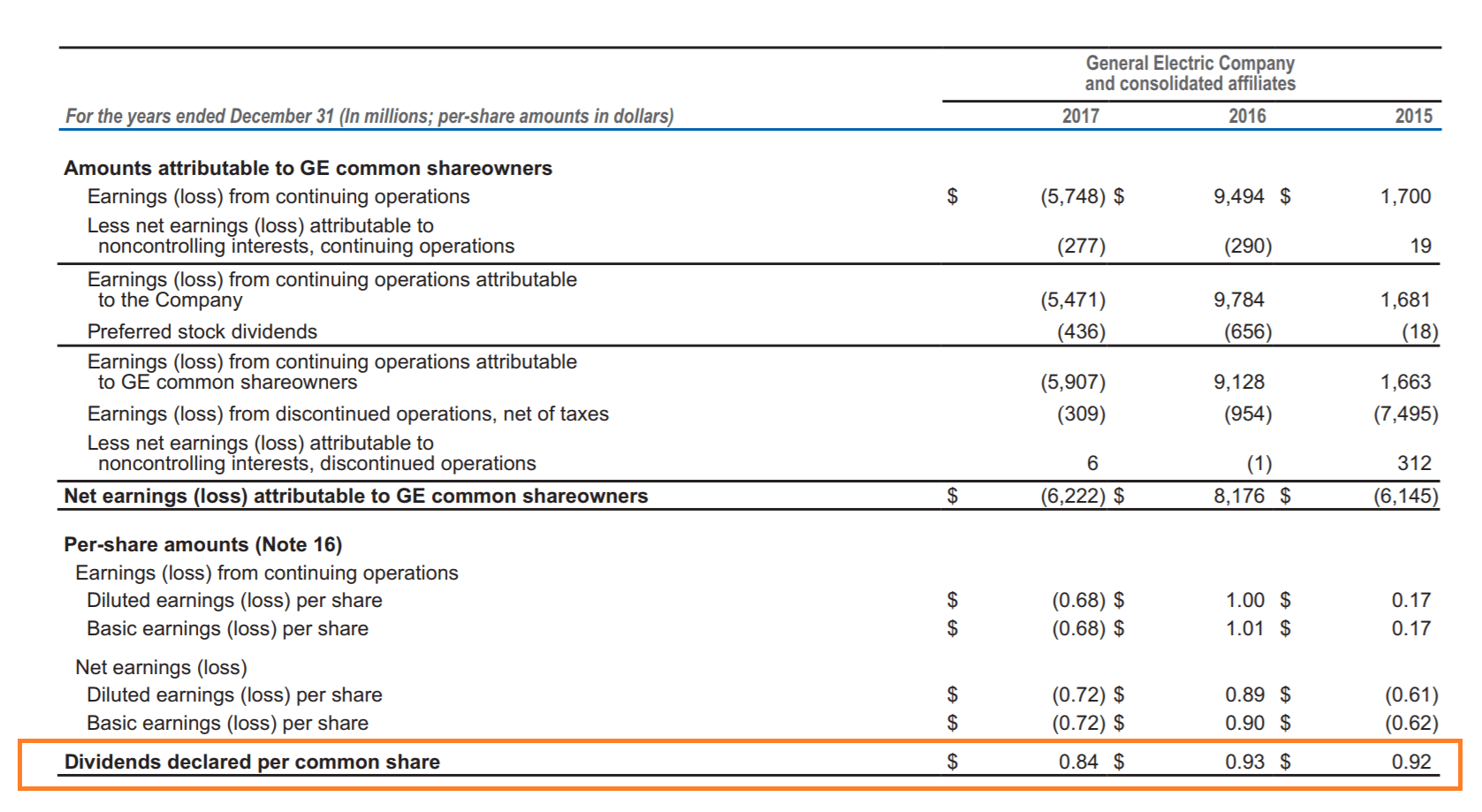

The Reality of Owning Common Stock

Common stock is basically the bottom of the barrel when things go wrong, but the ceiling is infinite when things go right. If a company like Nvidia or Tesla explodes in value, common stockholders are the ones who get rich. Why? Because you own the residual value. After the employees are paid, the taxes are settled, and the bondholders get their interest, everything else belongs to you.

But there’s a catch.

👉 See also: What CVS Stands For: The Meaning Behind Those Red Letters

If the company goes bankrupt? You’re last in line. Bondholders and "preferred" stockholders get their cut first. You get the crumbs, or more likely, nothing. It’s a high-stakes trade-off. You take the most risk, so you deserve the most reward. That’s the theory, anyway.

Voting Rights and the Illusion of Power

Most people don't realize that their common stock usually comes with one vote per share. Every year, you’ll get these annoying emails about "Proxy Voting." Most investors delete them. But these votes decide who sits on the Board of Directors and whether the company should merge with a rival. In 2024, we saw massive drama with Tesla’s shareholders voting on Elon Musk’s pay package. That was common stockholders flexing their muscles. It’s real power, even if it feels abstract when you're looking at your phone screen.

Why Dividends are the Secret Weapon

Dividends are a portion of a company's profit paid out to shareholders. Think of it like a rental property. The house might go up in value (that's the stock price), but the rent coming in every month is the cash flow.

Companies aren't required to pay dividends. Tech giants like Amazon or Alphabet (Google) famously went decades without paying a cent in dividends because they wanted to reinvest every dollar into growing the business. But then, in early 2024, Meta (Facebook) shocked the market by announcing its first-ever dividend. Why? Because they had so much cash they literally didn't know what else to do with it. It was a signal: "We’ve grown up. We’re a cash machine now."

The Dividend Yield Trap

Here is where people mess up. They see a stock with a 10% dividend yield and think they’ve found a gold mine.

Wait.

A sky-high yield is often a giant red flag. Remember, the yield is calculated by dividing the annual dividend by the stock price ($\text{Yield} = \frac{\text{Dividend}}{\text{Price}}$). If the stock price is crashing because the company is failing, the yield looks huge. But if the company is failing, they’re probably going to cut the dividend soon. You buy in for the 10% check, and a month later, they announce the dividend is canceled and the stock drops another 20%. You’ve been trapped.

Dividend Aristocrats and Kings

If you want safety, you look for the "Aristocrats." These are companies in the S&P 500 that have not only paid but increased their dividends every year for at least 25 consecutive years. We’re talking about the boring-but-reliable stuff: Johnson & Johnson, Procter & Gamble, 3M.

"Dividend Kings" are even crazier—50+ years of increases. These companies have survived the 2008 financial crisis, the COVID-19 pandemic, and the stagflation of the 70s without missing a beat. They are the marathon runners of the financial world.

The Tax Man Cometh (And He Wants Your Dividends)

Not all dividends are treated equal in the eyes of the IRS. This is the boring part that actually matters for your bank account.

- Qualified Dividends: These are taxed at the long-term capital gains rate (usually 0%, 15%, or 20% depending on your income). Most stocks you hold for more than 60 days fall here.

- Ordinary Dividends: These are taxed at your regular income tax rate, which can be as high as 37%.

If you're holding high-dividend stocks in a regular brokerage account, you might be giving a huge chunk of your profits to the government. This is why many smart investors keep their "dividend heavy" portfolios inside a Roth IRA or a 401(k), where the growth and the checks are protected from the tax man.

Growth vs. Income: The Great Debate

Should you care about common stock and dividends, or just common stock?

It depends on where you are in life. If you’re 22 and just starting your first real job, dividends might actually be a distraction. You want growth. You want the companies that are aggressively expanding. But if you’re 60 and looking at retirement, you can’t wait 10 years for a stock to double. You need cash to pay for groceries and golf.

There’s also the concept of "Dividend Growth Investing" (DGI). This is the middle ground. You buy companies that pay a small dividend now but grow it fast. Visa is a classic example. Its yield is tiny—usually under 1%—but they increase the payout by double digits almost every year. Over twenty years, your "yield on cost" becomes massive.

Common Misconceptions That Cost Money

- "Dividends are free money." Nope. On the day a dividend is paid (the ex-dividend date), the stock price typically drops by the amount of the dividend. If a stock is $100 and pays a $1 dividend, it starts the next day at $99. You haven't gained net value instantly; you’ve just moved money from the company's pocket to yours.

- "Only old companies pay dividends." While common, it's changing. Tech is maturing. Even Nvidia started paying a (very small) dividend.

- "Companies have to pay dividends." They really don't. A board of directors can vote to axe a dividend in five minutes if they hit a cash crunch. Look at Intel in 2024—a historic dividend payer that had to slash its payout to save its manufacturing business.

How to Actually Start Building a Portfolio

You don't need a million dollars. You can buy fractional shares. But you need a plan.

First, look at the payout ratio. If a company is earning $1.00 per share and paying out $0.90 in dividends, they have no room for error. If their earnings drop to $0.80, the dividend is in trouble. A "safe" payout ratio is usually under 60%.

👉 See also: McHenry County Assessor Property Search: What Most People Get Wrong

Second, check the debt. A company might be paying a dividend while drowning in loans. That’s like someone paying for a luxury vacation on a credit card while they're behind on their mortgage. It’s a facade. Check the balance sheet on sites like Yahoo Finance or Seeking Alpha. Look for "Total Debt/Equity." If it’s skyrocketing, walk away.

Practical Steps for the Modern Investor

If you're ready to move beyond just reading about it, here is how you actually handle your common stock and dividends strategy:

- Enable DRIP (Dividend Reinvestment Plan): Most brokerages like Fidelity, Schwab, or Vanguard let you do this with a single click. Instead of getting $5.42 in cash, the brokerage automatically buys $5.42 worth of more shares. Over decades, this "compounding" is what turns small accounts into fortunes.

- Diversify Across Sectors: Don't just buy "Real Estate" stocks (REITs) because they have high dividends. When interest rates rise, those stocks usually tank. Mix it up with Consumer Staples, Tech, and Healthcare.

- Watch the Ex-Dividend Date: If you buy a stock the day after this date, you don't get the upcoming check. You have to own it before this cutoff.

- Use ETFs if You're Lazy: If you don't want to research individual companies, buy an ETF like SCHD (Schwab US Dividend Equity) or VIG (Vanguard Dividend Appreciation). They do the heavy lifting for you for a tiny fee.

The world of common stock and dividends isn't about getting rich overnight. It's about building a machine that works while you sleep. It’s about owning businesses that are essential to daily life and getting your cut of the profits. Start small, stay consistent, and don't get blinded by high yields that look too good to be true. Usually, they are.