California taxes are a beast. There’s really no other way to put it. If you’ve lived here for more than a week, you know the Golden State takes its cut with a level of enthusiasm that would make a Victorian debt collector blush. But when January rolls around, everyone starts frantically Googling for a income tax estimator california to figure out if they’re getting a windfall or if they need to start selling plasma to pay the Franchise Tax Board (FTB).

Most people get this wrong because they treat California taxes like a smaller version of federal taxes. It isn’t. Not even close.

California’s tax system is famously progressive. That's a fancy way of saying if you make good money, the state is going to lean on you. Hard. While the federal government has seven tax brackets, California has nine. And that’s before we even talk about the "Mental Health Services Act" tax, which adds an extra 1% to incomes over a million dollars. You might think you're in the middle of the pack, but a simple income tax estimator california search can quickly reveal you're creeping toward a 9.3% or even 10.3% marginal rate faster than you'd expect.

The Progressive Trap and Your Bracket

Honestly, the biggest shock for new residents—or people who finally got that big promotion—is how fast the rates climb. California starts low at 1%, sure. But it hits 8% and 9.3% at income levels that many middle-class families in Los Angeles or the Bay Area hit without trying.

If you are a single filer making $68,827 in taxable income, you aren't just paying a flat rate. You're paying a tiered amount. Everything up to $10,412 is taxed at 1%. The next chunk is 2%. By the time you hit that $60k mark, you are paying 9.3% on every additional dollar.

That’s a massive jump.

When you use a income tax estimator california, you have to look at your "Taxable Income," not your gross. This is where people trip up. They put their salary into a calculator, see a terrifying number, and forget that California has its own standard deduction. For the 2024 tax year (filed in 2025), that's $5,363 for individuals. It’s small. Compared to the federal standard deduction, it feels like a rounding error. This is why many Californians still benefit from itemizing on their state returns even if they take the standard deduction on their federal 1040.

Why the FTB and the IRS Are Not Friends

It would be convenient if California just followed federal rules. They don’t. This is called "non-conformity," and it's the reason your tax software looks like a chaotic mess of additions and subtractions.

Take Health Savings Accounts (HSAs). The IRS loves them. They let you put money in pre-tax, and it grows tax-free. California? They don't care. The FTB treats your HSA contributions as regular income. If you put $4,000 into an HSA, the federal government ignores it, but California taxes it. If you earn interest inside that HSA, California wants a piece of that too.

✨ Don't miss: Pacific Plus International Inc: Why This Food Importer is a Secret Weapon for Restaurants

Then there’s the California Paid Family Leave (PFL). The state pays you, but then they don't tax it. However, the federal government does tax it. It’s a constant back-and-forth that makes a simple income tax estimator california result feel more like a "best guess" than a financial certainty unless you’re adjusting for these specific quirks.

- Social Security: California is one of the states that doesn't tax Social Security benefits. That’s a huge win for retirees.

- Unemployment: Unlike the federal government, California doesn't tax unemployment insurance benefits.

- State Disability Insurance (SDI): You pay into this all year. It’s usually 1.1% of your wages (though the cap was recently removed). It’s a tax that pays for a benefit, and it’s one of those "hidden" costs that most estimators forget to mention.

The Myth of the Flat Tax and Local Add-ons

People often complain about the 13.3% top rate. Yes, it’s the highest in the nation. But very few people actually pay that. You have to be clearing over $1 million to see that number. For the average person making $75,000, your effective rate—what you actually pay as a percentage of your total income—is usually much lower, often around 4% or 5%.

But wait. There’s more.

While we are focusing on a income tax estimator california for personal income, you can’t ignore the total tax burden. We have some of the highest sales taxes in the country. In places like Long Beach or Fremont, you’re looking at over 10% at the cash register.

If you own a home, you’re dealing with Prop 13. This is the one place where California is actually "cheap" compared to states like New Jersey or Texas. Your property taxes are capped at roughly 1% of the purchase price, plus small inflationary increases. This creates a weird dynamic where a person living in a $2 million house they bought in 1975 pays less tax than a person in a $500,000 condo they bought last year.

Capital Gains: The California Gut Punch

If you sell stock or flip a house for a profit, the IRS gives you a break. They have "Long-Term Capital Gains" rates of 0%, 15%, or 20%.

California does not do this.

In California, there is no such thing as a capital gains rate. Your investment profit is taxed exactly the same as your hourly wage at McDonald’s or your salary as a software engineer. If you sell $100,000 worth of Nvidia stock and you’re already in the 9.3% bracket, you’re writing a check to Sacramento for $9,300. Period. No discounts for holding the stock for ten years. This is a massive factor that people miss when they run a income tax estimator california during a year they sold a big asset.

🔗 Read more: AOL CEO Tim Armstrong: What Most People Get Wrong About the Comeback King

Credits That Actually Save You Money

It’s not all bad news. California has a few unique credits that can wipe out your tax bill entirely if you qualify.

The California Earned Income Tax Credit (CalEITC) is huge for lower-income workers. If you make less than $30,000, you might get money back even if you didn't pay any tax. There’s also the Young Child Tax Credit, which can provide up to $1,117 for qualifying families.

If you rent your home and make a modest income, don't forget the Renter’s Credit. It’s not much—$60 for individuals or $120 for married couples—but in a state this expensive, you take what you can get.

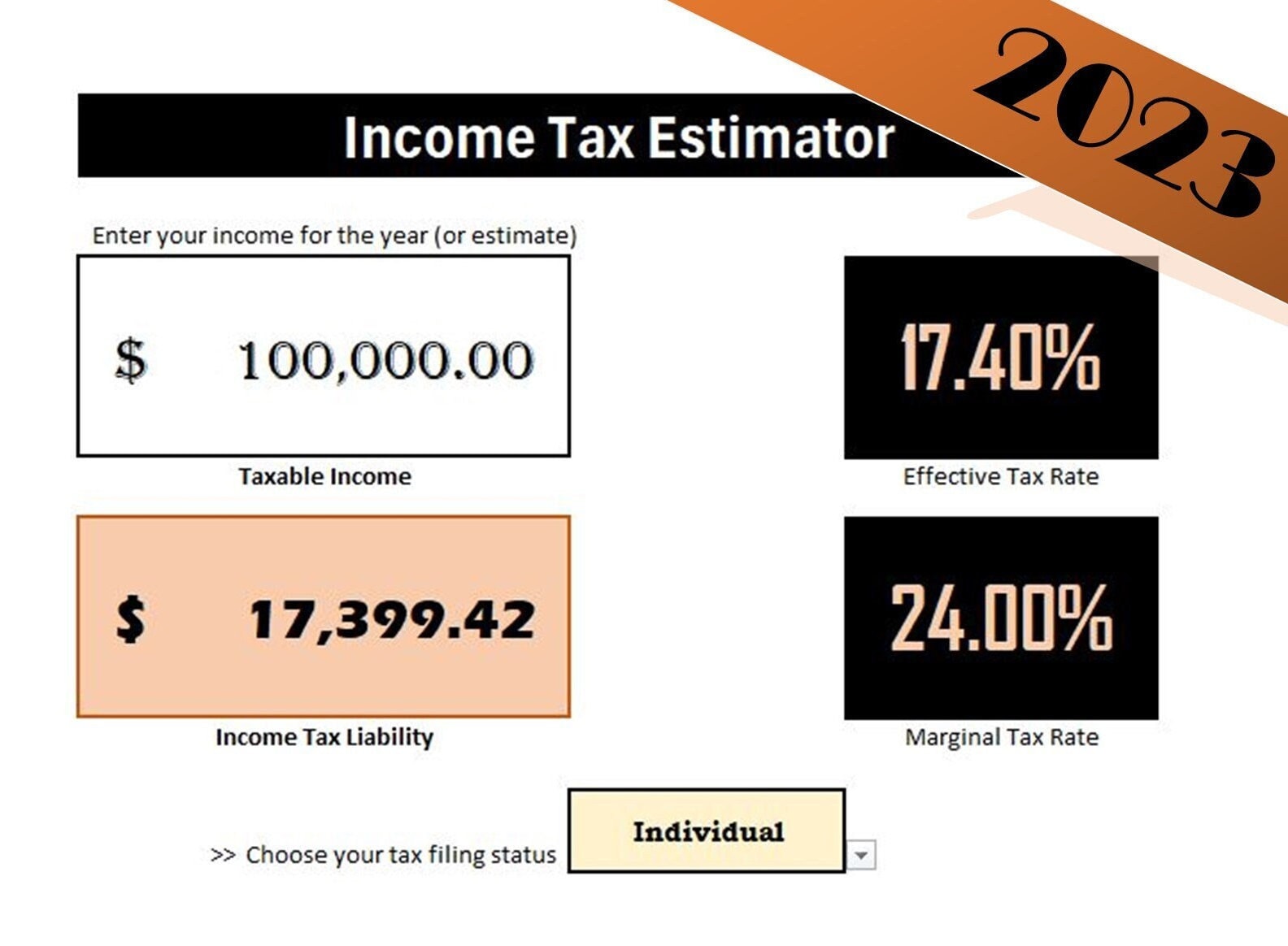

Real World Scenario: The $100k Earner

Let's look at a realistic example. Imagine you’re single, living in San Diego, making $100,000.

After your federal standard deduction, you’re paying a good chunk to Uncle Sam. But for California, you start with that $100,000. You subtract the $5,363 standard deduction. Now you're at $94,637 in taxable income.

The first few brackets are cheap. You’ll pay about $3,500 on the first $68k or so. Then, that remaining $26,000 gets hit at 9.3%. That’s another $2,418. Your total state tax is roughly $5,900.

When you see it laid out, a 5.9% effective rate doesn't sound as scary as "The Highest Taxes in America," does it? But then you look at your paystub and see the SDI tax, the federal tax, and the high cost of gas, and you realize why everyone is obsessed with finding a reliable income tax estimator california.

Common Mistakes When Estimating

Most people fail at estimating because they forget about "Other State Taxes." If you worked a few weeks in New York or Oregon for a business trip, you might owe money there, but California usually gives you a credit for taxes paid to other states. It’s a form called the Schedule S. It is a nightmare to fill out.

💡 You might also like: Wall Street Lays an Egg: The Truth About the Most Famous Headline in History

Another big one? Use Tax. If you bought a couch online from a state with no sales tax and they didn't charge you, California expects you to report that on your income tax return and pay the sales tax manually. Almost nobody does this, but the FTB is getting much better at tracking large purchases.

Actionable Steps for Tax Planning

The year is already moving. If you want to avoid a massive surprise when you actually file, there are things you can do right now that no income tax estimator california can do for you.

First, check your withholding. Go to the payroll portal at your job and look at your DE-4 form. This is the California version of the federal W-4. Many people just mirror their federal settings, but because California's brackets are so different, you might be under-withholding without knowing it.

Second, if you're a freelancer or "1099" worker, you must pay estimated taxes quarterly. The FTB is much more aggressive with penalties than the IRS. If you wait until April to pay the full year's tax, they will tack on an underpayment penalty that can eat into your savings quickly. Use the 540-ES vouchers.

Third, look into the Middle Class Tax Refund or any one-time stimulus programs. California occasionally dips into its surplus to send out "inflation relief" checks. These are usually not taxable by California, but—surprise—they might be taxable by the IRS.

Finally, keep track of your "adjustments." Since California doesn't conform to federal law on moving expenses or certain educator expenses, keeping a separate folder for "California Only" receipts is a lifesaver. If you moved to California for a job, you generally can't deduct those expenses on your federal return anymore, but the state rules are different.

The reality of living here is that the "sunshine tax" is real. Using a income tax estimator california early in the year gives you the leverage to adjust your 401k contributions or your spending before the FTB comes knocking. Information is the only way to keep your head above water in one of the most complex tax jurisdictions on the planet.

Maximize your retirement contributions if you can. While California taxes the HSA, they generally respect 401k and 403b deductions. Reducing your taxable income at the top end—where that 9.3% rate lives—is the most effective way to lower your bill. If you put $20,000 into a 401k, you aren't just saving for the future; you're essentially "saving" about $1,860 in California taxes today.