Checking your paycheck stub in the Badger State usually leads to a few questions. Wisconsin’s tax code has a bit of a reputation for being high, but things are shifting in a pretty significant way for the 2025 tax year. Honestly, if you haven’t looked at the new brackets yet, you might be surprised by how much more of your income is now sitting in the lower tax buckets.

Governor Tony Evers signed the 2025-2027 biennial budget (2025 Wisconsin Act 15), and it’s not just a minor tweak. We're talking about a massive expansion of the second tax bracket. This means more of your hard-earned money is taxed at 4.4% instead of jumping up to 5.3% as quickly as it used to.

It’s a win for the middle class, basically.

The Big Shift: Wisconsin State Income Tax Rate 2025 Brackets

The state still uses a progressive system with four main rates: 3.5%, 4.4%, 5.3%, and 7.65%. But the goalposts moved.

For 2025, the thresholds were widened significantly to fight "bracket creep"—that annoying thing where inflation raises your pay but the tax man takes a bigger percentage because the brackets stayed still.

If you’re filing as Single or Head of Household, here is how your taxable income breaks down:

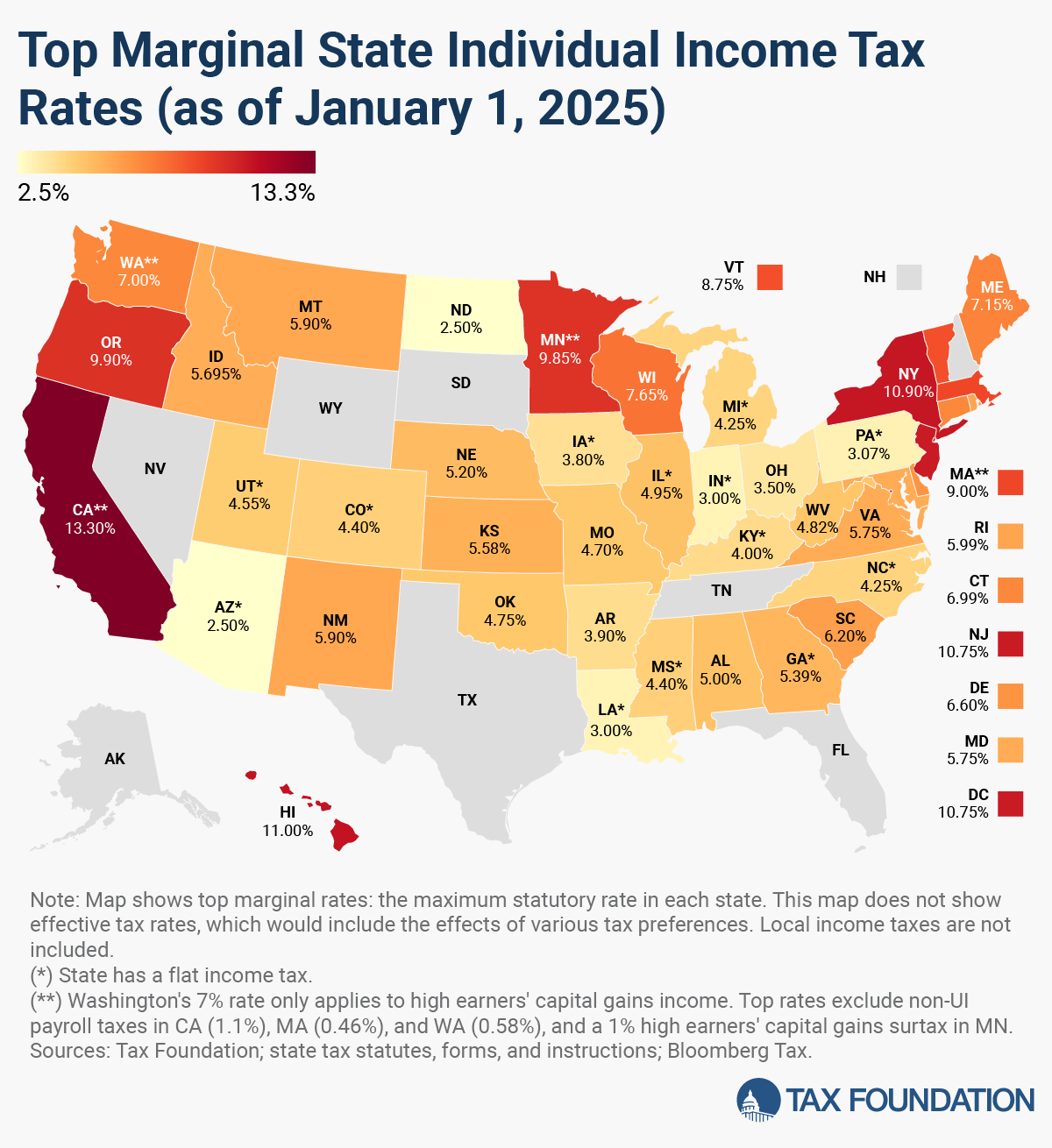

The first $14,680 you earn is taxed at 3.5%. Once you cross that, every dollar up to $50,480 is taxed at 4.4%. This is the big change; previously, that 4.4% rate cut off much earlier (around $29k). Anything from $50,480 up to $323,290 falls into the 5.3% bracket. If you’re lucky enough to clear $323,290, you hit the top rate of 7.65%.

For the Married Filing Jointly crowd, the numbers are even roomier:

- 3.5% Rate: $0 to $19,580

- 4.4% Rate: $19,581 to $67,300

- 5.3% Rate: $67,301 to $431,060

- 7.65% Rate: Over $431,060

Think about that 4.4% bracket for a second. Raising that ceiling to $67,300 for couples keeps a huge chunk of change out of the 5.3% tier. It's real money.

Why the 4.4% Bracket is the "Hero" of 2025

Most Wisconsinites live in that second and third bracket. By stretching the 4.4% range, the state is effectively giving a tax cut without actually lowering the percentage rate itself. It’s a structural change. According to the Wisconsin Legislative Fiscal Bureau, these changes in Act 15 are expected to decrease net taxes by over $1.5 billion over the next two years.

A Game Changer for Retirees

If you’re 67 or older, 2025 is a very good year to be in Wisconsin.

✨ Don't miss: Suez Canal Africa Map: What Most People Get Wrong

Before this update, the retirement income exclusion was a bit of a joke—only $5,000 for singles and $10,000 for couples, and it was heavily restricted by income levels. Now? You can exclude up to **$24,000** of eligible retirement income if you're single, or $48,000 if you’re married filing jointly.

There are some "gotchas," though. You have to be 67 by the end of the tax year. Also, taking this exclusion might disqualify you from certain other credits, so you'll want to run the numbers both ways. But for most seniors, this is the biggest state tax break they’ve seen in decades.

More than Just Income: Sales and Local Taxes

You can't talk about the Wisconsin state income tax rate 2025 without mentioning the stuff that happens at the register. While the state sales tax is a flat 5%, local counties have been busy.

- Milwaukee County: It’s now at 0.9% (plus the 5% state tax and the city’s own 2% tax if you're within city limits). It’s one of the highest in the region.

- New Players: Manitowoc County (as of Jan 1, 2025) and Racine County (as of April 1, 2025) have both introduced their own 0.5% local sales taxes.

Interestingly, the new budget actually eliminated sales tax on residential electricity and natural gas for the "warm" months (May through October), starting late in 2025. It’s a small breather on your utility bills.

Credits and Deductions You Shouldn't Ignore

Wisconsin doesn't just take; sometimes it gives back through specific incentives.

Adoption Expenses: This saw a massive jump. You can now deduct up to $15,000 per child for qualified adoption expenses, up from a measly $5,000.

College Savings (Edvest): The state still loves 529 plans. For 2025, the maximum subtraction for contributions to a Wisconsin state-sponsored college savings account is $5,130 per beneficiary. If you’re married filing separately, that’s halved to $2,560.

👉 See also: 1 billion won to usd: What that money actually buys you today

Standard Deduction: Don't forget this is indexed for inflation. For 2025, it's roughly $14,260 for singles and $26,510 for joint filers. It slides down as you earn more, which is a unique Wisconsin quirk—the wealthier you are, the smaller your standard deduction becomes until it eventually hits zero.

What Most People Get Wrong

A common myth is that if you "move into a higher bracket," all your money is taxed at that higher rate.

That’s not how it works.

If you are single and earn $60,000, only the amount over $50,480 is taxed at 5.3%. Your first $14,680 is still sitting pretty at 3.5%. This is the "progressive" part of the tax code. People often freak out about a raise putting them in a new bracket, but in Wisconsin, you almost always end up with more take-home pay regardless of the bracket shift.

Practical Next Steps for Your 2025 Taxes

Tax season feels far away until it isn't. Here is how to handle the 2025 changes:

- Adjust Your Withholding: Since the brackets widened, you might be over-withholding. Check with your HR department or use the Wisconsin Department of Revenue's updated withholding tables to see if you can put a few extra bucks back in your monthly paycheck instead of waiting for a refund.

- Review Retirement Plans: If you’re approaching 67, the $24,000/$48,000 exclusion might change your strategy for withdrawing from 401(k)s or IRAs.

- Track Adoption and Education Costs: With the limits for adoption expenses and 529 contributions rising, keep every receipt.

- Watch the Sales Tax: If you live in Manitowoc or Racine, remember that local purchases just got a tiny bit more expensive.

Wisconsin’s tax landscape is definitely getting more complex, but for once, the complexity is largely working in favor of the taxpayer. Whether it's the expanded 4.4% bracket or the massive new break for retirees, there’s a good chance your 2025 filing will look better than your 2024 one.