If you’ve spent any time lately scrolling through real estate listings or staring at a mortgage calculator, you’ve probably felt that specific kind of "rate-watch" fatigue. It’s exhausting. You’re waiting for that magic number to drop so you can finally afford that extra bedroom or stop paying a landlord’s equity.

So, will housing interest rates go down in 2026?

The short answer is yes—but probably not in the way you’re hoping for. We aren’t heading back to the 3% glory days of the pandemic. Honestly, those days were an anomaly, a "black swan" event that we likely won't see again in our lifetimes.

As of mid-January 2026, the 30-year fixed-rate mortgage is hovering around 6.06% to 6.18%, according to data from Freddie Mac and Bankrate. That’s a massive relief compared to the 7% and 8% peaks we saw a couple of years ago. But the "downward" trajectory is looking more like a slow, bumpy crawl than a cliff dive.

Why the Federal Reserve is playing hard to get

Most people think the Federal Reserve sets mortgage rates. They don't.

Basically, the Fed sets the Federal Funds Rate, which is what banks charge each other for overnight loans. Mortgage rates usually follow the 10-year Treasury yield. But—and this is a big "but"—the Fed’s vibe matters immensely.

🔗 Read more: Why Edgar Thomson Steel Works Still Matters (and How It Survives)

Right now, the Fed is in a tricky spot. In December 2025, they cut the benchmark rate by 25 basis points to a range of 3.5% to 3.75%. You’d think that would send mortgage rates plummeting, right? Not exactly.

The bond market already "priced in" a lot of those cuts months ago. Investors are forward-looking creatures. If they expect the Fed to cut, rates drop before the meeting. If the Fed sounds "hawkish"—meaning they’re worried about inflation—rates can actually go up even when the Fed cuts. It’s frustratingly counterintuitive.

Jerome Powell, whose term as Fed Chair ends in May 2026, has been trying to balance a cooling labor market with inflation that just won't stay down at that 2% target. There’s a lot of drama behind the scenes, too. With a potential leadership change at the Fed coming up, the market is jittery about whether the next Chair will be more aggressive with cuts or stay the course.

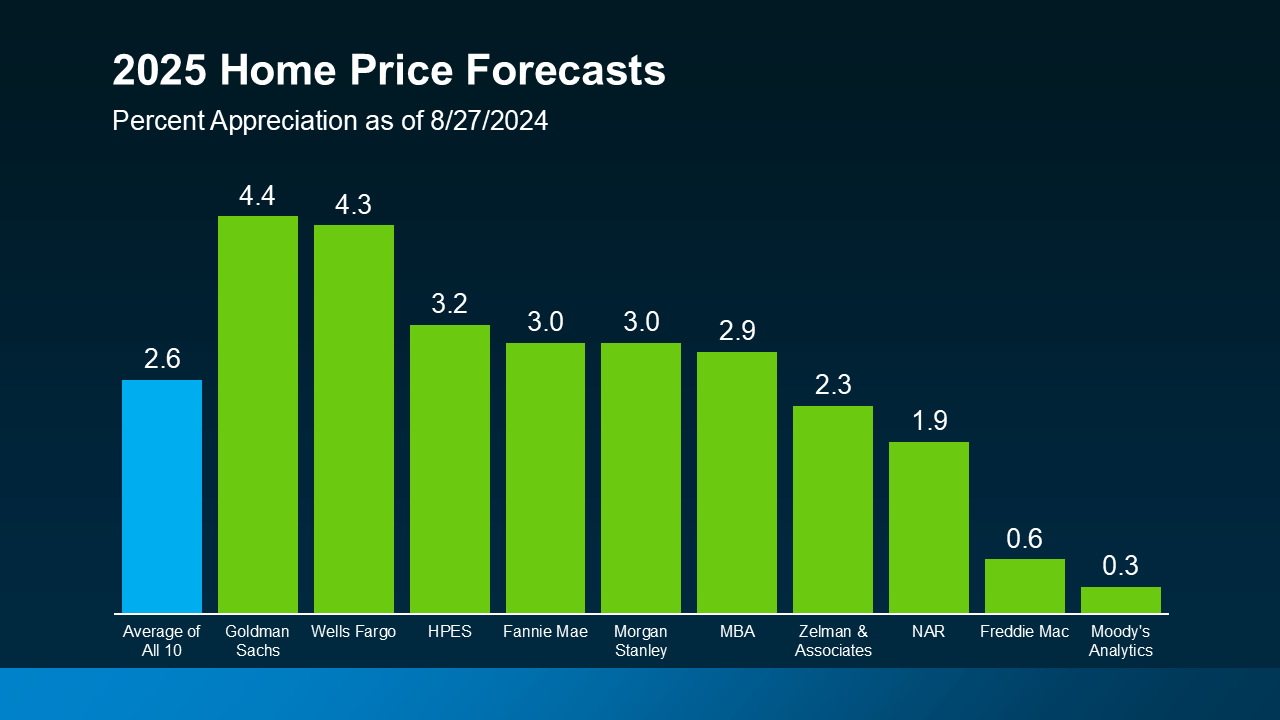

The expert consensus for 2026

If you ask five different economists if will housing interest rates go down further this year, you’ll get six different answers. But there is a general range they're all circling.

The Morgan Stanley View

Analysts at Morgan Stanley are actually somewhat optimistic. They see mortgage rates potentially dipping toward 5.75% in the first half of 2026. Their logic? The 10-year Treasury yield might fall to around 3.75% by mid-year. However, they also warn that rates could creep back up in the second half of the year as the economy stabilizes.

The Bankrate Forecast

Ted Rossman at Bankrate thinks we’ll see the 30-year fixed rate fall below 6% for the first time since 2022. He’s looking at a low of 5.7% and a high of 6.5% for the year. He basically expects rates to "bounce around" the 6% mark.

The "Big Three" Outlook

- Fannie Mae: Predicts a baseline of 5.9% by the end of 2026.

- Mortgage Bankers Association (MBA): A bit more cautious, seeing rates around 6.4%.

- National Association of Realtors (NAR): Expects stabilization near 6.0%.

What does this tell us? Nobody is betting on 4%. If you're waiting for that, you might be waiting a decade.

The "lock-in" effect and the inventory problem

We can't talk about rates without talking about inventory. It's the "ghost in the machine" of the housing market.

Millions of homeowners are currently sitting on mortgages with rates between 2% and 4%. They are "locked in." Why would they sell their home and trade a 3% rate for a 6% rate? They wouldn't. This has kept housing supply at historic lows, which keeps prices high even when demand softens.

Interestingly, as rates have started to drift toward 6%, we're seeing more people finally decide to list. They’re realizing that life—babies, new jobs, divorces—doesn’t wait for the Fed. Redfin is calling 2026 the "Great Housing Reset." They expect home sales to rise about 3% this year because affordability is just good enough to lure some people off the sidelines.

Regional winners and losers

Not every market is feeling the same "rate relief."

If you’re looking in the NYC suburbs or places like Minneapolis and Madison, you’re still in a dogfight. These "commuter" and "affordability" hubs are seeing high demand that offsets any benefit from lower rates.

✨ Don't miss: Boeing and Air India: What Really Happened Behind the Biggest Aviation Deal Ever

On the flip side, the pandemic-era darlings are cooling off. Austin, Nashville, and several coastal Florida cities are seeing homes sit on the market longer. In some of these spots, insurance costs are actually becoming a bigger hurdle than the interest rate itself. Imagine getting a 5.9% mortgage but your homeowners insurance triples. It’s a reality for a lot of people in Texas and Florida right now.

What should you actually do?

The big question: Should you wait or buy now?

Waiting is a gamble. If rates drop to 5.5%, a flood of buyers will likely rush the market. More buyers means more competition, which often leads to bidding wars and higher sales prices. You might save $200 a month on interest but pay $40,000 more for the house.

Honestly, the best advice most pros give is this: Buy when you can afford the monthly payment and you find a house you actually like.

If you bought in 2023 or 2024 when rates were near 8%, 2026 is your year to refinance. If you can drop your rate by 1% or more, the math usually works out in your favor. For example, on a $400,000 loan, dropping from 7.25% to 6% saves you over $300 a month. That's a car payment or a lot of groceries.

Actionable steps for the 2026 market

Stop obsessing over the daily headlines and do these three things instead:

- Check your "refi" math. If your current rate is 7% or higher, call a lender today. You don't need to wait for 5%. The "break-even" point on a refinance is often sooner than you think.

- Watch the 10-year Treasury. If you want to know which way the wind is blowing for will housing interest rates go down, keep an eye on the 10-year Treasury yield. When it drops, mortgage rates usually follow a few days or weeks later.

- Get a "fully underwritten" pre-approval. In a 6% environment, sellers are still picky. Being able to close in 21 days because your paperwork is already done gives you more leverage than a slightly lower interest rate ever would.

The 2026 market is about a return to "normalcy." It’s not a boom, and it’s not a crash. It’s just a slow, steady adjustment to a world where money actually costs something to borrow. It’s a "reset," and for those who are prepared, it’s the first real window of opportunity we’ve seen in years.

Next Steps for You

Evaluate your current debt-to-income ratio to see how much "house" a 6% rate actually buys you today. If the numbers don't work, focus on aggressive savings for a larger down payment, as even a 0.5% rate drop won't fix a fundamentally overstretched budget. For those already in homes with high rates, set a "trigger rate"—a specific number where a refinance becomes a no-brainer—and move the moment the market hits it.