You're sitting at your kitchen table, staring at a screen, wondering if that Caribbean vacation is actually happening this year. We've all been there. You plug a few numbers into a tax refund estimate calculator, see a glorious four-digit number pop up, and immediately start spending it in your head. But here's the kicker: that number is often just a guess. A sophisticated guess, sure, but a guess nonetheless.

The IRS doesn't care about your "estimated" number. They care about the cold, hard math on Form 1040.

Most people use these calculators wrong. They treat them like a crystal ball when they should be treating them like a rough sketch. If you don't understand the difference between a deduction and a credit, or if you forget that one side hustle you did back in July, that calculator is going to give you a number that's about as accurate as a weather forecast in a hurricane.

The Math Behind the Magic

Let’s get real about how a tax refund estimate calculator actually functions under the hood. It’s basically a giant logic tree. It asks for your filing status—Single, Married Filing Jointly, Head of Household—and then starts subtracting. It takes your Gross Income and tries to find your Adjusted Gross Income (AGI).

If you're using a tool from a reputable source like TurboTax, H&R Block, or even the IRS’s own Tax Withholding Estimator, the logic is sound. But the logic is only as good as your memory. Did you remember the $400 you made selling vintage lamps on Etsy? Did you account for the interest on that high-yield savings account that finally started actually yielding interest?

Standard vs. Itemized: The Great Divide

For the vast majority of Americans—we’re talking roughly 90% since the Tax Cuts and Jobs Act of 2017—the standard deduction is the way to go. For the 2025 tax year (filing in 2026), these amounts have shifted again to keep up with inflation. If you’re single, you’re looking at a standard deduction of $15,000. If you’re married and filing jointly, it’s $30,000.

A lot of people get tripped up here. They think they can "write off" their home office and their $5,000 donation to the local animal shelter. But unless those specific expenses add up to more than the standard deduction, they don't move the needle on your tax refund estimate calculator. You're just doing extra math for fun.

📖 Related: What Does a Stoner Mean? Why the Answer Is Changing in 2026

Why Your Estimate Usually Fails

The biggest "gotcha" in tax planning is the difference between a tax deduction and a tax credit.

Ductions lower the amount of income you're taxed on. Credits are way better. They are a dollar-for-dollar reduction in the actual tax you owe. If you owe $3,000 in taxes and you have a $2,000 credit, you now owe $1,000. Simple.

But here is where a tax refund estimate calculator gets messy. It might ask if you have children. You click "yes." It assumes you get the full Child Tax Credit. But wait. Is that credit refundable or non-refundable? If it’s non-refundable and you already owe zero taxes, that credit doesn't turn into a check in your pocket. It just vanishes. This is a nuance that many quick-glance calculators skip over, leading to a "phantom refund" that disappears once you actually file.

The Self-Employment Trap

If you're part of the gig economy, honestly, most basic calculators are going to fail you. They rarely account for the Self-Employment Tax (the 15.3% that covers Social Security and Medicare). You might see a $2,000 refund estimate because your W-2 job over-withheld, but once you factor in the taxes owed on your freelance work, that refund might evaporate into a $500 bill.

I’ve seen people get absolutely blindsided by this. They see the "Refund" box in green and ignore the "Tax Owed" box in red.

Predicting the 2026 Filing Season

We are looking at some interesting shifts this year. The IRS has been aggressively updating their systems, and the "Direct File" program has expanded significantly. This means more people are getting closer to their real numbers earlier in the year.

👉 See also: Am I Gay Buzzfeed Quizzes and the Quest for Identity Online

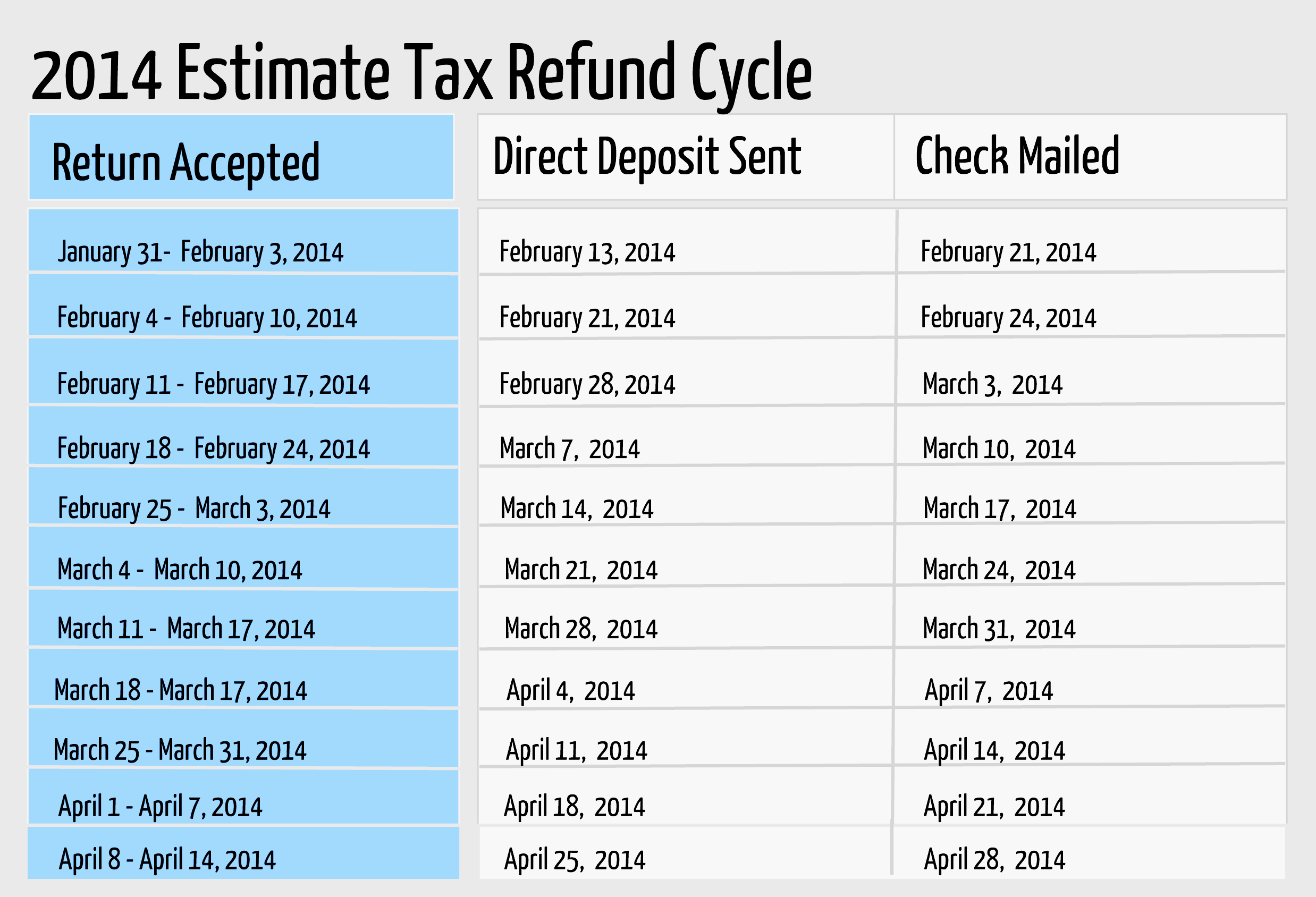

However, the tax refund estimate calculator remains a snapshot in time. If you use one in October, it’s a guess. If you use one in January after you have all your 1099s and W-2s, it's a preview.

The Under-Withholding Crisis

Lately, more taxpayers are finding themselves owing money even when they thought they were safe. Why? Because payroll departments are getting "too good" at their jobs. The goal of the IRS withholding tables is to get you as close to zero as possible. They don't want to give you a big refund. They want to keep your money throughout the year to keep the government running.

If you have a side-hustle or multiple jobs, the withholding from Job A doesn't "know" about the income from Job B. When you combine them on a tax refund estimate calculator, you might realize you’re in a higher tax bracket than either job thinks you are. That’s a recipe for a tax season headache.

How to Get an Accurate Estimate

Stop guessing. If you want a number that actually means something, you need to gather your "paper trail" before you even open a browser tab.

- Grab your last pay stub. Don't look at the "net pay." Look at the "Federal Income Tax Withheld" year-to-date. That is the actual money you've already sent to the IRS.

- Account for the "Unseen" Income. Did you sell crypto? Did you win a sports bet? Did you get a 1099-INT from your bank for more than $10? The IRS already knows about these. If you don't put them in the calculator, the estimate is garbage.

- Check your filing status carefully. "Head of Household" has very specific requirements regarding who you supported and for how long. Choosing the wrong status can swing an estimate by thousands of dollars.

Practical Steps to Take Right Now

Instead of just staring at a tax refund estimate calculator and dreaming, take these steps to ensure you aren't surprised in April.

First, go to the official IRS.gov "Tax Withholding Estimator." It’s less "pretty" than the commercial ones, but it’s the source of truth. It allows you to upload or input your most recent pay stubs to see if you are on track.

✨ Don't miss: Easy recipes dinner for two: Why you are probably overcomplicating date night

Second, if the estimate shows you owe money, don't panic. You still have time to adjust your W-4 at work. Increasing your withholding by even $50 a paycheck for the remainder of the year can wipe out a surprise bill.

Third, organize your receipts for "Adjustments to Income." Things like student loan interest (up to $2,500), HSA contributions made with after-tax dollars, and educator expenses for teachers are "above-the-line" deductions. They reduce your AGI regardless of whether you take the standard deduction.

Most importantly, remember that a refund is just the government returning a 0% interest loan you gave them. If your tax refund estimate calculator shows a $0 refund and $0 owed, you actually won the game. You kept your money in your own pocket all year long.

Check your 2025 totals against the 2026 tax brackets. If your income jumped into a new bracket—for example, moving from the 12% to the 22% bracket—your withholding needs to reflect that shift immediately.

Don't wait until the deadline. Use the tools to plan, not just to hope. Accurate data in means an accurate estimate out. Get your documents in order, adjust your expectations, and use the results to fix your withholding for the next year so you never have to worry about a "lying" calculator again.