Tax season usually feels like a looming cloud. Most people just sit around until January or February, waiting for that envelope from their employer to show up so they can finally see the damage. It’s a reactive way to live. Honestly, if you aren't using a federal tax income estimator at least twice a year, you’re basically flying a plane without looking at the fuel gauge. You might land fine, or you might realize you're empty while you're still three miles up.

The IRS Tax Withholding Estimator is the gold standard here, but people treat it like a chore. It isn't. It’s a strategic move. When you plug your numbers into a federal tax income estimator, you aren't just guessing what you'll owe; you are taking control of your monthly cash flow. Think about it. Would you rather have an extra $200 in every paycheck right now to pay down high-interest credit card debt, or would you rather give the government a 0% interest loan for twelve months just to get a "big refund" in April? The math doesn't lie. The refund is just your own money coming back to you late.

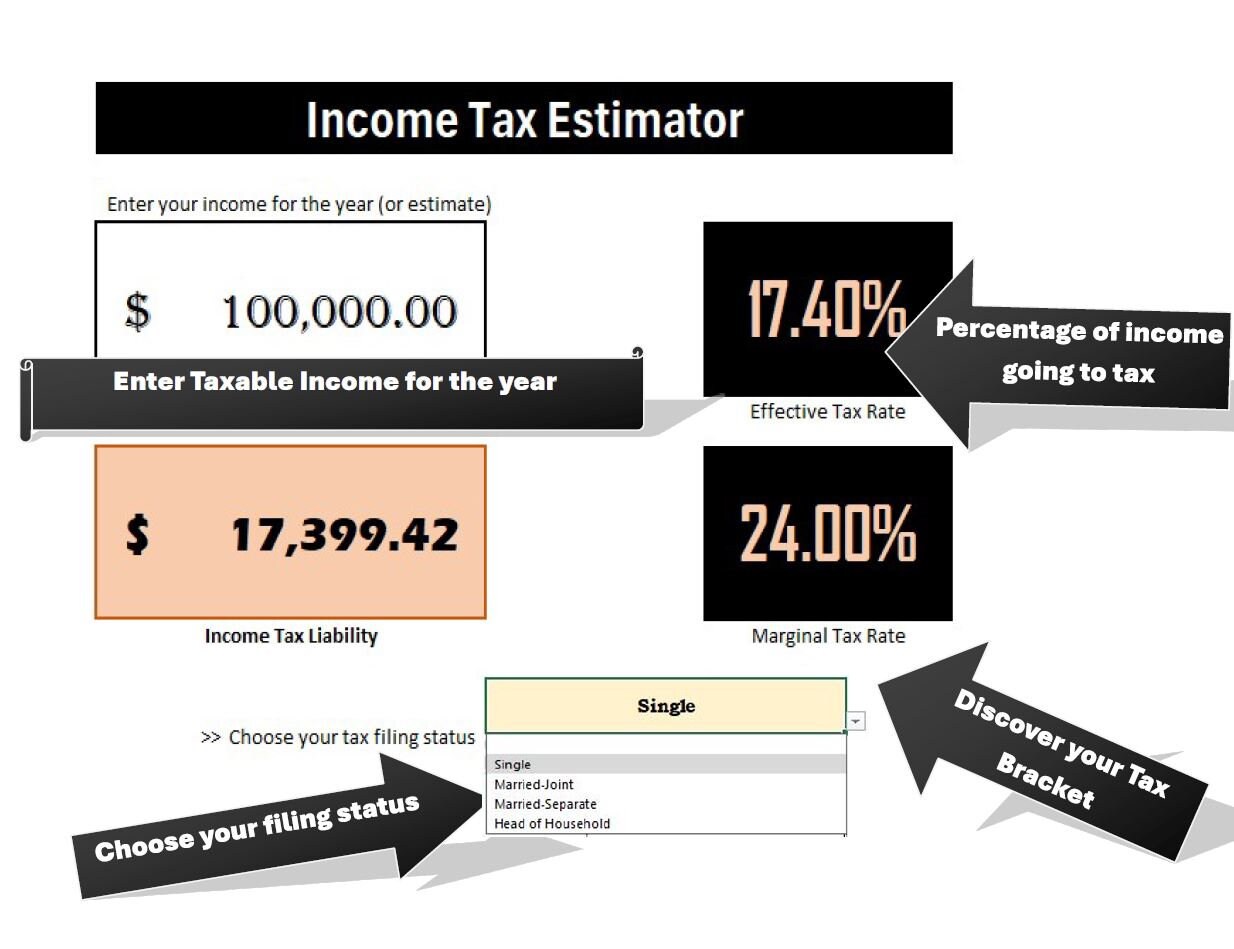

The Math Behind the Federal Tax Income Estimator

It’s not magic. It’s just logic.

Most estimators work by taking your year-to-date income and projecting it forward to December 31. If you made $50,000 by June, it assumes you’ll hit $100,000 by the end of the year. Then, it subtracts your standard deduction. For 2025, that’s $15,000 for single filers and $30,000 for married couples filing jointly. The tool then applies the progressive tax brackets—10%, 12%, 22%, and so on—to find your "tax liability."

The real trick is the credits.

💡 You might also like: Apartment Decorations for Men: Why Your Place Still Looks Like a Dorm

If you have kids, the Child Tax Credit is a massive needle-mover. If you’re a student, the American Opportunity Tax Credit (AOTC) can knock $2,500 straight off your bill. A solid federal tax income estimator asks about these things because they aren't deductions; they are dollar-for-dollar subtractions from what you owe. There is a huge difference. Deductions lower the amount of income you're taxed on, but credits lower the tax itself.

Why Your Paycheck Doesn't Always Match Your Reality

Payroll software is literal. It looks at a single pay period and multiplies it by the number of pay periods in a year. If you get a big one-time bonus, the software thinks you make that much every week. It bumps you into a higher withholding bracket. You see a massive chunk of your bonus vanish.

This is where the estimator saves you. By looking at the "big picture" of your annual income, you can see if your employer is over-withholding. If they are, you go to HR, change your W-4, and start seeing that money in your bank account next Friday instead of next year.

The Stealth Taxes People Forget

Standard income is easy. It’s the "other" stuff that trips people up. If you sold some Bitcoin or offloaded a few shares of stock, you’ve got capital gains. Most basic calculators won't ask about this unless you dig into the settings. Short-term capital gains are taxed like regular income, but long-term gains—stuff you held for over a year—get special treatment (usually 0%, 15%, or 20%).

📖 Related: AP Royal Oak White: Why This Often Overlooked Dial Is Actually The Smart Play

Then there’s the side hustle.

The "1099-NEC" life is a trap for the unwary. If you’re driving for Uber or freelancing on the side, nobody is taking taxes out for you. You owe the 15.3% self-employment tax on top of your regular income tax. A federal tax income estimator that doesn't account for the SE tax is worse than useless; it’s dangerous. It gives you a false sense of security while a massive bill builds up in the background.

Adjusting for the 2025-2026 Shift

Tax laws aren't static. We’re currently in a weird period where many provisions of the Tax Cuts and Jobs Act (TCJA) are approaching their sunset dates. While 2025 remains relatively stable, the brackets have been adjusted for inflation. This is called "bracket creep" prevention. If the IRS didn't adjust these, a 3% raise at work could actually make you poorer by pushing you into a higher tax percentage.

When you use a federal tax income estimator, make sure it’s updated for the current tax year. Using a 2023 calculator in 2026 is like using a map of London to navigate New York. You'll recognize some landmarks, but you're going to end up in the river.

👉 See also: Anime Pink Window -AI: Why We Are All Obsessing Over This Specific Aesthetic Right Now

The "Safe Harbor" Strategy

If you realize you're going to owe a lot of money, don't panic. You just need to meet the "Safe Harbor" rules to avoid underpayment penalties. Generally, if you pay in 90% of what you owe for the current year, or 100% of what you owed last year (110% if you're a high earner), the IRS won't fine you. They'll still take the money, obviously. But they won't add the extra "thanks for being late" fee.

Actionable Steps to Take Right Now

Stop guessing. Start calculating.

First, grab your most recent pay stub. You need the "Year to Date" (YTD) figures, not just the last two weeks. If you’re married, you need your spouse’s stub too. Tax filing is a team sport.

Second, find a reputable federal tax income estimator. The official IRS one is great for W-2 employees. If you have a complex situation with rental properties or K-1 income, look toward tools from reputable tax software companies like TurboTax or H&R Block. They usually offer free versions of their estimators to get you into their ecosystem.

Third, look at your "Total Tax" from last year’s Form 1040. Compare it to what the estimator is telling you for this year. If there’s a massive gap and you haven't had a massive life change (like a new kid or a $20k raise), something is wrong. Re-check your entries.

Finally, if the tool says you’re going to owe $3,000, don't just sit there. Increase your withholding on your W-4 or start putting $250 a month into a high-yield savings account designated specifically for "The Taxman." By the time April rolls around, you won't be scrambling for a loan. You'll just write a check and move on with your life. Control is better than a surprise. Always.