Tax season is basically the adult version of a surprise pop quiz. You think you’ve got your finances handled until February rolls around and suddenly you’re staring at a W-2 or a pile of 1099-NEC forms wondering if you actually owe the IRS a small fortune. Honestly, it’s stressful. Most of us just want to know one thing: am I getting a refund or do I need to clear out my savings? That’s where a calculator federal income tax tool becomes your best friend, but only if you actually know how to feed it the right data.

Most people treat these calculators like a magic 8-ball. They punch in their gross salary, hit enter, and pray. But the IRS doesn't just look at your top-line revenue. They care about your "taxable income," which is a completely different beast altogether. If you aren't accounting for the standard deduction, your 401(k) contributions, or that side hustle you started in June, your estimate is going to be wildly off.

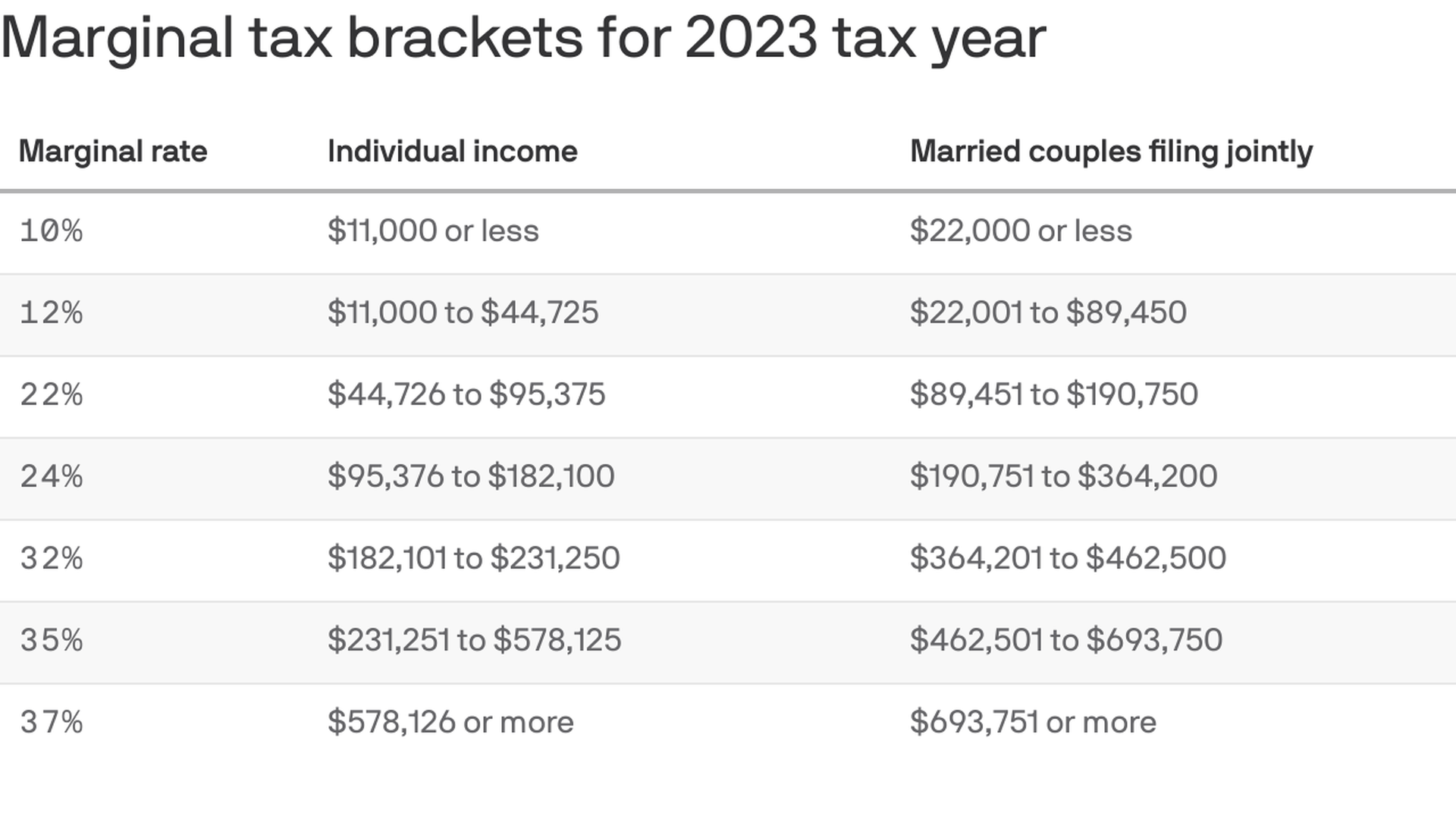

The Reality of the Progressive Tax System

America uses a "progressive" tax system. Some people think if they jump into a higher tax bracket, all their money gets taxed at that higher rate. That’s a total myth. It’s a bucket system. Your first chunk of income is taxed at 10%, the next at 12%, and so on.

Let’s say you’re single and your taxable income is $50,000. You aren't paying 22% on the whole $50k. You’re filling up the 10% bucket first, then the 12% bucket. Understanding this is crucial when using a calculator federal income tax program because it helps you realize why a $5,000 raise might not hit your paycheck as hard as you expected. It also explains why deductions are so powerful—they pull money out of your highest "bucket" first.

Why Your Withholding Might Be Messing You Up

Have you ever gotten a massive refund? Like, five grand?

It feels great. It feels like a gift. But technically, you just gave the government an interest-free loan for a year. On the flip side, if you end up owing the IRS money at the end of the year, it usually means your W-4 at work is set up incorrectly.

The IRS revamped the W-4 a couple of years ago. They got rid of "allowances," which confused everyone who had been doing taxes the same way since 1995. Now, the form asks for specific dollar amounts for dependents and other income. If you haven't updated your W-4 since the 2017 Tax Cuts and Jobs Act (TCJA) took full effect, your calculator federal income tax results might show a scary discrepancy between what you’re paying and what you actually owe.

✨ Don't miss: Rough Tax Return Calculator: How to Estimate Your Refund Without Losing Your Mind

The Standard Deduction vs. Itemizing

For the vast majority of Americans—roughly 90% according to the Tax Foundation—the standard deduction is the way to go. For the 2025 tax year (the taxes you’re likely thinking about right now), the standard deduction jumped again to keep up with inflation.

- Single filers: $15,000

- Married filing jointly: $30,000

- Head of household: $22,500

If your mortgage interest, state and local taxes (SALT), and charitable donations don’t add up to more than those numbers, don't bother itemizing. It’s a waste of time. When you use a calculator federal income tax tool, make sure you’re checking if it automatically applies the current year's standard deduction. If it’s using 2023 or 2024 numbers, your estimate is already wrong.

Don't Forget the "Above-the-Line" Adjustments

This is where the real tax geeks win. Before you even get to the standard deduction, there are "adjustments to income." These are great because they lower your Adjusted Gross Income (AGI).

Why does AGI matter? Because AGI is the gatekeeper for a lot of other credits. If your AGI is too high, you lose the Child Tax Credit or the ability to deduct student loan interest.

Common adjustments include:

- Traditional IRA contributions (if you qualify)

- Health Savings Account (HSA) contributions

- Student loan interest (up to $2,500)

- Educator expenses (for the teachers out there spending their own money on crayons)

If you're using a calculator federal income tax and you don't see a spot for these, find a better calculator. Every dollar you shave off your AGI is a win.

🔗 Read more: Replacement Walk In Cooler Doors: What Most People Get Wrong About Efficiency

The Self-Employment Trap

If you’re a freelancer, a driver, or a consultant, the "federal income tax" is only half the battle. You also have to deal with Self-Employment Tax. This is the 15.3% that covers Social Security and Medicare.

When you work a W-2 job, your boss pays half of that. When you're the boss, you pay both halves. A lot of basic calculators forget to add this in. You might think you owe $4,000 in income tax, but suddenly you’re hit with an extra $6,000 in self-employment tax. It’s a gut punch. Always look for a tool that specifically asks if you have "1099 income" or "self-employment earnings."

Credits vs. Deductions: Know the Difference

People use these terms interchangeably. They shouldn't.

A deduction lowers the amount of income you're taxed on. A credit is a dollar-for-dollar reduction of the tax you owe.

If you owe $3,000 in taxes and you get a $2,000 tax credit (like the Child Tax Credit), you now only owe $1,000. If you got a $2,000 deduction instead, it might only save you $440 (assuming you’re in the 22% bracket).

When you're running the numbers through a calculator federal income tax program, pay close attention to the "Refundable" vs. "Non-refundable" credits. A refundable credit can actually give you money back even if you owed zero taxes. A non-refundable one can only bring your tax bill down to zero—it won't give you a check for the surplus.

💡 You might also like: Share Market Today Closed: Why the Benchmarks Slipped and What You Should Do Now

State Taxes: The Quiet Killer

Unless you live in a state like Florida, Texas, or Washington, you’ve got state income tax to worry about too. Federal calculators often ignore this.

State rates vary wildly. Some are flat (like Illinois or North Carolina), while others are progressive (like California or New York). When you're budgeting your life based on a calculator federal income tax result, remember that you might need to set aside another 3% to 9% for your state's Department of Revenue.

Actionable Steps for an Accurate Estimate

To get a result that actually reflects reality, stop guessing. Open your payroll portal or find your last pay stub.

- Check your Year-to-Date (YTD) Gross: This is your starting point.

- Look at Pre-tax Deductions: Find your 401(k) or 403(b) contributions and health insurance premiums. Subtract these from your gross. This is your likely taxable income.

- Find your Federal Withholding: See how much has already been sent to the IRS.

- Input into the Calculator: Use a tool that allows for "Filing Status," "Dependents," and "Other Income."

- Adjust your W-4: If the calculator says you're going to owe $3,000, go to your HR portal now and increase your withholding for the rest of the year.

Taxes are complicated because life is complicated. No software can perfectly predict your life changes—marriage, a new baby, a house purchase—unless you tell it. Use the calculator federal income tax results as a roadmap, not a final destination. If your situation involves complex stock options (RSUs), rental properties, or foreign assets, a $0 web tool isn't enough. You need an Enrolled Agent or a CPA to make sure you aren't leaving money on the table or accidentally triggering an audit.

The goal isn't just to calculate; it's to plan. The best time to check your tax liability is October, not April. By then, it's too late to change your withholding or maximize your 401(k) to lower your bill. Get the data now, adjust your strategy, and keep more of your paycheck where it belongs—in your bank account.

Check your most recent pay stub against the current 2025 tax brackets to see if your withholding matches your projected income bracket. If you are significantly under-withholding, submit a revised W-4 to your employer immediately to avoid "underpayment penalties" which are essentially just throwing money away. Ensure you have documented all your potential "adjustments to income" like HSA contributions before the April filing deadline, as these can be made up until the day taxes are due for the previous year.