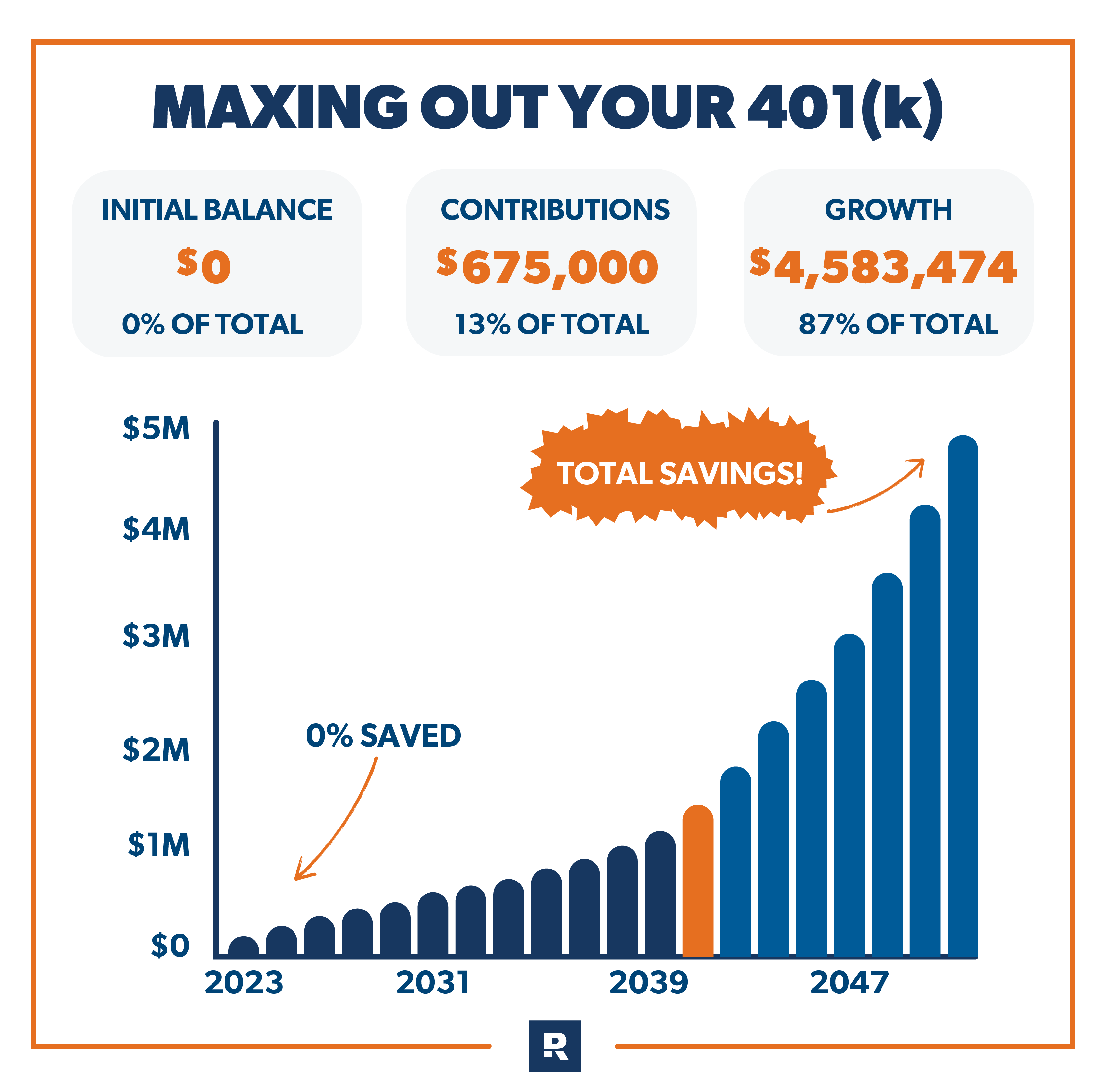

Saving for retirement is weird. You’re basically telling your current self to stop having fun so your 70-year-old self can buy expensive birdseed and go to Florida. It’s a hard sell. But honestly, if you aren't using a 401k max out calculator, you’re probably leaving a massive amount of free money on the table. Most people just pick a random percentage like 5% or 10% because it sounds "responsible." That's a mistake.

The IRS changes the rules every single year. For 2026, the contribution limits have shifted again, reflecting the ongoing adjustments for inflation. If you’re just "setting and forgetting" your contributions based on what you did in 2024 or 2025, you are missing out on tax-advantaged growth that you can never get back. Once the calendar flips to January 1st, that year's "bucket" is sealed. You can't go back and fill it later.

🔗 Read more: Precio dolar americano a peso mexicano: ¿Por qué bajó tanto este enero?

The Math Behind the Max

Let’s get real about the numbers. For 2026, the individual contribution limit for a 401k is $24,000. If you’re 50 or older, you get that "catch-up" bonus, which pushes your total allowable contribution even higher. Think about that. $24,000. That’s $2,000 a month. Most people look at that number and think, "No way." But a 401k max out calculator isn't just for the wealthy. It’s a tool to help you figure out how close you can get without eating ramen for every meal.

It’s about the "Effective Take-Home." Because 401k contributions are (usually) pre-tax, a $500 contribution doesn't actually lower your paycheck by $500. Depending on your tax bracket, it might only feel like $350 or $400. That’s the magic of the tax code. You’re essentially getting a discount on your own savings.

Why Your HR Department is Lying to You (Sorta)

Your HR portal probably has a little slider. You know the one. It lets you pick 1% to 50%. It might even show you a tiny graph.

But those sliders are dumb. They don't know your tax filing status. They don't know about your side hustle. They definitely don't know if you’re planning to front-load your contributions. A dedicated 401k max out calculator allows you to input your specific salary, your existing year-to-date contributions, and how many pay periods you have left.

Here’s a scenario: It’s June. You just realized you’ve only contributed $4,000. You want to hit the $24,000 limit by December. If you just guess a percentage, you’ll either fall short or—worse—you’ll hit the limit in November and lose your company match for December.

Wait, what? Yeah.

Many employers only match on a per-pay-period basis. If you max out too early in the year, you have $0 coming out of your last few checks. If there's no employee contribution, there's often no employer match. You literally lock yourself out of free money by being too aggressive early on. A good calculator prevents this "spillover" error.

The 2026 Limits and the "Catch-Up" Nuance

The SECURE Act 2.0 changed the game. It introduced higher catch-up limits for people aged 60 to 63. This isn't just a minor tweak; it's a significant shift in how people near retirement need to calculate their "max."

If you are in that specific age bracket in 2026, your limit isn't just the standard $24,000 plus the $7,500 catch-up. It's potentially higher. Navigating this without a 401k max out calculator is like trying to do your own dental work. You might survive, but it’s going to be messy.

And don't forget the Roth vs. Traditional debate. If you’re using a calculator, you need to factor in whether you want the tax break now (Traditional) or the tax-free withdrawals later (Roth). High earners in 2026 are also facing new rules where catch-up contributions must be Roth if they earn over a certain threshold. If your calculator doesn't ask for your income, it’s useless for 2026 planning.

Real World Example: The "Mid-Year Pivot"

Let’s look at Sarah. Sarah earns $120,000 a year. She’s paid bi-weekly (26 checks a year).

By the end of March, she’s contributed $3,000. She gets a raise to $130,000 in April. She realizes she wants to hit the $24,000 limit.

✨ Don't miss: Why the 10 year US bond yield is the only number that actually matters for your wallet

- Remaining amount to hit max: $21,000

- Pay periods left: 19

- Required contribution per check: ~$1,105

If Sarah just looks at her HR portal, it might tell her to set her contribution to 15%. But 15% of her new $5,000 gross paycheck is only $750. She’d end the year way short of the max. She needs to set it closer to 22%. This is why the 401k max out calculator is a living document, not a one-time check-up.

The Psychological Barrier

Maxing out is scary. It feels like losing control of your money. But remember: this is your money. You’re just moving it from your "spend now" pocket to your "future yacht" pocket (or "future modest apartment" pocket, let's be realistic).

Most people find that once they automate the max-out process, they stop missing the money. The human brain is remarkably good at spending exactly what is in the checking account. If the money never hits the checking account, the brain just adapts. It's sort of a "forced scarcity" that leads to wealth.

Common Mistakes to Avoid

Don't ignore the "True Up." Some high-end employers offer a "True Up" contribution at the end of the year. This means if you max out early and miss your match, they’ll cut you a check in January to make you whole. Check your Summary Plan Description (SPD). If your company doesn't offer a True Up, you absolutely must pace your contributions perfectly until the last paycheck of the year.

Also, watch out for the total limit. While the $24,000 limit is for your contributions, the total limit (including employer matches) is much higher—$70,000 for 2026. If you have a generous employer or you're doing "Mega Backdoor Roth" maneuvers, you need a much more sophisticated calculation than a basic web form provides.

📖 Related: 1 dollar to dh: Why the exchange rate never actually changes

Actionable Next Steps for 2026

Stop guessing. Seriously.

- Find your last pay stub. Look at the "Year-to-Date" (YTD) 401k contribution line. This is your starting point.

- Count your remaining paychecks. Look at a calendar. Don't assume there are two a month; some months have three if you're bi-weekly.

- Check the 2026 IRS limits. Confirm if you qualify for the $7,500 catch-up (age 50+) or the enhanced SECURE 2.0 catch-up (ages 60-63).

- Input the data into a 401k max out calculator. Adjust the percentage in your payroll system immediately.

- Re-calculate in July. Life happens. Raises, bonuses, or unexpected unpaid time off can throw your numbers off. A mid-year correction is much easier than a frantic December scramble.

If you find that maxing out isn't feasible right now, don't sweat it. Use the calculator to see what a 1% or 2% increase does to your take-home pay. Usually, the difference is the cost of a few pizzas. But over thirty years? That 2% is the difference between working until you're 75 or retiring at 62. The math doesn't lie, even if our brains try to.