Water doesn’t care about your mortgage. It doesn't care about the zip code or how much you paid for that brownstone in Gowanus. When the clouds opened up during Hurricane Ida in 2021, people found out the hard way that the official New York City flooding map they’d looked at during closing wasn't exactly the crystal ball they thought it was. It's a mess. Honestly, navigating these maps is like trying to read a menu in a language you only half-understand while the restaurant is slowly filling with water.

You’ve probably seen the blue shaded areas on a FEMA map. You think, "Okay, I'm outside the blue, I'm safe."

Wrong.

The reality of living in a concrete jungle like New York is that flooding isn't just about the ocean overtopping a seawall. It's about the literal ground beneath your feet being unable to swallow another drop. We're talking about "pluvial" flooding—flash floods from rain—and that is a whole different beast than the "fluvial" or coastal stuff the government usually warns you about. If you're relying on a single map to decide where to live or how to renovate, you're basically flying blind.

The FEMA trap and why your basement is at risk

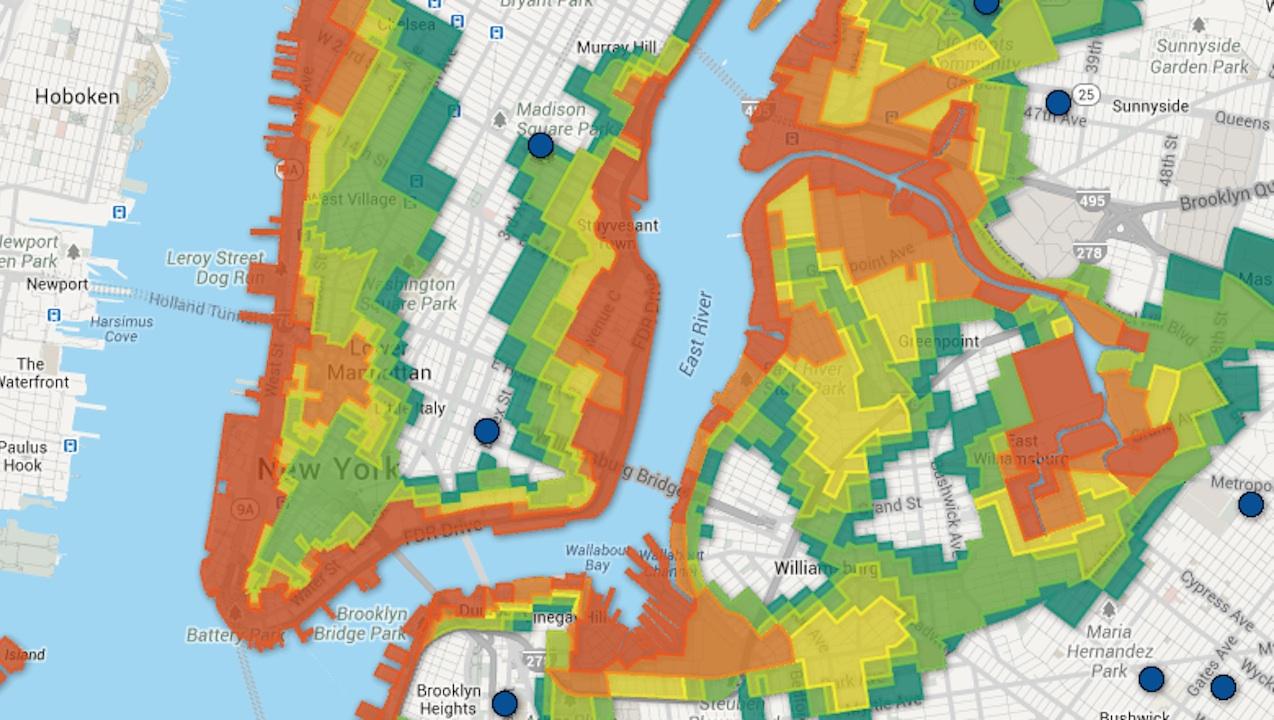

Most people start with the FEMA Flood Insurance Rate Maps (FIRMs). They’re the gold standard for insurance, but they’re also kind of a historical artifact. They focus almost entirely on coastal surges. If you live in the Rockaways or Lower Manhattan, yeah, those maps are your bible. But if you’re in a basement apartment in Woodside, Queens? FEMA might show you’re in a "low-risk" zone while your living room is actually a literal swimming pool during a heavy thunderstorm.

The city has been trying to fix this. They released the "Flood Hazard Mapper," which is a lot better because it starts to layer in things like sea-level rise projections for the 2050s and 2080s. But here’s the kicker: even the best New York City flooding map has trouble accounting for the city's aging sewer system.

Our sewers are old. Really old.

Many parts of Brooklyn and Queens still use "combined" sewer systems. This means the rain runoff and your... well, "toilet stuff," go into the same pipes. When a big storm hits, those pipes get overwhelmed instantly. The water has nowhere to go but up. It backs up through the drains. It bursts through the manholes. No map can perfectly predict exactly which block has a clogged catch basin that will turn a street into a river in fifteen minutes.

👉 See also: Black Red Wing Shoes: Why the Heritage Flex Still Wins in 2026

Stormwater vs. Coastal: Knowing the difference saves lives

If you want to understand your actual risk, you have to look at the NYC Stormwater Flood Maps.

These are different.

The Mayor's Office of Climate and Environmental Justice (MOCEJ) put these out to show where rain—not the ocean—will pool. This is where you see the "moderate" versus "extreme" stormwater flooding scenarios. It’s scary stuff. When you look at the extreme scenario, huge swaths of the inland Bronx and central Brooklyn turn bright blue. This is water that collects in the low spots of our topographical "bowls."

Think about it this way. NYC is not flat. It’s a series of ridges and valleys that we’ve paved over with asphalt. When it rains four inches in an hour, that water follows the ancient path of long-buried streams. It’s looking for the Minetta Brook in Manhattan or the Tibbetts Brook in the Bronx. If your building is sitting on top of one of those old waterways, you are on a New York City flooding map that was written by nature long before the Dutch showed up.

The 100-year flood is a lie (or at least a misunderstanding)

We need to talk about the "100-year flood" terminology because it’s incredibly misleading. People hear that and think, "Cool, I've got a century before the next one."

It actually means there is a 1% chance of that flood happening in any given year.

Over a 30-year mortgage, a property in a 1% zone has about a 26% chance of being flooded. Those aren't great odds. It’s like playing Russian Roulette with your floorboards. And with climate change, those "1% events" are happening every few years now. The maps are struggling to keep up with the pace of the shifting climate. The 2026 data we're looking at now is already reflecting a much more aggressive rainfall pattern than what we saw even five years ago.

✨ Don't miss: Finding the Right Word That Starts With AJ for Games and Everyday Writing

How to actually use a New York City flooding map like a pro

Don't just look at one map. You need to triangulate.

First, hit the NYC Flood Hazard Mapper. Check the "Future Floodplains" layer. This shows you where the water is going to be in 2050. If you’re buying property, this is the only map that matters for long-term value.

Second, go to the NYC Stormwater Flood Maps. Look for "Deep and High Weight" flooding. If your street is highlighted in purple or dark blue, you need to invest in backwater valves and flood barriers yesterday.

Third, check the "Checklist" from the city's "Rainproof NYC" initiative. It’s not a map, but it’s the context the map forgets. It tells you if your neighborhood has high groundwater levels. If the water table is already high, the rain has nowhere to soak into, making the map’s "moderate" risk feel very "extreme" very quickly.

Real-world impact: The tragedy of the basement apartments

We can't talk about these maps without talking about the human cost. During Ida, 13 people died in NYC, mostly in illegal or unregulated basement apartments in Queens. Many of these homes were not in a "special flood hazard area" according to the federal government.

The New York City flooding map for stormwater finally started to highlight these inland risks, but for many, it came too late. There is a massive disconnect between the technical data and the way people actually live. If you’re a renter, you likely won't see a flood map unless you go looking for it. Landlords are now legally required to disclose flood risk in New York, but that doesn't mean they always do it clearly. You have to be your own advocate.

The infrastructure problem: Why maps can't fix everything

The city is trying "Cloudburst" management. They’re building "sunken" parks and permeable pavements in places like South Jamaica and St. Albans. These areas are notorious on every New York City flooding map for being underwater after a light drizzle.

🔗 Read more: Is there actually a legal age to stay home alone? What parents need to know

But infrastructure takes time. Years. Decades.

The map might show that your neighborhood is slated for an upgrade, but until the shovels are in the ground, that blue shading on your screen is your current reality. We also have to consider the "Green Roof" tax abatements. The city is trying to encourage developers to soak up the water at the source—the roof—before it ever hits the street. It’s a smart move, but it’s a drop in the bucket compared to the sheer volume of water we’re seeing in these "supercell" storms.

Actionable steps for every New Yorker

Stop guessing. Start measuring.

If you are a homeowner, check your elevation certificate. This is a document that tells you exactly how high your lowest floor is relative to the base flood elevation. If you don't have one, get one. It can lower your insurance premiums if you’re higher up than the map suggests.

If you’re a renter, ask your landlord point-blank: "Has this unit or the basement ever taken on water?" Check the walls for salt deposits or "efflorescence," which looks like white powder. That’s a sign of moisture pushing through the foundation. Look at the baseboards for warping.

Use the "FloodHelpNY" website. It’s a great resource that combines several maps into one interface. It’s run by the Center for NYC Neighborhoods and it’s arguably more user-friendly than the official city portals. It gives you a clear "Risk Score" based on your specific address.

Next Steps for Property Protection:

- Install a backwater valve. This stops sewage from backing up into your home when the city pipes are full. It's the single best investment for inland NYC residents.

- Elevate your utilities. If your boiler or water heater is on the ground in the basement, get it on a pedestal.

- Get flood insurance. Even if you aren't in a mandatory zone. Remember, a standard homeowners policy does not cover flood damage. You need a separate policy through the NFIP or a private insurer.

- Seal your foundation. Use hydraulic cement to plug gaps where pipes enter the wall.

- Download the Notify NYC app. It’s the fastest way to get flash flood warnings that are specific to your borough.

The maps are just tools, not guarantees. They tell us where the water wants to go, but in a city as complex as New York, the water will always find the path of least resistance. Usually, that path leads right to your front door if you aren't prepared.