You’ve probably noticed it at the grocery store. Or maybe when you’re looking at used car prices and wondering why a Honda with 100,000 miles costs what a new one did five years ago. It feels like money is just... thinner. That’s the devaluation of the dollar in motion, and honestly, it’s a lot more complicated than just "prices going up."

Money is a story we all agree on. But lately, the plot is getting a bit messy. When we talk about the dollar losing value, we’re usually talking about two different things that people often mix up. First, there’s purchasing power—how many eggs your ten-buck bill can actually buy. Second, there’s the exchange rate—how that same ten-buck bill stacks up against the Euro or the Yen. Both are slipping in ways that matter for your 401(k) and your rent.

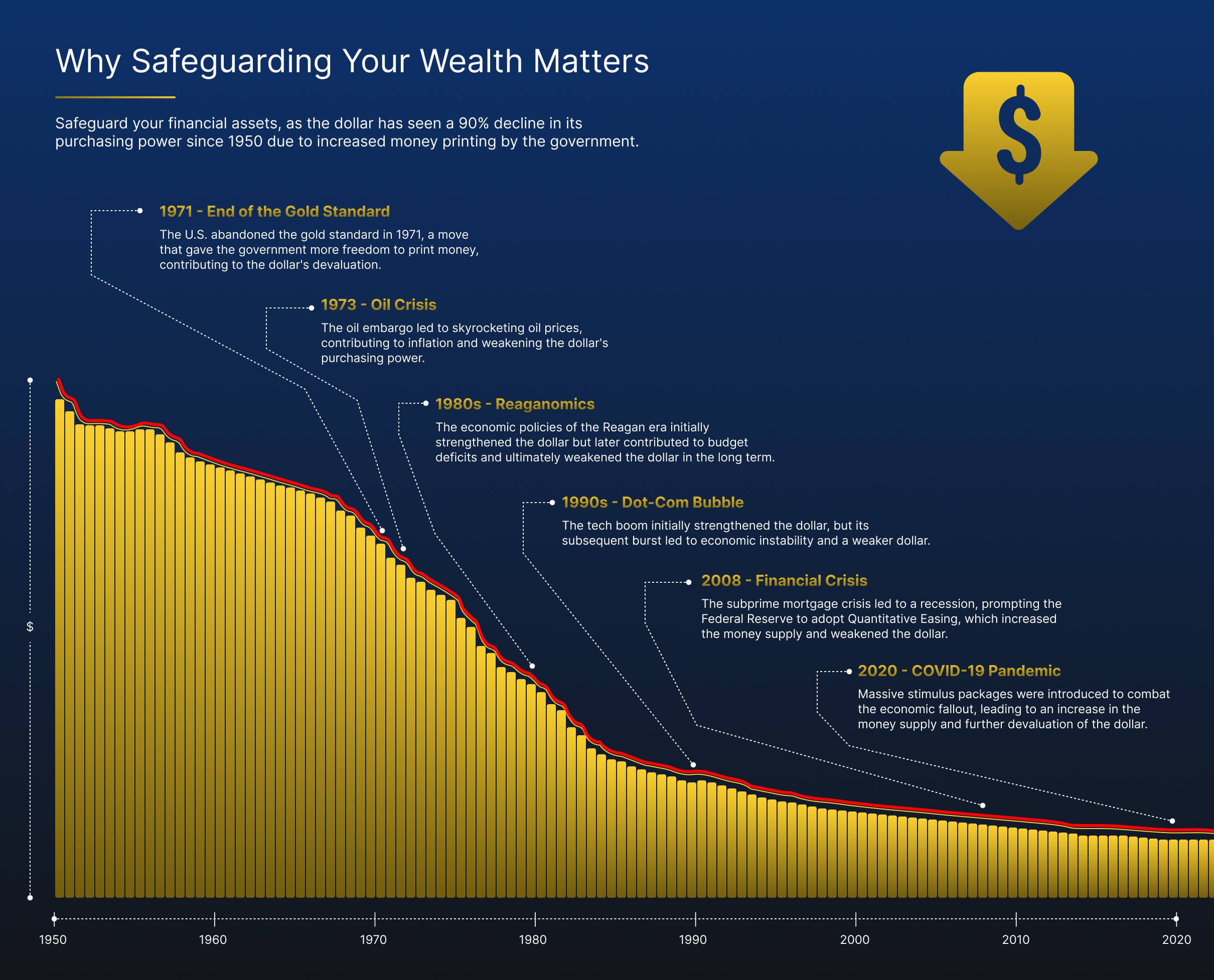

The Brutal Reality of Purchasing Power

Inflation is the most obvious face of a devalued currency. Think back to the stimulus checks and the massive government spending during the early 2020s. The M2 money supply—basically a measure of all the cash, checking deposits, and "near money" in the US economy—exploded. According to Federal Reserve data, the M2 supply jumped by about 27% in 2020 alone. That’s a staggering amount of new liquidity. When you flood the system with more dollars but the amount of stuff to buy stays the same (or shrinks because of supply chain disasters), each individual dollar becomes less "special." It’s basic scarcity.

It’s kinda like a concert. If there are only 100 tickets, they’re worth a lot. If the promoter suddenly prints 5,000 more tickets but the venue size doesn't change, the value of holding an original ticket plummets.

But it isn't just about printing money. We also have to look at interest rates. When the Fed keeps rates low, borrowing is cheap. People take out loans, businesses expand, and money flows like water. This stimulates growth, sure, but it also dilutes the value of the currency. Recently, we’ve seen the Fed hike rates to fight this, but the "damage" to the dollar’s internal value is already baked into the prices you see at the pharmacy or the gas station.

Why the World is "De-Dollarizing" (And Why You Should Care)

For decades, the US dollar has been the undisputed king—the world's reserve currency. If a country wanted to buy oil or trade internationally, they needed dollars. This "exorbitant privilege," a term famously used by French Finance Minister Valéry Giscard d'Estaing, meant the US could run huge deficits because the rest of the world always wanted our currency.

That's shifting.

Countries like China, Russia, and even some BRICS nations (Brazil, Russia, India, China, South Africa) are actively looking for ways to trade without using the greenback. They're tired of US "sanctions power." When the US froze Russia's dollar reserves after the invasion of Ukraine, it sent a shockwave through global central banks. The message was clear: if you cross Washington, your money isn't yours anymore.

- Central Bank Gold Buying: In 2023 and 2024, central banks bought gold at record levels. They aren't doing that for fun. They're hedging against the devaluation of the dollar.

- Bilateral Trade Deals: India has started settling some oil trades in Rupees. China is pushing the Yuan for international contracts.

- The Debt Clock: The US national debt is screaming past $34 trillion. When foreign investors look at that number, they start to wonder if the US will eventually just "inflate its way out" of the debt by making the dollar worth less.

If global demand for dollars drops because people don't need them for trade, the value of the dollar on the international stage falls. Hard. This makes imports—like the electronics and clothes we rely on—much more expensive for American consumers.

The Hidden Tax on Your Savings

Devaluation is basically a hidden tax. If you have $10,000 sitting in a standard savings account earning 0.05% interest while the dollar is devaluing at 4% or 5% a year, you are losing wealth. You aren't "spending" it, but your ability to use that money in the future is being eaten away.

Economist Milton Friedman once said, "Inflation is the only form of taxation that can be imposed without legislation." He was right. Nobody voted for your grocery bill to go up 20%, but it happened because the currency's value was diluted.

It’s not all doom, though. Some people actually benefit from a devalued dollar. If you owe a lot of money—like a fixed-rate mortgage—devaluation is technically good for you. You’re paying back the bank with dollars that are worth less than the ones you originally borrowed. Large corporations with heavy debts also love a little devaluation for this exact reason. But for the average person trying to build a nest egg? It’s a headwind that never stops blowing.

Real-World Examples of the Slide

Let’s look at some specifics. In 1913, the Federal Reserve was created. Since then, the dollar has lost over 96% of its purchasing power. What $1 bought in 1913 would require roughly $30 today. This isn't a "glitch" in the system; it’s a feature of modern fiat currency. Unlike the gold standard, where the dollar was pegged to a physical asset, today’s dollar is backed only by "full faith and credit."

When faith wavers, the currency follows.

What Most People Get Wrong About the "Strong Dollar"

You’ll often hear news anchors talk about a "Strong Dollar" as if it’s always a good thing. It’s a bit of a double-edged sword. A strong dollar means your trip to Europe is cheaper. Great. But it also means American-made products are more expensive for people in other countries to buy. This hurts US manufacturers and can lead to job losses in export-heavy industries.

Conversely, a devaluation of the dollar can actually help the US trade deficit by making our exports more competitive. The problem is that we've become an import-dependent nation. We buy so much from overseas that the "benefit" to our exports rarely makes up for the pain of paying more for everything we bring in.

How to Protect Your Wealth from Devaluation

Waiting for the government to "fix" the currency is a losing game. History shows that once a currency starts this slide, it rarely reverses for long. You have to be proactive.

- Own Productive Assets. Stocks in companies with "pricing power"—meaning they can raise prices without losing customers—are a classic hedge. Think companies like Coca-Cola or Apple.

- Real Estate. Land is finite. Dollars are not. Rental property allows you to collect "devalued" dollars in higher rent while the underlying asset usually keeps pace with inflation.

- Commodities and Gold. There’s a reason people have turned to gold for 5,000 years. It can't be printed. It’s a "hard" asset that tends to shine when the dollar is shaky.

- TIPS (Treasury Inflation-Protected Securities). These are government bonds specifically designed to increase in value when inflation rises. They aren't perfect, but they're a safer bet than a mattress full of cash.

- International Diversification. Don't keep all your eggs in the US basket. Investing in foreign markets can give you exposure to currencies that might be performing better than the dollar.

The Long Road Ahead

The devaluation of the dollar isn't going to happen overnight in a single "crash." It’s a slow burn. It’s the "boiling frog" scenario where the water temperature rises just a tiny bit every year until you realize your life's savings don't buy what they used to.

Understanding this isn't about being a "doomer." It’s about being realistic. The fiscal path of the US—massive deficits, high debt-to-GDP ratios, and political gridlock—suggests that the pressure on the dollar isn't going away anytime soon.

✨ Don't miss: Copper price per oz: What Most People Get Wrong About the 2026 Market

Stop thinking of your wealth in terms of "how many dollars do I have?" and start thinking in terms of "what can these dollars buy?" That shift in mindset is the first step toward surviving a devaluing economy.

Immediate Action Steps:

- Audit your cash holdings. If you have more than 3-6 months of expenses sitting in a low-interest checking account, you are actively losing money to devaluation. Move excess cash into high-yield accounts or short-term treasuries at the very least.

- Look at your debt. If you have high-interest variable debt (like credit cards), pay it off immediately. If you have low-interest fixed debt, don't rush to pay it off—let the devaluing dollar do some of the work for you over time.

- Diversify your "store of value." Consider putting a small percentage of your portfolio into "hard assets" like physical gold, silver, or even a highly-vetted basket of commodities to act as a fire insurance policy for your wealth.

The dollar is still the world’s most important currency, but its dominance isn't a law of nature. It’s a choice made by the global market every day. As that choice becomes harder for the world to make, you need to be ready for a future where the greenback doesn't go as far as it used to.