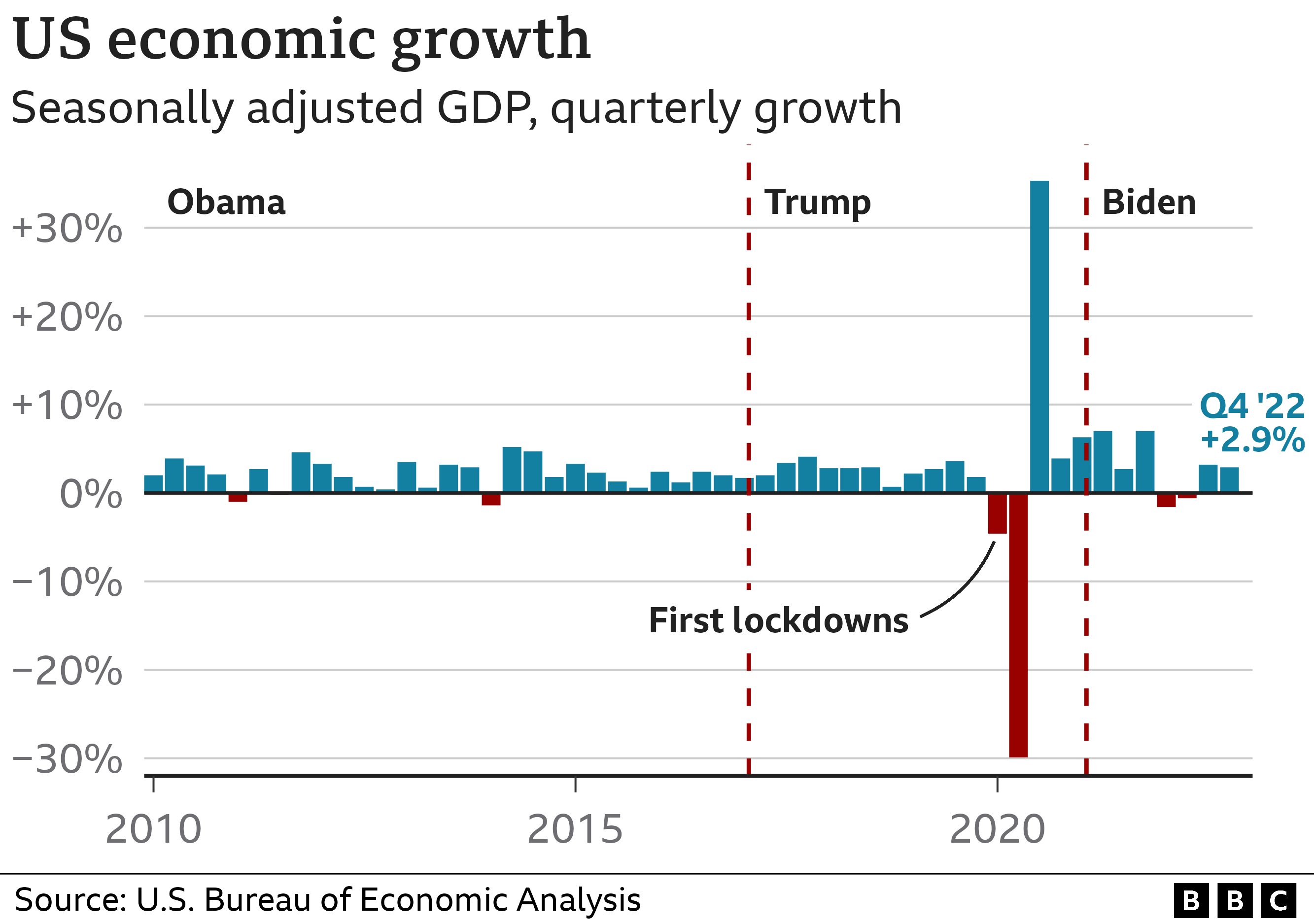

Walk into any grocery store in 2026, and you’ll see it. People are staring at the price of eggs like they’re looking at a car invoice. It’s weird, right? On paper, the Federal Reserve and the Bureau of Labor Statistics are pointing at charts that look... fine. Unemployment is low. GDP is growing. But the vibes are absolutely off. If you’ve been asking why is the american economy so bad, you aren't crazy. You’re just living in the gap between "the economy" (the abstract machine) and "your economy" (the money you actually have left on Friday night).

The truth is complicated. It’s a mix of a massive post-pandemic hangover, weirdly sticky housing costs, and the fact that a $15 burrito now costs $22. We’ve entered an era where the numbers say we’re thriving, but the average person feels like they’re running a race on a treadmill that keeps speeding up.

The Inflation Hangover That Won't Quit

Most people think inflation is "fixed" once the percentage goes down. It’s a total misunderstanding of how the math works. When you hear that inflation has dropped from 9% to 3%, that doesn’t mean prices are going down. It just means they’re going up more slowly. The damage is already baked in.

Imagine you’re at a bar. In 2021, a beer was $6. Inflation hits, and it jumps to $9. Even if the inflation rate "cools off," that beer stays at $9. It never goes back to $6. That’s why people are so frustrated. We’re still paying the 2022 and 2023 "emergency" prices, but our wages haven't caught up to that cumulative jump. According to data from the Economic Policy Institute, while low-wage workers saw some of the fastest growth in decades recently, the middle class is still feeling the squeeze of a 20% total increase in the cost of living over a few short years.

The Housing Crisis Is a Mathematical Wall

You can't talk about why is the american economy so bad without mentioning the fact that nobody can afford to move. It’s a gridlock.

Millions of homeowners are sitting on 3% mortgage rates from the COVID era. If they sell their house to buy a new one, their interest rate might double or triple. So, they stay put. This means there are no "starter homes" for sale. When there’s no supply, prices stay high. It’s basic 101 supply and demand, but it feels like a personal attack when you’re trying to buy a house.

- Interest Rates: The Fed raised rates to kill inflation. It worked, but it also made borrowing money for a house incredibly expensive.

- Corporate Landlords: Firms like Blackstone and various REITs have been buying up single-family homes for years, turning them into permanent rentals.

- The "Golden Handcuff" Effect: People who want to sell can't afford to, which keeps inventory at historic lows.

For a young person today, the "American Dream" of homeownership feels more like a fairy tale. When your rent takes up 40% or 50% of your take-home pay, the economy feels broken, regardless of what the S&P 500 is doing.

🔗 Read more: Price of Tesla Stock Today: Why Everyone is Watching January 28

Why the "Low Unemployment" Number is Misleading

The government loves to tout the 4% unemployment rate. It sounds great. But honestly? It hides the "underemployed" and the "exhausted."

Being employed doesn’t mean you’re doing well. It just means you have a job. If you’re a college graduate working two retail shifts and driving Uber on the weekends just to pay for health insurance, you are "employed" in the eyes of the government. But you’re not prospering. This is the "Gig Economy Trap." We have a lot of jobs, but we don't have enough good jobs that provide a path to retirement or stability.

Mark Zandi, chief economist at Moody’s Analytics, has often noted that consumer sentiment is deeply tied to the "cost of life" rather than just the availability of work. If you have to work 60 hours a week to live the life your parents lived in 40 hours, the economy is failing you. Period.

The Shadow of Consumer Debt

We are currently living on plastic.

Total U.S. household debt hit record highs recently. As prices went up, Americans didn't stop spending—they just started swiping. Credit card balances are soaring, and with interest rates at 20% or higher, that debt is becoming a monster.

- Credit Card Delinquencies: They’re rising, especially among younger borrowers.

- Auto Loans: Have you seen the price of a used Ford F-150 lately? It's insane. People are taking out 7-year loans just to afford a car to get to work.

- Student Loans: The pause ended, payments restarted, and suddenly billions of dollars left the consumer economy and went back to the Treasury.

When you’re paying $400 a month in interest alone, you don't care if the GDP grew by 2.5% last quarter. You’re broke.

💡 You might also like: GA 30084 from Georgia Ports Authority: The Truth Behind the Zip Code

Greedflation vs. Reality

There’s a lot of debate about whether companies are just hiking prices because they can. Some call it "Greedflation." While it's true that corporate profits hit record highs during the post-pandemic recovery, it’s also true that supply chains were genuinely messed up.

But here’s the kicker: even when the supply chains fixed themselves, the prices didn’t drop. Companies realized that people were "used" to paying more. If you’re a CEO and you see that people will pay $18 for a fast-food meal, why would you ever lower it back to $12? This creates a permanent floor for high prices that crushes the average household budget.

The Perception Gap: Why Experts and Regular People Disagree

If you ask an economist why is the american economy so bad, they might actually argue with you. They’ll point to real wage growth and the "soft landing" the Fed achieved. They see a macro success story.

But you see a micro disaster.

Economists look at averages. If Elon Musk walks into a bar, the average person in that bar is a billionaire. But nobody else can buy a drink. The "average" wealth in America is skewed by the top 10% who own the vast majority of stocks and real estate. If you don't own assets, you aren't feeling the "growth." You’re just feeling the heat.

Practical Steps to Navigate This Mess

Complaining about the Fed won't pay the rent. Since the macroeconomy isn't changing tomorrow, you have to play defense.

📖 Related: Jerry Jones 19.2 Billion Net Worth: Why Everyone is Getting the Math Wrong

First, audit your "Subconscious Spending." During the low-interest-rate years, we all got lazy with subscriptions and convenience fees. DoorDash is essentially a tax on your future self. If the economy feels tight, the easiest "raise" you can give yourself is cutting the digital bleed.

Second, look at your debt structure.

If you're carrying a balance on a card with 24% APR, that is an emergency. Look into balance transfer cards or personal consolidation loans if your credit is still decent.

Third, focus on "Skill Stacking." In a weird economy, the only thing you truly own is your ability to solve problems. The traditional 9-to-5 isn't the safety net it used to be. Whether it’s learning a trade, getting a certification in a high-demand tech field, or starting a side hustle that actually scales, you need multiple streams.

Fourth, change your housing expectations. This is the hard one. The "big house in the suburbs" might be a 10-year goal now instead of a 2-year goal. House hacking—renting out a room or buying a duplex—is becoming a necessity for the middle class to build equity.

The Reality of 2026

The American economy isn't "bad" in a way that means it's collapsing. It’s "bad" because it’s transitioning into something that favors those who already have money while making it harder for everyone else to catch up. It’s a K-shaped recovery.

To survive it, you have to stop waiting for prices to "go back to normal." This is the new normal. Adjusting your budget, focusing on high-value skills, and being ruthless with your debt are the only ways to bridge the gap between the government's sunny charts and your actual bank balance.

Stay skeptical of the headlines. Focus on your own balance sheet. The macro is out of your control, but your micro is where the win happens.

Actionable Next Steps:

- Calculate your Personal Inflation Rate: Compare your total monthly expenses from two years ago to today. If your income hasn't grown by that same percentage, you need to negotiate a raise or find a new role immediately.

- Move Cash to High-Yield Accounts: If you have any savings in a traditional big-bank savings account, you’re losing money. Rates are still high enough that a High-Yield Savings Account (HYSA) can act as a small "inflation shield."

- Inventory Your Assets: If you have a car with positive equity that you don't need, or clutter you can sell, liquidate it now. Cash is king when the economy feels uncertain.