You're sitting there, third cup of coffee going cold, staring at a simulation about deferred tax assets that feels like it was written in ancient Greek. It’s the classic candidate’s dilemma. Honestly, looking at cpa exam example questions is usually the moment where the reality of the 14-hour-per-week study grind finally hits you. It isn't just about knowing the math; it’s about surviving the tricks.

The American Institute of Certified Public Accountants (AICPA) isn't exactly trying to hide the ball, but they aren't making it easy either. Most people think they just need to memorize some formulas and call it a day. Wrong. In reality, the exam is designed to test your "higher-order skills," which is basically just fancy talk for "can you spot the trap we hid in paragraph three?"

👉 See also: Why Your Next Coach Might Get Hired Over a Cup of Coffee

The Brutal Reality of Audit Evidence Questions

Audit (AUD) is often the sleeper hit of the CPA exam. Not "hit" as in popular, but "hit" as in it knocks you sideways because the questions feel so subjective. When you look at cpa exam example questions for AUD, you’ll notice something annoying. Frequently, all four answers are technically "correct" in the real world. But the AICPA wants the most correct answer or the one that happens first in the sequence of an audit.

Let’s look at a common scenario. Say you’re testing for the existence of accounts receivable. An example question might ask whether you should vouch from the ledger to the shipping documents or trace from the shipping documents to the ledger. If you mix up "vouching" and "tracing," you’re done.

Vouching goes backward (existence). Tracing goes forward (completeness). It’s a tiny distinction that kills pass rates every single year. Most candidates spend way too much time memorizing the names of the reports and not enough time understanding the "flow" of a transaction. If you don't know where the paper starts, you can't possibly know where it's supposed to end up.

Why BEC Disappearing Changed the Game

The 2024 CPA Evolution initiative basically nuked the old BEC (Business Environment and Concepts) section and replaced it with three disciplines: BAR, ISC, and TCP. This changed the landscape of cpa exam example questions overnight. If you’re looking at old materials from 2022, you’re essentially studying for a test that doesn't exist anymore.

BAR (Business Analysis and Reporting) is basically FAR on steroids. It takes all the complex stuff—pensions, leases, hedge accounting—and cranks it up. If you see a practice question about a complex lease modification and it feels like it belongs in a PhD program, it’s probably a BAR question.

✨ Don't miss: Why the Cemex Brooksville South Cement Plant Actually Matters for Florida

On the flip side, ISC (Information Systems and Controls) is much more about IT governance and SOC reports. The questions here aren't about "math." They’re about logic. You might get a task-based simulation (TBS) where you have to look at a list of internal controls and decide which one is "redundant" or "missing." It’s less about being a human calculator and more about being a detective.

The Mental Trap of FAR Calculations

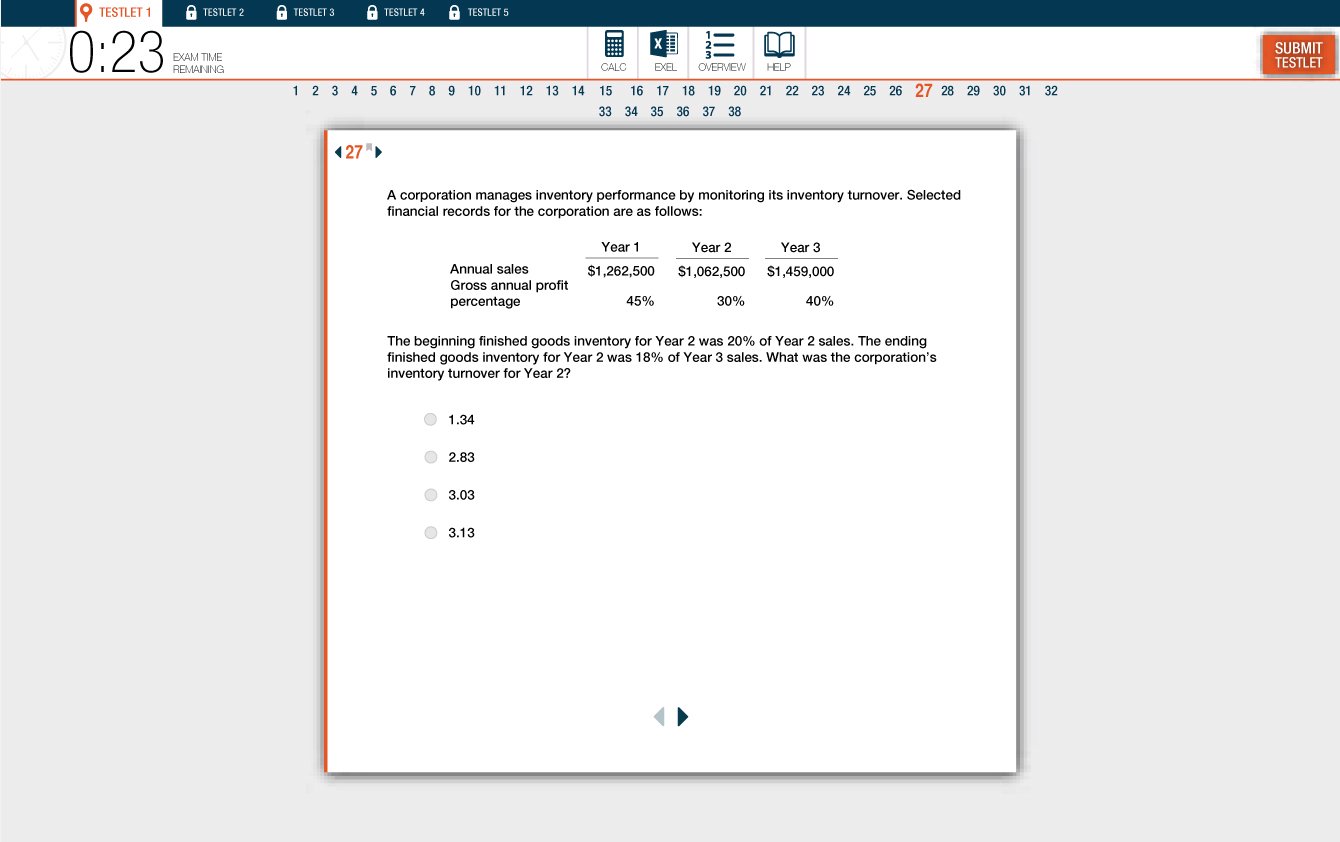

Financial Accounting and Reporting (FAR) is the beast. Everyone knows it. But the secret to tackling FAR cpa exam example questions isn't knowing every single GAAP rule. It’s time management.

I’ve seen brilliant people—straight-A students—fail FAR because they spent 15 minutes on a single multiple-choice question about consolidated financial statements. You can’t do that. You have to be okay with "guessing and moving."

Consider a typical FAR question on Depreciation.

- Asset cost: $100,000

- Salvage value: $10,000

- Life: 5 years

- Scenario: The company switches from Double Declining Balance to Straight Line in Year 3.

A lot of practice questions will try to trip you up on whether this is a "change in accounting principle" (which requires retrospective restatement) or a "change in estimate" (which is prospective). Hint: Changing a depreciation method is handled as a change in estimate. If you start trying to rewrite the Year 1 and Year 2 books, you’ve already lost the battle. You’re doing work the question didn't ask for.

Task-Based Simulations: Where Dreams Go to Die

Multiple-choice questions (MCQs) are the appetizer. The Task-Based Simulations (TBS) are the main course, and they are usually overcooked and hard to swallow. A typical TBS provides you with 5 to 10 "exhibits"—emails, invoices, memos, and board meeting minutes.

You have to synthesize all that junk to fill out a tax form or an adjustment worksheet. The mistake most people make when practicing cpa exam example questions in a TBS format is reading all the exhibits first. Don't do that. You’ll forget everything by the time you get to the actual data entry.

Read the requirements first. Know what you’re looking for. If the simulation asks for the "basis of the distributed property," specifically look for the partner's basis and the FMV of what they received. Ignore the fluff about the company’s new logo or the CEO’s vacation.

Tax (REG) and the Law of Small Details

Regulation (REG) is weirdly specific. You’ll find cpa exam example questions that hinge entirely on whether a taxpayer is "active" or "passive" in a rental activity.

For instance, the $25,000 offset for rental real estate losses sounds simple. But wait—there’s a phase-out. Once your Adjusted Gross Income (AGI) hits $100,000, you start losing that deduction. By $150,000, it’s gone. If a practice question gives you a taxpayer with an AGI of $160,000 and asks for their deductible loss, and you calculate the full $25,000, you’ve fallen for the trap. The answer is $0.

It’s these "thresholds" that make REG a nightmare. You have to memorize numbers that change every few years with inflation. Honestly, it feels a bit like hazing. But that's the profession.

How to Actually Use Example Questions to Pass

Stop using practice questions to see what you know. Use them to see how the exam thinks.

When you get a question wrong, don't just read the explanation and say "oh, okay." Write down why you fell for the wrong answer. Did you misread "not" as "now"? Did you forget to prorate for a half-year convention?

👉 See also: Ramcides HR Tamil Nadu: What Most People Get Wrong

- Do questions in small batches. Doing 100 questions at once is useless. Your brain turns to mush after 20. Do 10, review them deeply, then do 10 more.

- Focus on the "why," not the "what." If you memorize that the answer is "C," you haven't learned anything. If you understand that "C" is the answer because of the Revenue Recognition principle, you’ve actually studied.

- Simulate the environment. No music. No phone. No snacks. The CPA exam is a test of endurance as much as knowledge. If you only practice in 15-minute bursts, you're going to crash during the four-hour actual exam.

The AICPA's own website actually has a "sample test" for each section. It’s the most accurate version of the software you’ll use on test day. Use it. Not for the content, but for the interface. Knowing how to use the built-in spreadsheet tool or the authoritative literature search can save you 10 minutes of panic.

What Most People Get Wrong About Practice Scores

I’ve talked to dozens of candidates who were scoring 90% on their review software (like Becker, UWorld, or Ninja) but then failed the actual exam. How? Because they memorized the cpa exam example questions in the software.

If you see the same question three times, you aren't "learning" the material; you're recognizing a pattern. This is why you need to find fresh sources of questions. If you’re using one main course, maybe buy a "test bank" from a different provider for the final two weeks of your review. It forces your brain to stop relying on muscle memory and start relying on actual accounting logic.

Moving Toward the Finish Line

You shouldn't aim to be an expert in everything. Aim to be "dangerously competent" in most things. The CPA exam is a game of points. You don't need a 100; you need a 75.

If you’re struggling with a specific topic—like Treasury Stock or Section 1231 gains—don't let it paralyze you. If you get 80% of the other questions right, you can afford to whiff on a weirdly specific simulation. The goal is to accumulate enough points across the board to cross that 75-mark finish line.

The journey through these cpa exam example questions is basically a rite of passage. It sucks. It’s meant to. But once you start seeing the patterns—once you see the "trap" before you even finish reading the question—that's when you know you’re ready.

Actionable Next Steps for Your Study Sessions:

- Download the AICPA Blueprints: This is the literal map of what is on the exam. If a topic isn't in the blueprints, it won't be in the questions. Stop over-studying "extra" material.

- Audit your mistakes: Spend more time reviewing the questions you got wrong than doing new questions. If you don't understand your errors, you're doomed to repeat them.

- Master the "Authoritative Literature" tool: In the simulations, you often have access to the actual tax code or GAAP rules. If you know how to search this effectively, you can find the answer to questions you haven't even studied.

- Schedule your "Brain Dump": Practice writing down your key formulas (like the Debt-to-Equity ratio or the mnemonic for the fundamental qualities of financial info) on a piece of paper in under two minutes. You'll do this the second you sit down at the testing center.