So, you’re staring at a stack of benefit folders. Or maybe you're scrolling through the Healthcare.gov marketplace and the same blue symbols keep popping up everywhere. It’s almost impossible to talk about the American medical system without talking about Blue Cross and Blue Shield medical insurance.

It's massive. It’s also confusing.

Most people think of "The Blues" as one giant company headquartered in a glass skyscraper somewhere in DC. That’s actually wrong. It’s actually a federation of 33 independent, locally operated companies. They share a brand, but they don’t always share the same rules. If you have Blue Cross in California (Anthem), it’s a completely different animal than having it in Michigan or Massachusetts.

This matters because your experience depends entirely on your zip code.

What’s the Deal With the Two Different Logos?

Have you ever noticed the logo is actually two separate things? You’ve got the cross and you’ve got the shield. This isn't just fancy graphic design; it’s a relic of how American healthcare used to be split down the middle.

Back in 1929, Justin Ford Kimball at Baylor University Hospital started a plan to help teachers pay for hospital stays. That became Blue Cross. It was specifically for the "bricks and mortar" of the hospital. Then, in the late 30s, the "Shield" part popped up in the Pacific Northwest to cover the actual doctors' bills. They didn't even officially merge until 1982.

Today, they cover roughly one in three Americans. That’s 115 million people.

The Network Effect is Real

When you’re looking at Blue Cross and Blue Shield medical insurance, you’re basically buying access. That’s the "product." Because they’ve been around since the Great Depression, they have the deepest roots in almost every hospital system.

💡 You might also like: How to take out IUD: What your doctor might not tell you about the process

Honestly, the biggest reason people stick with them is the "BlueCard" program.

If you travel or have a kid away at college, this is huge. Most insurance companies have "pockets" of coverage. You leave your state, and suddenly you’re "out of network" and facing a $5,000 bill for a simple ER visit. BlueCard is the backend tech that lets a doctor in Maine treat a patient from Arizona as if they were local. It’s the closest thing we have to a unified national network in a fragmented private system.

But it isn’t always perfect.

Why Some Doctors Give You the Side-Eye

Even with that huge reach, you’ll find some specialists who refuse to take Blue Cross. Why? It usually comes down to the "reimbursement rate."

Since Blue Cross is the 800-pound gorilla in the room, they have massive leverage. They tell a doctor, "We’ll pay you $80 for this visit." The doctor might want $150. If the doctor says no, they lose access to those 115 million members. It’s a power struggle. Sometimes, the doctor just opts out. This is why you always—and I mean always—need to check the specific provider directory for your specific plan suffix (like PPO, EPO, or HMO) before you book that specialist.

Understanding the Plan Tiers (Bronze, Silver, Gold)

The "metal" tiers can feel like a scam if you don't do the math.

- Bronze: You pay a tiny monthly premium. But if you actually get sick? You’re paying thousands out of pocket before the insurance kicks in a dime. It’s "catastrophic" coverage. Basically, it’s for people who bet on staying healthy.

- Silver: The middle ground. This is where most people land because of "cost-sharing reductions" if you qualify based on income.

- Gold/Platinum: You pay a fortune every month. But when you go to the doctor, you might only pay a $20 copay.

If you have a chronic condition—diabetes, asthma, or you're planning a surgery—the Gold plan is usually cheaper in the long run. If you’re a 24-year-old gym rat who hasn't had a cold in three years, Bronze is your friend.

📖 Related: How Much Sugar Are in Apples: What Most People Get Wrong

Medicare Advantage and the "Blue" Twist

For the 65+ crowd, Blue Cross and Blue Shield medical insurance is a major player in Medicare Advantage (Part C).

Standard Medicare (the red, white, and blue card from the government) has gaps. It doesn't cover dental. It doesn't cover vision. It doesn't have an out-of-pocket maximum.

Companies like Florida Blue or Horizon Blue Cross Blue Shield of New Jersey package everything together. They often add "silver sneakers" gym memberships or grocery allowances. The catch? You have to stay in their network. If you have Original Medicare, you can see any doctor in the country who takes Medicare. With a Blue Cross Medicare Advantage plan, you’re often locked into a specific region.

The "Not-for-Profit" Myth

This is a sticky point. Historically, the Blues were non-profits. They were seen as "insurers of last resort."

That changed in the 90s.

Today, some of the biggest "Blue" companies are massive, for-profit corporations. Elevance Health (formerly Anthem) is a publicly traded company on the NYSE. They have shareholders. They want profits. Others, like Blue Cross and Blue Shield of Louisiana or Alabama, have stayed closer to their non-profit roots, though that’s becoming rarer as the industry consolidates.

Does it change your coverage? Not necessarily. But it does change how they handle rate hikes and where their extra cash goes at the end of the year.

👉 See also: No Alcohol 6 Weeks: The Brutally Honest Truth About What Actually Changes

Real World Example: The "Prior Authorization" Headache

Imagine you need an MRI. Your doctor says you need it. You think, "Great, I have Blue Cross, I'm covered."

Not so fast.

Blue Cross and Blue Shield medical insurance—like almost all major carriers—uses a process called Prior Authorization. They use third-party companies or internal algorithms to decide if that MRI is "medically necessary." They might tell you to try physical therapy for six weeks first.

It’s frustrating. It feels like a bean counter is practicing medicine without a license.

To win this fight, your doctor’s office has to be aggressive. They have to submit the right "ICD-10" codes and clinical notes. If you get a denial, don't just give up. Over 50% of insurance denials that are appealed actually get overturned. Most people just don't bother to appeal.

How to Actually Pick a Plan

Don't just look at the premium. That’s the biggest mistake people make.

- Check the "Formulary": This is a fancy word for the list of drugs they cover. If you take a specific brand-name medication, search the Blue Cross formulary for your state. If it's a "Tier 4" or "Non-Preferred" drug, you could be paying hundreds of dollars even with insurance.

- Look for the PPO vs. HMO distinction: If you want to see a specialist without asking a primary care doctor for permission, you need a PPO. If you want the lowest price and don't mind the "gatekeeper" model, go HMO.

- Verify the Hospital: Just because a hospital is "Blue Cross" doesn't mean every doctor inside that hospital is. The anesthesiologist or the radiologist might be out-of-network. This is called "surprise billing." While the No Surprises Act (2022) has helped, it's still a mess to navigate.

Actionable Next Steps

If you are looking at Blue Cross and Blue Shield medical insurance right now, here is what you should do:

- Download the App: Every local Blue company has its own app (like "MyBlue" or "Sydney Health"). It’s the fastest way to see your digital ID card. You don't want to be at the pharmacy at 9:00 PM without it.

- Sync Your Health Savings Account (HSA): If you pick a High Deductible Health Plan (HDHP), make sure you actually open the HSA account. It’s triple-tax-advantaged money.

- Check for "Teledoc" Benefits: Most Blue plans now offer $0 or low-cost virtual visits. For a sinus infection or a quick prescription refill, this saves you four hours in a waiting room.

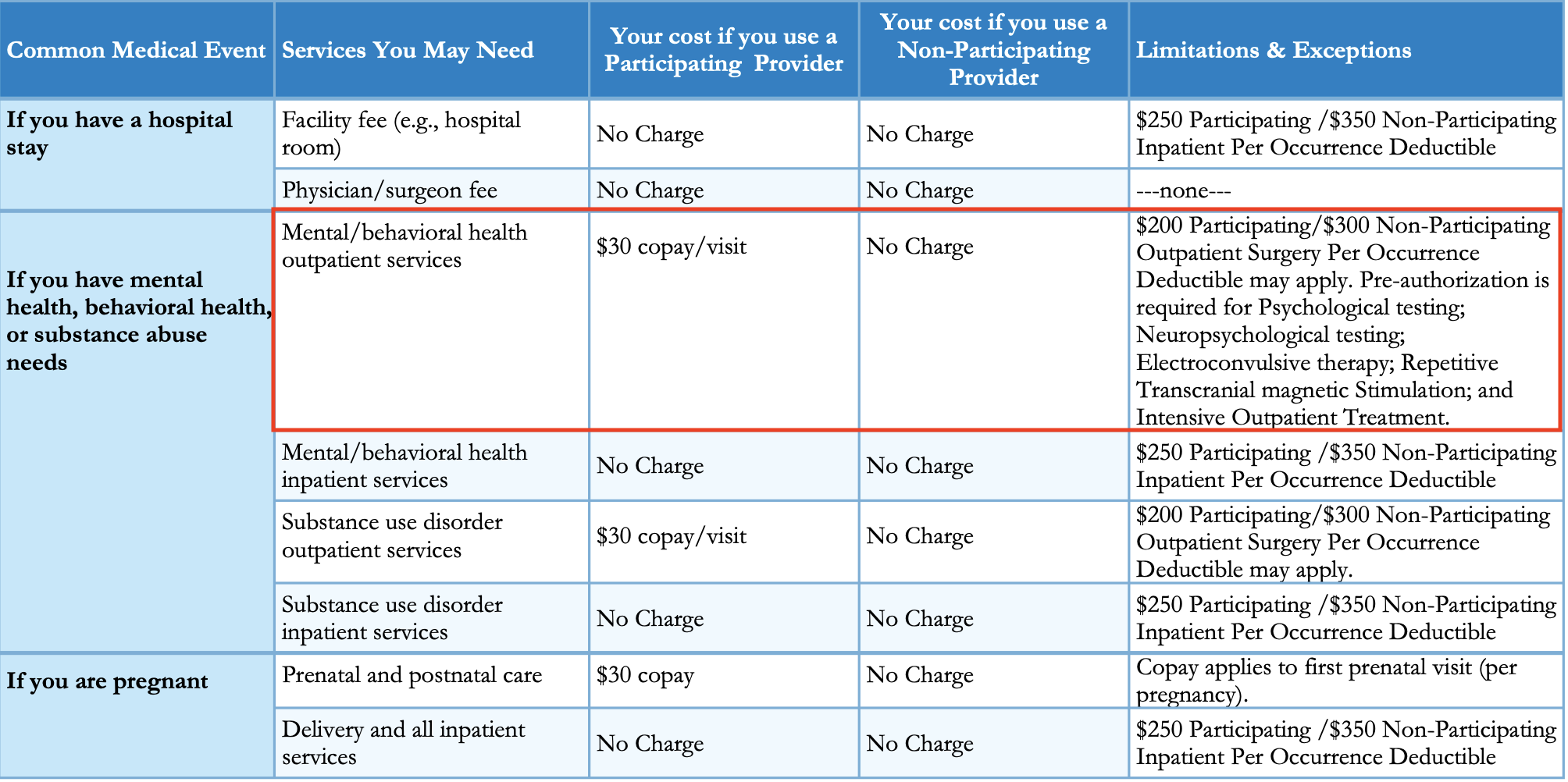

- Review the Summary of Benefits and Coverage (SBC): This is a standardized 8-page document. Every plan has one. It uses the same language so you can compare a Blue plan against a UnitedHealthcare or Aetna plan side-by-side. Look at the "Examples" on the last page—they show you exactly what a baby delivery or a broken foot would cost under that specific plan.