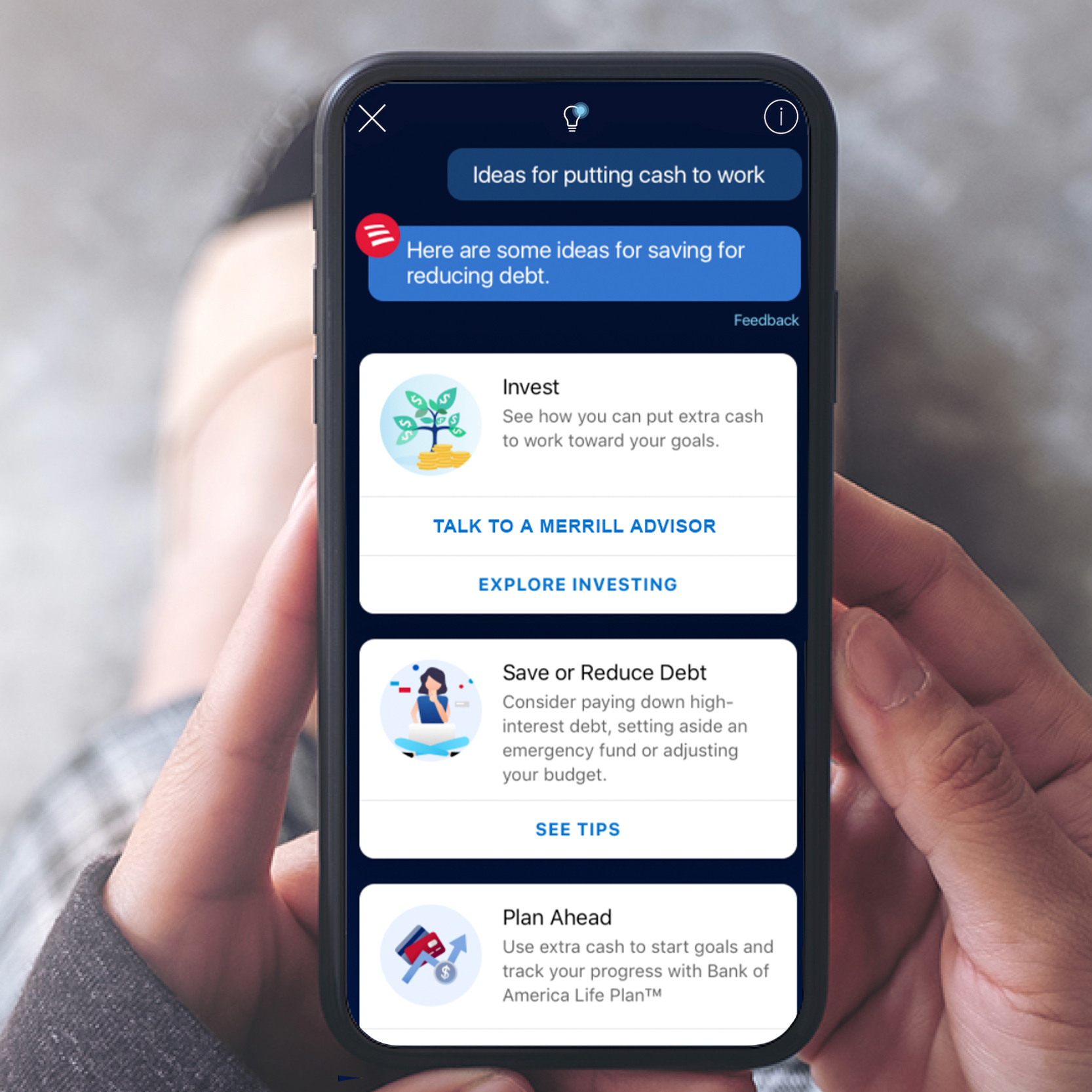

You’re lying in bed at 11:00 PM and suddenly remember that weird $45 charge from three weeks ago. You could log in, scroll through endless PDF statements, and squint at merchant codes. Or, you could just tell your phone, "Show me my transactions at Starbucks last month." That’s where Bank of America Erica comes in. Honestly, when BofA first launched this virtual assistant back in 2018, people were skeptical. We’d all been burned by those clunky "how can I help you?" chatbots that basically just link you to a FAQ page you’ve already read. But Erica has quietly turned into something much more sophisticated than a simple search bar with a voice. It’s a massive experiment in predictive banking that’s actually working.

Banks are notorious for being slow. They’re legacy institutions built on systems from the 80s. So, seeing a major player like Bank of America commit so heavily to an AI-driven interface was a gamble. It wasn’t just about being trendy. They needed a way to handle the billions of digital interactions happening every year without exploding their call center budget. Now, years later, the data shows that millions of people use it every single day. It’s not just for checking balances anymore; it’s becoming a legitimate financial coach that catches things you might miss.

What Most People Get Wrong About Bank of America Erica

People often think Erica is just Siri for your bank account. It’s not. While Siri is great for setting timers or checking the weather, Bank of America Erica is integrated directly into the bank’s core processing engine. This means it has a level of "contextual awareness" that a general AI lacks. It knows your patterns. If your gym membership suddenly doubles in price, Erica doesn't just process the payment—it flags it.

- It tracks your recurring subscriptions so you can see where your money is leaking.

- The assistant can find your routing number in two seconds, saving you from digging through the "About" section of the app.

- It monitors for duplicate charges, which happens more often than most of us realize.

One of the coolest, and maybe slightly creepy, features is the proactive notification system. Let's say you have a bill due next Tuesday, but your current balance won't cover it based on your typical spending. Erica can actually ping you and say, "Hey, you might run short." That’s a huge shift from the old-school banking model where the bank would just wait for you to overdraw and then hit you with a $35 fee. It’s a shift toward "wellness," which is a word banks love to use lately, but in this case, it actually has some teeth.

The Technology Under the Hood

Underneath the slick interface, Bank of America Erica uses Natural Language Processing (NLP). This is what allows it to understand that "How much did I spend at Target?" and "Target transactions" mean the exact same thing. According to Bank of America's own technical insights, the system has been trained on millions of different ways customers ask for things. They’ve spent years refining the "intent recognition" so that the AI doesn't get confused by slang or slightly garbled voice commands.

✨ Don't miss: Syrian Dinar to Dollar: Why Everyone Gets the Name (and the Rate) Wrong

It’s also important to realize that this isn't just one static program. It's constantly learning. When the pandemic hit in 2020, BofA had to rapidly update Erica’s "brain" to understand questions about CARES Act stimulus checks and mortgage deferments. It showed the world that digital assistants are only as good as the speed at which their parent company can update their knowledge base.

Why Privacy Advocates Are Still Watching Closely

We have to talk about the elephant in the room: data. When you use Bank of America Erica, you are giving the bank permission to analyze every single cent that moves through your life. While the bank maintains that this data is used to "personalize your experience," privacy experts often point out that this creates a incredibly detailed profile of your habits.

Are they selling this info? Bank of America says no, but they are definitely using it to market their own products to you. If Erica sees you’re paying a high interest rate on a credit card at another bank, don’t be surprised if you see a "special offer" for a BofA balance transfer. It’s a double-edged sword. You get convenience and "financial coaching," but the bank gets a 360-degree view of your financial soul.

The Limits of Virtual Assistants

Even with all the updates, Erica isn't human. If you have a complex problem—like a disputed fraud claim involving a third-party vendor and a shipping delay—Erica is going to struggle. There’s a limit to what an AI can do before it needs to hand you off to a human being. The trick is how seamless that handoff is. BofA has tried to make it so the human representative can see exactly what you were talking to Erica about, so you don't have to repeat your whole life story once you get a person on the phone.

🔗 Read more: New Zealand currency to AUD: Why the exchange rate is shifting in 2026

- Standard queries like "What's my FICO score?" work 100% of the time.

- Middle-ground tasks like "Transfer $50 to savings every Friday" are pretty reliable.

- Complex emotional or nuanced problems still require the "Call Us" button.

Practical Ways to Use Erica Right Now

If you're already a BofA customer, you're probably only using about 10% of what the tool can do. Honestly, most of us just use it to find the nearest ATM. But if you want to actually get some value out of it, try these specific triggers.

First, ask for your "Spend Path." This is a visual breakdown of where your money went over the last month compared to previous months. It’s a reality check. Second, use the "Refund Watch." You can tell Erica to notify you when a specific refund hits your account—like that $200 jacket you sent back to Nordstrom. No more checking your app every three hours to see if the money is back.

Another solid move is checking your "Rewards Balance." If you have a Bank of America credit card, you’re probably sitting on cash back or points. Just ask, "How many points do I have?" and it’ll show you the dollar value. It's a small thing, but it prevents you from leaving free money on the table.

Looking Ahead: The Future of AI in Banking

The next step for Bank of America Erica is likely going to be even more "generative." With the explosion of Large Language Models (LLMs), expect the conversations to feel less like a menu and more like a real talk with a financial planner. Imagine asking, "Can I afford a $500/month car payment if I also want to save for a wedding in 2027?" and having the AI run a thousand simulations in the background to give you an honest answer.

💡 You might also like: How Much Do Chick fil A Operators Make: What Most People Get Wrong

We aren't quite there yet, but the trajectory is clear. The bank wants to move away from being a place where you just "store" money and toward being an active participant in your financial life. Whether that's a good thing depends entirely on how much you trust a mega-bank to have your best interests at heart.

Actionable Insights for Users:

- Audit Your Subscriptions: Type "recurring charges" into Erica today. You will almost certainly find a $9.99/month service you forgot you signed up for three years ago. Cancel it through the merchant immediately.

- Set Up "Low Balance" Alerts: Instead of waiting for the bank's default alerts, ask Erica to notify you when your balance hits a specific number that makes you uncomfortable, like $500 or $1,000.

- Monitor Your Credit Score: Use the voice command "Show me my FICO score" once a month. It’s a free service for BofA customers, and Erica makes it a two-second habit instead of a chore.

- Check for Duplicate Charges: Periodically ask, "Do I have any duplicate charges?" to catch glitches at restaurants or gas stations that might have swiped your card twice.

- Search for Specific Merchants: If you need to know how much you spent on "Amazon" over the last year for tax or budgeting reasons, just ask. It beats manual spreadsheet work every time.

Managing money is usually boring and stressful. Using tools like Erica doesn't make the math change, but it does lower the friction of paying attention. And in the world of personal finance, paying attention is usually half the battle.