So, you're looking at the calendar and wondering when I can get Medicare. Honestly, it's a bit of a maze. Most people think it’s just a "happy 65th birthday" gift from the government, but the timing is actually way more nuanced than that. If you mess up the window, you’re looking at lifetime penalties. Nobody wants that.

Medicare isn't just one thing; it's a collection of parts—A, B, C, and D—and they all have different entry points depending on your health, your job, and even your birthday.

The Standard Rule: The Magic 65

For the vast majority of us, the answer to when I can get Medicare is tied directly to your 65th birthday. This is your Initial Enrollment Period (IEP). It’s a seven-month window. It starts three months before the month you turn 65, includes your birth month, and ends three months after.

Simple, right? Not quite.

If you sign up in those first three months, your coverage starts the first day of your birthday month. But if your birthday is on the first of the month, Medicare actually views you as having turned 65 the month before. It’s a weird quirk of the Social Security Administration’s logic.

Wait too long—like, signing up in those last three months of the window—and your coverage might be delayed. You don't want a gap in insurance. Medical bills don't take a vacation just because your paperwork is stuck in a processing center in Maryland.

When You Can Get Medicare Early

You don't always have to wait until 65. Life happens. Sometimes it’s unfair.

📖 Related: Your Skin and Bones: Why They Are Breaking Down Faster Than You Think

If you’ve been receiving Social Security Disability Insurance (SSDI) for 24 months, you’re automatically enrolled in Medicare Parts A and B on the 25th month. You don't even have to lift a finger. The red, white, and blue card just shows up in your mailbox.

There are two major exceptions where the 24-month wait is waived entirely:

- ALS (Amyotrophic Lateral Sclerosis): Also known as Lou Gehrig’s disease. Medicare kicks in the very first month your disability benefits start.

- ESRD (End-Stage Renal Disease): If you have permanent kidney failure and need dialysis or a transplant, you can usually get Medicare regardless of your age.

This is a lifeline for people facing massive healthcare costs. It's one of the few areas where the government moves relatively fast.

The "Working Past 65" Dilemma

A lot of people are working longer now. If you're 66 or 67 and still have "creditable" coverage through an employer with 20 or more employees, you might not need to sign up for Part B yet.

But be careful.

"Creditable" is the keyword here. If your employer coverage isn't considered as good as Medicare by the Centers for Medicare & Medicaid Services (CMS), you’ll get hit with a Part B late enrollment penalty later. That penalty is 10% for every 12-month period you could have had Part B but didn't. And that's a "forever" penalty. It stays on your premium for life.

Once you stop working or the insurance ends, you get an eight-month Special Enrollment Period (SEP). Use it. Don't wait.

✨ Don't miss: How Often Should You Have a Massage? What Your Body Actually Needs

Common Myths About Timing

People often get confused about Social Security and Medicare. They are cousins, not twins. You can take Social Security at 62, but you can't get Medicare then (unless you have the disabilities mentioned earlier).

Conversely, you might wait until 70 to claim your maximum Social Security check. You still need to deal with Medicare at 65.

Another big one: "I'm healthy, so I'll wait."

Terrible idea.

Medicare Part A is usually free if you or your spouse worked for 10 years (40 quarters) and paid Medicare taxes. Since it's free, there is almost no reason not to sign up at 65. Part B has a monthly premium—usually around $185 in 2026, though it fluctuates based on inflation and the economy—but skipping it without other coverage is a gamble that rarely pays off.

Breaking Down the Enrollment Windows

Since we aren't doing fancy tables, let's just talk through the periods.

The General Enrollment Period runs from January 1 to March 31 every year. This is for people who missed their initial window. If you sign up then, your coverage starts the following month.

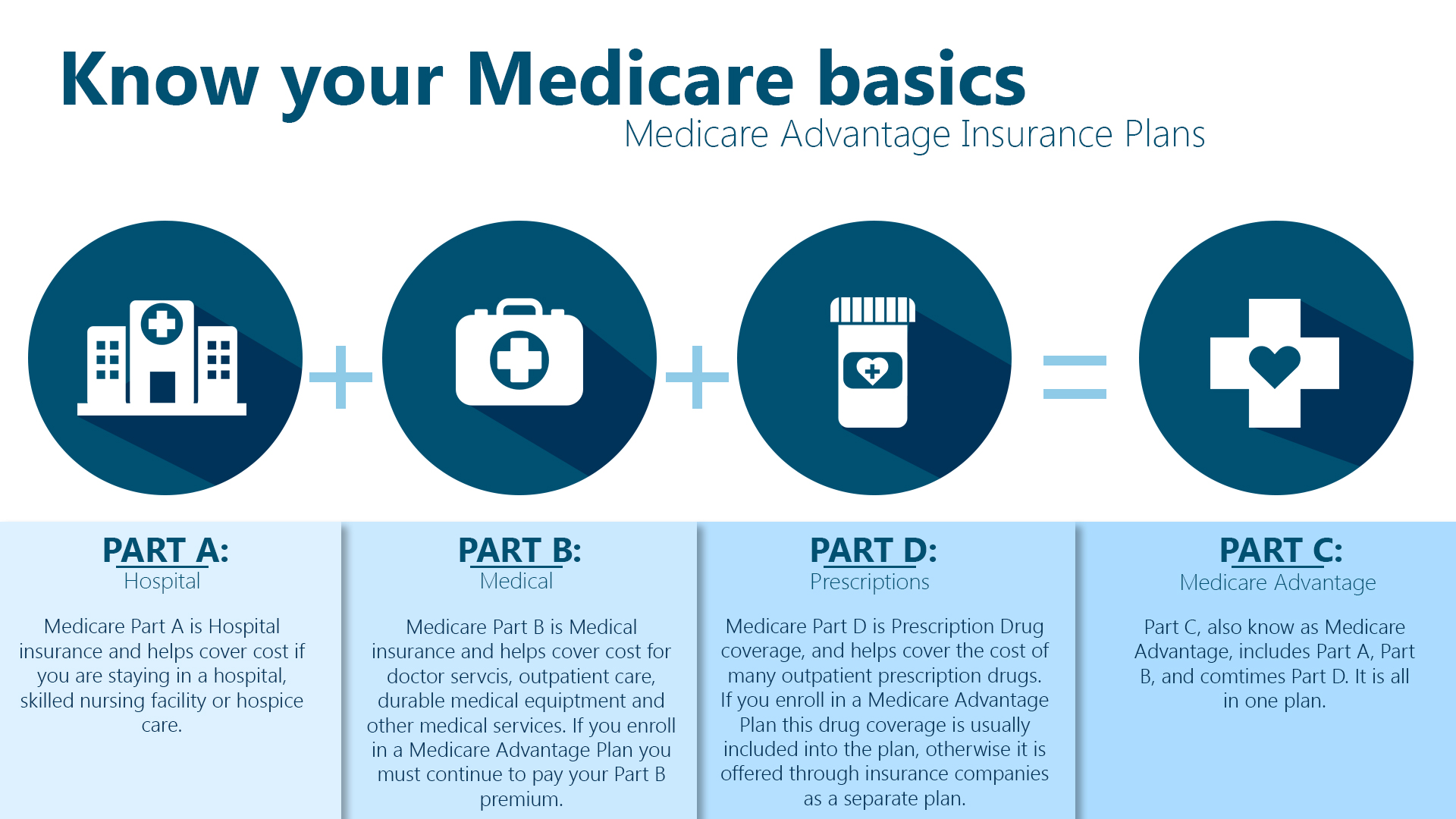

Then there's the Annual Enrollment Period (AEP) from October 15 to December 7. This isn't for getting Medicare for the first time; it's for people already on it who want to switch plans, like moving from Original Medicare to a Medicare Advantage plan (Part C) or changing their Part D drug coverage.

Actionable Steps for Your Timeline

Don't leave this to the last minute.

- Check your records: Log into SSA.gov about six months before you turn 65. Make sure your earnings history is correct. This determines if you get Part A for free.

- Evaluate your current insurance: If you're working, talk to your HR department. Ask them specifically: "Is this coverage primary or secondary to Medicare?" and "Is it considered creditable coverage?" Get that in writing.

- Mark the T-minus 3 months date: Three months before your 65th birthday is the day you can finally answer when I can get Medicare with a definitive "Now."

- Review Part D: Even if you don't take any meds, get a basic Part D plan. If you go years without it and then need it at 75, you'll pay a penalty based on every month you went without.

Medicare is a bit of a beast, but it’s manageable if you respect the deadlines. The government isn't known for its flexibility with dates. If you miss your window, the costs—both in terms of premiums and potential medical debt—can be staggering. Keep your eye on that 65th birthday, but keep your paperwork ready long before the candles are lit.