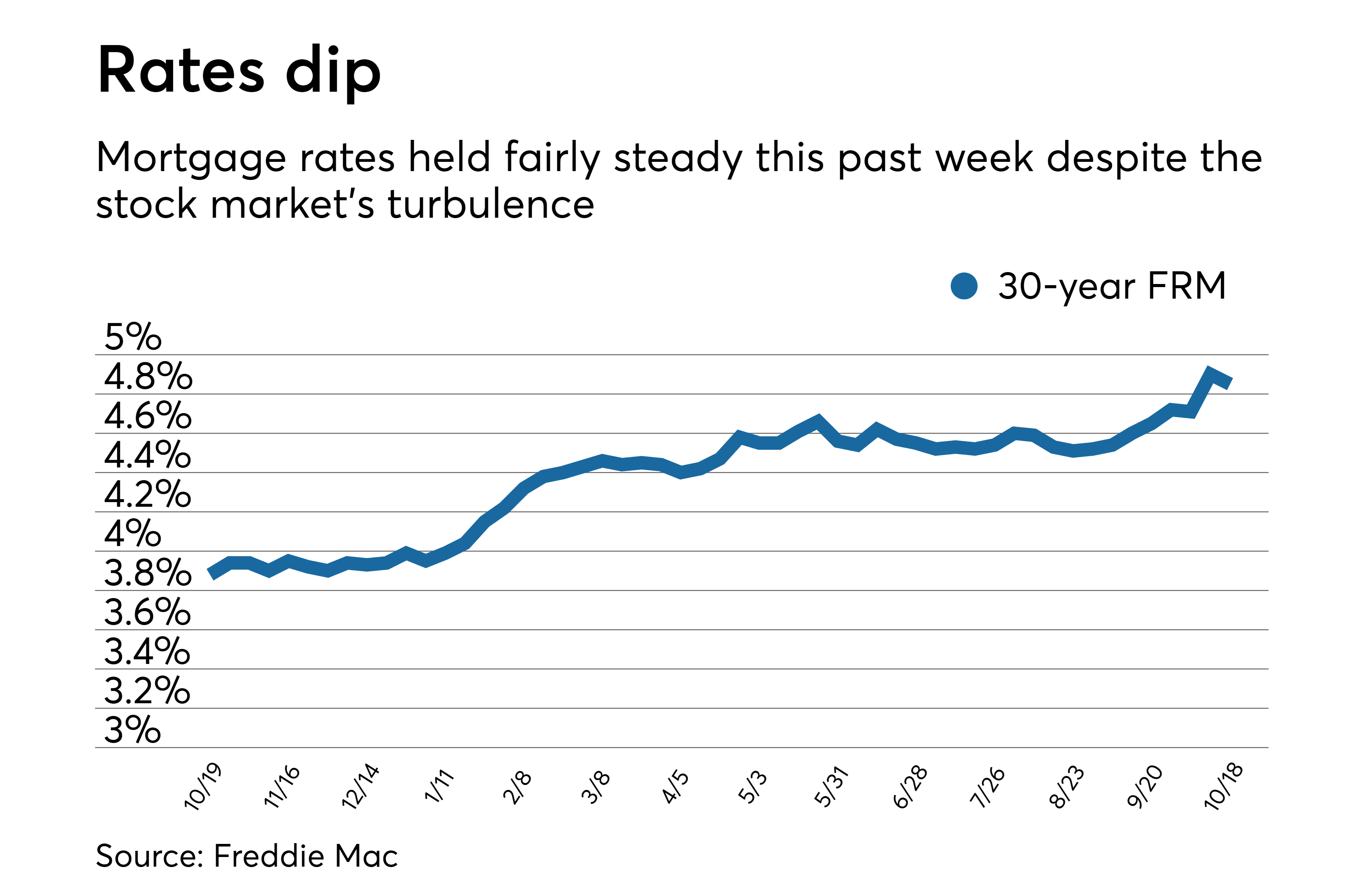

You've probably heard the rumors that the housing market is finally cooling off, but when you look at the actual numbers, it feels like a different story. Honestly, everyone wants to know one thing: what's the mortgage rate now?

If you're checking your phone today, Saturday, January 17, 2026, the national average for a 30-year fixed mortgage is sitting right around 6.11%. Some lenders are quoting closer to 6.18% when you factor in the APR. It’s a bit of a relief compared to those scary 7% or 8% days we saw a year or two ago, but it’s definitely not the 3% "pandemic special" everyone is still nostalgic for.

Basically, we're in this weird middle ground. Rates are down from their peaks, but they aren't exactly "cheap."

The Current Numbers: Breaking Down What's The Mortgage Rate Now

Let's look at the actual data from this week. According to the latest Freddie Mac Primary Mortgage Market Survey released on January 15, the 30-year fixed-rate mortgage averaged 6.06%. That's a decent drop from the 6.16% we saw just a week prior.

If you're more of a "get it over with" type of person and you're looking at a 15-year fixed loan, you're looking at an average of 5.38%.

👉 See also: Why 425 Market Street San Francisco California 94105 Stays Relevant in a Remote World

Here is how the landscape looks across different loan types right now:

- 30-Year Fixed: ~6.11% (National Average)

- 15-Year Fixed: ~5.45%

- 30-Year FHA: ~5.78% (Great for lower down payments, but watch those fees)

- 30-Year VA: ~6.14% (For the veterans, usually better terms)

- 5/1 ARM: ~5.41% (Good if you plan on moving in five years, risky if you don't)

It’s worth noting that if you’re trying to refinance, you’re going to pay a premium. The average 30-year refinance rate is hovering near 6.56%. Lenders are a bit more cautious with refis right now, especially with the economy feeling a little "vibecessionsy."

Why Are Rates Acting Like This?

So, why are we stuck at 6%? It’s a tug-of-war between the Federal Reserve and the bond market.

Last year, the Fed cut rates three times, ending 2025 with a federal funds rate in the 3.50% to 3.75% range. But here’s the kicker: the Fed doesn't actually set mortgage rates. They set the "vibe" for the economy. Mortgage rates are more closely tied to the 10-year Treasury yield.

✨ Don't miss: Is Today a Holiday for the Stock Market? What You Need to Know Before the Opening Bell

Lately, investors have been nervous. We've got a new Fed chair transition looming as Jerome Powell's term wraps up in May 2026. Names like Kevin Hassett and Kevin Warsh are being tossed around, and the market hates uncertainty. When investors are unsure, they demand higher returns on bonds, which keeps your mortgage rate from falling as fast as you'd like.

Also, inflation is being stubborn. It’s better than it was, but it's not "dead" yet.

The "Rate Lock" Dilemma

There's also a supply issue. Millions of homeowners are currently "locked in" at 3% or 4%. If you're one of them, moving and taking on a 6% mortgage feels like a punch in the gut. This keeps inventory low, which keeps home prices high, even if the rates are technically "improving."

Expert Predictions: Will It Get Better?

Ted Rossman over at Bankrate thinks we might see the 30-year fixed-rate fall below 6% for the first time in years later this spring. He's floating the possibility of 5.5% by the end of the year if the economy slows down enough.

🔗 Read more: Olin Corporation Stock Price: What Most People Get Wrong

On the other hand, the Mortgage Bankers Association (MBA) is a bit more conservative, predicting we’ll stay closer to 6.4% for most of 2026. They think the "inflation floor" is higher than people realize.

Fannie Mae is split down the middle, forecasting an end-of-year rate of about 5.9%.

How To Actually Get A Lower Rate Today

Don't just accept the first quote you see on a billboard. If the "average" is 6.11%, that means some people are getting 5.8% and some are getting 6.5%.

- Shop at least three lenders. Seriously. You could save $100 a month just by switching from a big bank to a local credit union.

- Buy down the rate. If you have extra cash, you can pay "points" upfront to lower your permanent interest rate. In 2026, many sellers are actually offering to pay for these points just to get their houses sold.

- Check your credit score. The difference between a 680 and a 740 score right now is roughly 0.5% in interest. That's tens of thousands of dollars over the life of the loan.

- Look at FHA or VA options. If you qualify, these government-backed loans often have lower interest rates than conventional loans, even if the insurance costs are a bit higher.

Next Steps For Your Wallet

Stop waiting for 3% to come back; it's likely not happening in our lifetime. Instead, focus on what you can control.

First, get a pre-approval from at least two different types of lenders—a big national bank and a mortgage broker—to see the "real" rate you qualify for based on your specific credit profile. Second, if you're a current homeowner with a rate above 7.25%, run the math on a refinance today. Even at 6.5%, the monthly savings on a $400,000 loan can be over $300, which usually covers the closing costs in less than two years.

Keep an eye on the next Fed meeting on January 28. If they hold steady, expect rates to stay exactly where they are. If they hint at more cuts, you might want to wait a few weeks before locking in.