Money feels weird lately. You go to the grocery store, grab a carton of eggs and a bag of coffee, and suddenly you’re out $40. It makes you wonder: is everyone else actually keeping up? Or are we all just pretending? When people ask what's the median household income in the us, they aren't usually looking for a dry government spreadsheet. They want to know where they stand in the middle of this "K-shaped" economy we’ve been living through.

Honestly, the numbers might surprise you. According to the latest 2025 and early 2026 data from the U.S. Census Bureau and tracking from institutions like the Dallas Fed, the median household income in the us is roughly $83,730.

Now, that sounds like a decent chunk of change, right? But "median" is the keyword there. It’s the literal middle point. Half of American households make more than that, and the other half make less. It’s a far cry from the "average" (mean) which gets pulled way up by billionaires in Silicon Valley and hedge fund managers in Manhattan.

Why the $83,730 number feels different depending on where you park your car

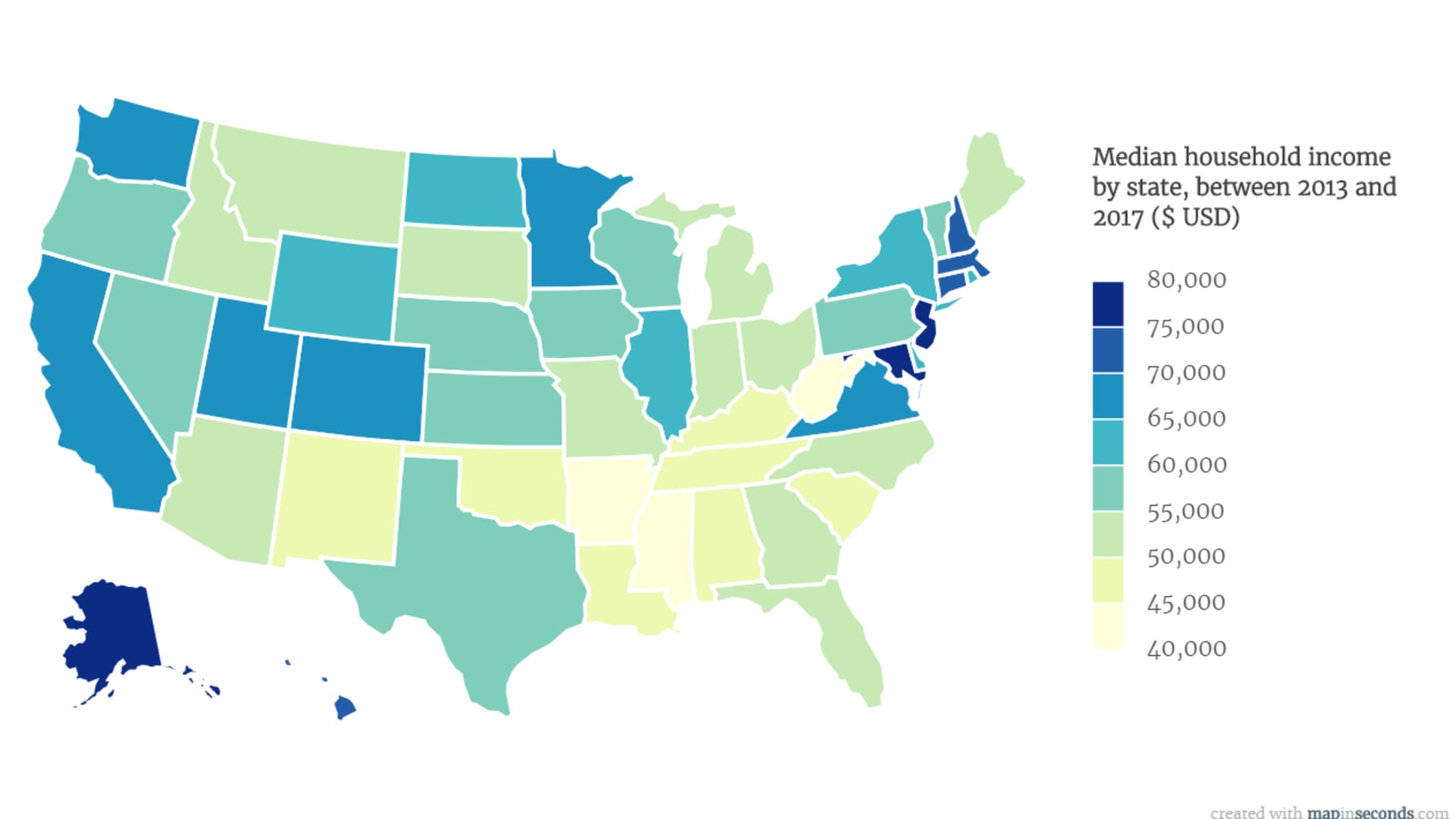

The national number is basically a myth once you cross state lines. You can't compare a paycheck in Jackson, Mississippi, to one in Boston. It’s just not the same life.

If you’re in Massachusetts, the median income is north of $101,000. In Maryland, it’s about $101,652. But head down to Mississippi, and that middle-of-the-pack number drops to around $54,915. That is a massive gap. It explains why a "six-figure salary" is a middle-class struggle in San Francisco but puts you in the top tier in West Virginia.

🔗 Read more: Shangri-La Asia Interim Report 2024 PDF: What Most People Get Wrong

The "Comfort" Gap

There’s a difference between making the median and being "comfortable." Recent 2025 studies by SmartAsset suggest that in places like Hawaii or California, a single adult actually needs over $120,000 just to feel secure. That’s nearly $40,000 more than the national median.

We’re seeing a real squeeze. For the first time in a while, the 2026 housing forecast shows that the typical mortgage payment is finally dipping back below 30% of the median income. It’s a small win, but for most families, it still feels like they're treading water.

What’s actually driving these income shifts in 2026?

It isn't just about hard work. A few big factors have been messing with the math over the last year.

- The Tariff Impact: 2025 saw some pretty heavy-duty tariffs come into play. These acted like a "regressive tax," meaning lower and middle-income families spent a bigger chunk of their paycheck on imported goods that got more expensive.

- The Education Premium: If you have a Bachelor’s degree, the data shows median weekly earnings around $1,559. Without a high school diploma? That drops to about $720.

- Household Composition: Married-couple households are still the highest earners by far. Two incomes are almost a requirement to hit that $83k+ median mark nowadays.

Does race and age play a role?

Kinda. Actually, a lot. Asian households continue to have the highest median income, often exceeding $112,000. Meanwhile, Black households saw a slight dip in the 2024-2025 period, sitting closer to $56,500.

💡 You might also like: Private Credit News Today: Why the Golden Age is Getting a Reality Check

Age is another weird one. You’d think the oldest people make the most, but the peak earning years are actually between 35 and 54. Once people hit 65, the median income drops significantly as they shift to Social Security and fixed pensions.

The 2026 Reality Check: Real vs. Nominal Income

This is where it gets nerdy but important. Your "nominal" income is the number on your W-2. Your "real" income is what that money actually buys.

Between 2023 and 2026, nominal wages went up. People are getting raises. But because inflation (especially in utilities and food) stayed sticky, "real" income for many families has stayed flat. Basically, you’re making more but buying the same amount of stuff.

How to use this data for your own wallet

Knowing that the median household income in the us is roughly $83,730 doesn't change your bank account today, but it does give you leverage.

📖 Related: Syrian Dinar to Dollar: Why Everyone Gets the Name (and the Rate) Wrong

If you are living in a high-cost state like New Jersey or Washington and making less than the state median, you are likely significantly underpaid for your market. Use these numbers. When you go into a salary negotiation, don't just ask for a "raise." Bring the local median data for your industry and education level.

Check your housing-to-income ratio. If your rent or mortgage is eating up more than 35% of your gross income, you are officially "cost-burdened" according to federal standards.

Your Next Steps

- Audit your local market: Go to the Bureau of Labor Statistics (BLS) website and search for your specific "Metropolitan Statistical Area." This gives you a way more accurate picture than a national average.

- Factor in the 2026 inflation forecast: Economists expect inflation to cool to about 2.4% this year. If your annual raise isn't at least 3%, you are technically taking a pay cut.

- Evaluate your household structure: If you're a single-earner household, look into the specific tax credits available in 2026 for your income bracket, as many thresholds were adjusted for inflation last November.

The "middle" is moving faster than it used to. Staying informed is the only way to make sure you aren't left behind in the data.