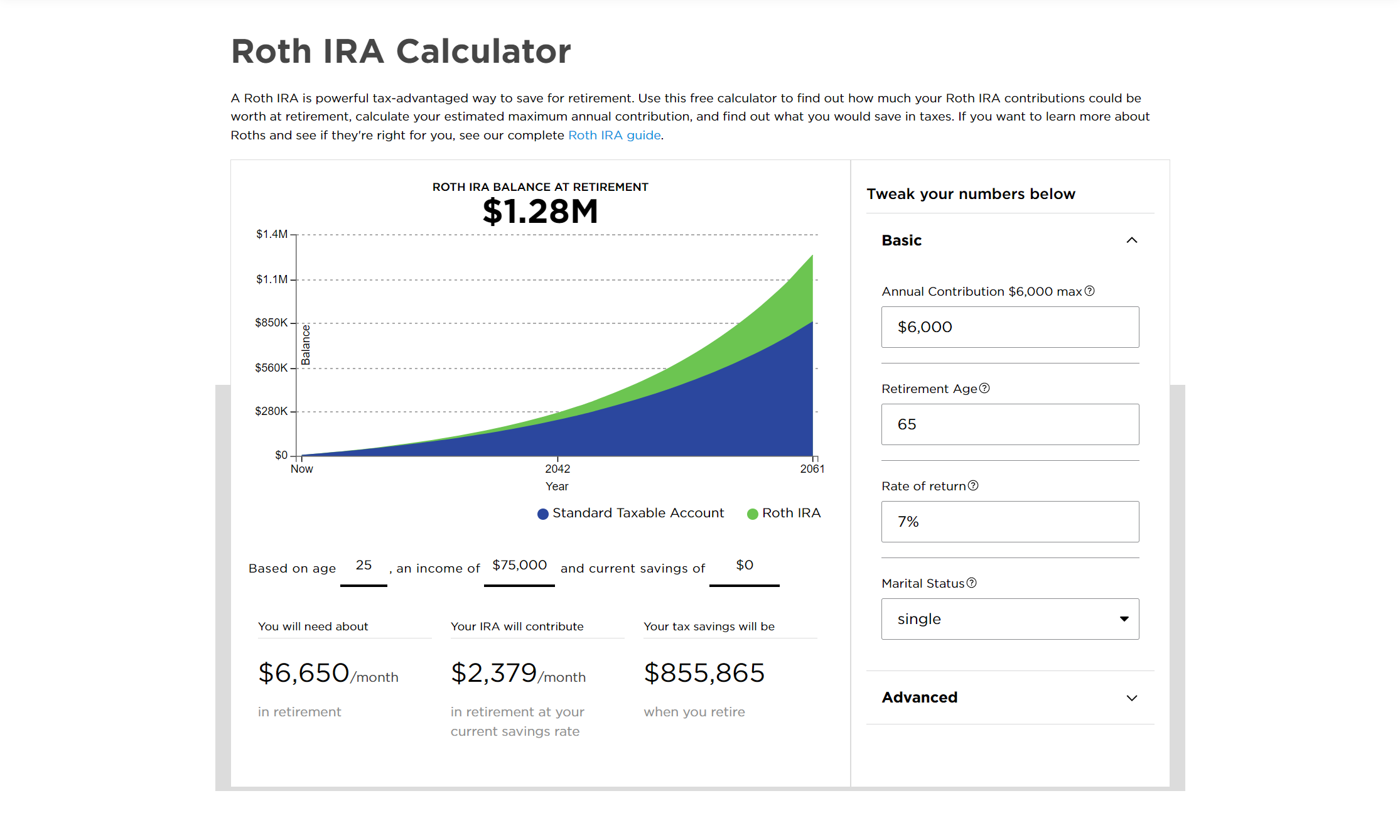

You’ve finally done it. You opened the account, linked your bank, and moved that $7,000 (or $8,000 if you’re over 50) into your Roth IRA. But now comes the part where most people freeze. The money is just sitting there in a "settlement fund," which is basically a fancy way of saying a holding pen that earns next to nothing. Honestly, it's heartbreaking to see people let their cash rot in a money market fund for years because they're terrified of picking the "wrong" thing.

The reality is that figuring out what to invest Roth IRA in isn't about finding a magic stock that will go to the moon. It’s about leveraging the most powerful tax advantage the IRS ever handed us: tax-free growth. Since you’re playing with money that has already been taxed, every penny of profit you make stays yours forever. No capital gains tax. No dividend tax. Nothing. That changes the math on how aggressive you should be.

Most people play it way too safe here. They treat their Roth like a savings account with a lock on it. If you’ve got decades until retirement, that’s a massive mistake.

The Case for Total Market Dominance

If you ask a Boglehead—those disciples of Vanguard founder Jack Bogle—they’ll tell you to keep it simple. They aren't wrong. For the vast majority of people, the best answer for what to invest Roth IRA in is a total stock market index fund. You’re basically buying a tiny slice of every public company in the US.

Think about it. You get Apple, Microsoft, and Amazon, but you also get the scrappy mid-cap companies that might be the giants of 2040. VTSAX (the Vanguard Total Stock Market Index Fund) or its ETF cousin VTI are the gold standards here. Fidelity has FZROX, which literally has a 0% expense ratio. It’s free. You can’t beat free.

But here is the nuance. A total market fund is heavy on tech right now because it's market-cap weighted. If tech slides, you slide. That’s why some folks prefer a "Target Date Fund." These are the "set it and forget it" kings. You pick the year you plan to retire—say, 2060—and the fund automatically shifts from aggressive stocks to boring bonds as you get older.

It’s convenient. But it’s also a bit of a drag on returns for a Roth. Bonds pay interest, which is great, but in a Roth IRA, you usually want the highest-growth assets possible because that's where the tax savings are most explosive. Putting bonds in a Roth is like putting a speed limiter on a Ferrari.

High-Dividend Stocks: The Stealth Wealth Play

There is a specific group of investors who swear by dividend growth investing for their Roth. Why? Because normally, when a company like Realty Income (O) or Johnson & Johnson (JNJ) pays you a dividend, Uncle Sam wants his cut that same year.

💡 You might also like: Wegmans Meat Seafood Theft: Why Ribeyes and Lobster Are Disappearing

In a Roth, those dividends hit your account and get reinvested immediately without the IRS seeing a dime.

This creates a compounding snowball. Imagine holding a REIT (Real Estate Investment Trust). These companies are legally required to pay out 90% of their taxable income to shareholders. They are notorious for being "tax-inefficient" in a regular brokerage account. But in a Roth? They are a powerhouse. You’re capturing high-yield income and letting it compound tax-free for thirty years.

Just don't go chasing yield for the sake of yield. A company paying 12% is usually a company in trouble. Stick to the "Dividend Aristocrats"—companies that have raised their payouts for 25 consecutive years. It’s boring. It works.

Why Your Age Changes Everything

Your timeline is the only thing that matters.

If you’re 22, your Roth IRA should probably look like a caffeinated teenager. You can afford the volatility of the Nasdaq-100 (QQM) or even some aggressive small-cap value funds like AVUV. Small-cap value has historically outperformed the S&P 500 over very long stretches, though it can be a gut-wrenching ride for five or ten years at a time.

If you’re 55, the math shifts. You don’t have time to wait out a 40% market crash. At this stage, choosing what to invest Roth IRA in becomes a game of capital preservation. You might actually want those bonds now. Or maybe a "Value" tilted ETF like VTV that focuses on established companies with steady cash flows rather than the next AI startup.

The Overlooked International Factor

We’ve had a decade where US stocks absolutely crushed the rest of the world. Because of that, many investors have ditched international stocks entirely.

📖 Related: Modern Office Furniture Design: What Most People Get Wrong About Productivity

That’s recency bias.

Experts like Burton Malkiel, author of A Random Walk Down Wall Street, often argue for a global approach. Adding an international fund like VXUS gives you exposure to markets in Europe, Japan, and emerging economies. Sometimes the US market is overpriced. Sometimes it’s underperforming. Having a bit of everything ensures you aren't betting the house on one single country's economy, even if it's ours.

The "Moonshot" Bucket

Some people use their Roth for "asymmetric bets." This is risky.

Since you can only put a limited amount into a Roth each year, losing it all hurts because you can’t just "refill" the bucket. You lose that "tax-free space" forever.

However, if you put $1,000 into a high-growth individual stock and it 10x's, that $10,000 is entirely tax-free. If you did that in a regular account, you’d owe a chunk to the government when you sold. This is why some people put a tiny "fun money" slice of their Roth—maybe 5%—into individual stocks or crypto ETFs (like IBIT for Bitcoin). It’s a gamble. If it pays off, the tax savings are legendary. If it fails, you’ve wasted precious Roth space.

Real World Breakdown: The Three-Fund Portfolio

If you want the most mathematically sound way to handle this, look at the Three-Fund Portfolio. It’s a strategy championed by the Bogleheads community and supported by decades of data. It consists of:

- A Total US Stock Market Index Fund (e.g., VTSAX)

- A Total International Stock Market Index Fund (e.g., VTIAX)

- A Total Bond Market Index Fund (e.g., VBTLX)

You decide the percentages. A 30-year-old might do 70% US, 25% International, and 5% Bonds. A 50-year-old might go 50/20/30. It’s simple. It’s low-cost. It beats most professional hedge fund managers over the long run because the fees are so low.

👉 See also: US Stock Futures Now: Why the Market is Ignoring the Noise

Fees are the silent killer of retirement. If you’re paying a 1% management fee on a mutual fund, and the fund returns 7%, you just gave away nearly 15% of your gains. In a Roth IRA, you want "Low Cost" to be your mantra.

Common Mistakes to Avoid

Don't buy tax-exempt municipal bonds in a Roth. It sounds smart, but it's redundant. "Muni" bonds already have tax advantages, so they usually offer lower interest rates. Putting them in a Roth is like wearing two raincoats. You’re paying for a benefit you already have and getting a lower return because of it.

Another big one? Over-diversifying. You don't need twelve different ETFs that all hold the same stocks. If you own an S&P 500 fund and a "Growth" fund, you probably own Apple and Microsoft twice. It doesn't make you safer; it just makes your taxes more annoying to track (though even that isn't a huge deal in a Roth).

Actionable Steps to Take Right Now

Stop overthinking. Analysis paralysis is the enemy of wealth.

If your money is sitting in cash, move it today. If you want the simplest path, put 100% into a Total Stock Market ETF (like VTI) or a Target Date Fund that matches your retirement year.

Check your expense ratios. If anything you own has an expense ratio higher than 0.20%, look for a cheaper version. Most index funds should be below 0.05%.

Automate the process. Set up a recurring buy so you aren't trying to time the market. The market doesn't care about your feelings or the headlines on CNBC. It rewards those who stay invested.

Max out that contribution before the deadline. For the 2025 tax year, you have until the April 2026 filing deadline to contribute for the previous year. If you haven't maxed out last year's space, do that first. Once that window closes, it’s gone forever.

The best time to start was ten years ago. The second best time is today. Pick a diversified, low-cost index fund and let the clock do the heavy lifting.