Ever played the board game? You know that feeling when your friend owns Boardwalk and Park Place, has hotels on every green property, and you’re just sitting there praying to roll a lucky number so you don't go bankrupt? That’s basically the vibe of a real-world monopoly, but with much higher stakes. In the actual world of finance and trade, understanding what is monopoly in economics isn't just about winning a game; it’s about how prices are set, how innovation dies or thrives, and why your cable bill is so annoying.

A monopoly happens when one single company or entity is the only provider of a specific product or service. There is no competition. None. If you want the thing, you buy it from them, or you don't get it at all. It’s the extreme opposite of perfect competition, where dozens of shops sell the same thing and fight over pennies to get your business.

The Core Mechanics of Market Power

To really get what a monopoly is in economics, you have to look at the "barriers to entry." This is a fancy way of saying it's really, really hard for anyone else to start a business in that same field.

Think about it. If I wanted to start a company that competes with my local water utility, I’d have to dig up every street in the city to lay my own pipes. That costs billions. Nobody is giving me a loan for that. Because the setup cost is so high, the existing water company has a "natural monopoly." They aren't necessarily evil geniuses; it just doesn't make sense for a second set of pipes to exist.

Economists like Joseph Schumpeter argued that some monopolies actually drive progress because they have the "excess" profit to spend on R&D. But most people side with the classic view that without a competitor breathing down your neck, you get lazy. You raise prices. You stop caring if the customer service line holds for forty minutes.

The Different Flavors of Being the Only Game in Town

Not every monopoly looks the same.

Some are Legal Monopolies. The government gives a company a patent—like for a new life-saving drug—which says "nobody else can sell this for 20 years." We do this to encourage people to spend money on inventing things. If a pharmaceutical giant spends $2 billion developing a cure, they want to know they can make that money back without a generic knock-off appearing the next day.

Then you have Geographic Monopolies. If you live in a tiny town in the middle of the desert and there’s only one gas station for 100 miles, that station is a monopoly. They can charge $8 a gallon because your only other option is walking through sand.

Price Makers vs. Price Takers

In a normal market, companies are "price takers." They look at what everyone else is charging and try to match it. If a coffee shop charges $15 for a plain latte while the guy next door charges $4, the expensive shop closes in a week.

✨ Don't miss: AquaFence Tampa General: What Most People Get Wrong About the Viral Flood Wall

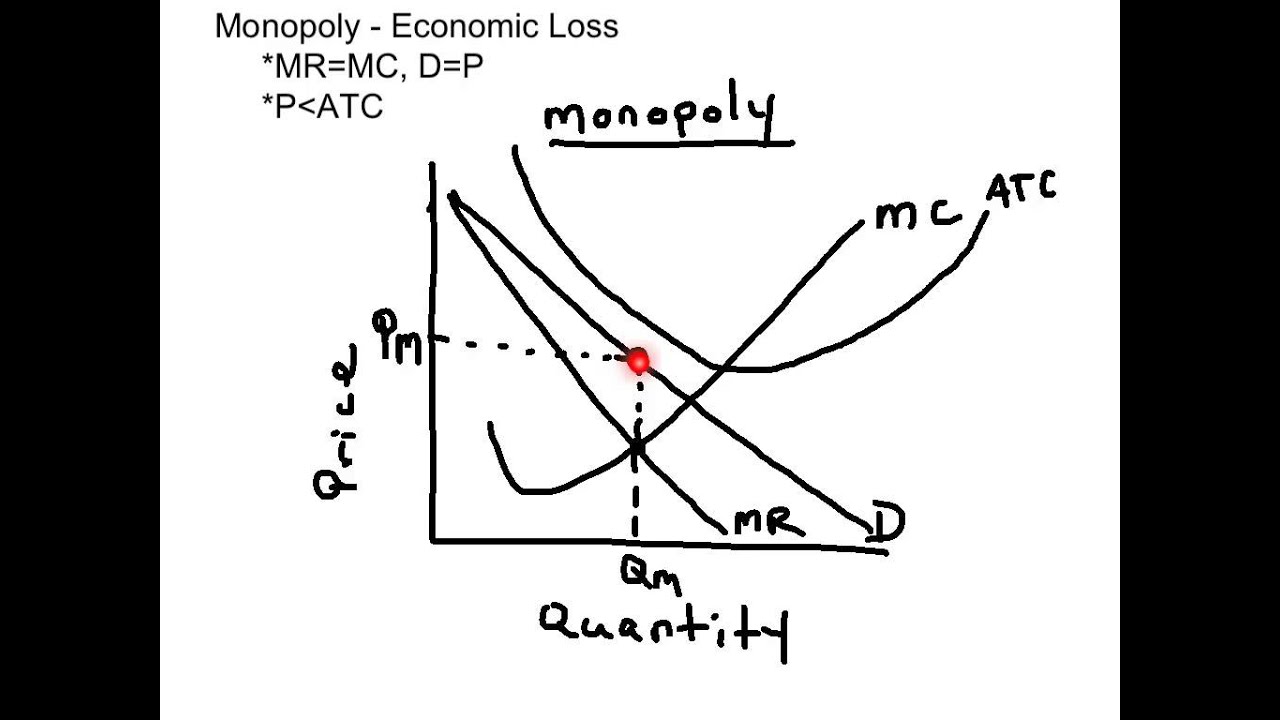

But a monopoly is a "price maker."

They don't look at the competition because there isn't any. Instead, they look at a demand curve. They ask: "If we raise the price by 20%, will 20% of people stop buying it?" If the answer is no—because people need the product—the monopoly raises the price. This is why insulin prices or utility rates are such heated political topics. When the product is a necessity, the monopoly has an incredible amount of leverage over your bank account.

Real Examples That Aren't Just Theory

Let's talk about Standard Oil. Back in the late 1800s, John D. Rockefeller controlled about 90% of the oil refineries in the U.S. He didn't just win by being better; he used his size to crush everyone else. He’d lower prices in one city to drive a local refinery out of business, then raise them back up once he was the only one left. This is "predatory pricing." It eventually led to the Sherman Antitrust Act of 1890, which is basically the rulebook the government uses to break up companies that get too big.

Then there’s Microsoft in the 90s. The government went after them because they were "bundling" Internet Explorer with Windows. Since almost everyone used Windows, it made it impossible for other browsers like Netscape to survive. It wasn't that Netscape was bad; it was that Microsoft owned the "territory" (the operating system) and used that power to control the "stores" (the browser).

💡 You might also like: 201 E Washington St: The Real Story Behind the City's Most Discussed Address

More recently, people argue about Google or Amazon. Is Google a monopoly because they are the best at search, or because they've made it so you can't really escape them? It’s a messy debate. Economists often use the Herfindahl-Hirschman Index (HHI) to measure market concentration, but even numbers don't tell the whole story.

Why Monopolies Can Be Total Innovation Killers

When a company doesn't have to fight for customers, they often stop trying to improve.

- Low Quality: If you hate your ISP but they're the only one in your zip code, they don't have to fix your slow internet.

- Reduced Choice: You get what they give you.

- Rent-Seeking: This is a term economists use for when a company spends more money on lobbying politicians to keep their monopoly than they do on making their product better.

Honestly, it’s a bit of a tug-of-war. Sometimes, a big company can produce things more cheaply because of "economies of scale." A giant factory can make a widget for $1, while a small shop makes it for $10. If the monopoly passes those savings to you, maybe it's okay? But they rarely do that unless they’re forced to.

How the Government Steps In

The "Antitrust" folks at the Department of Justice or the FTC are the referees. When they see a monopoly forming that hurts consumers, they have a few moves:

- Breaking it up: Like they did with Ma Bell (AT&T) in 1982, turning one giant into several "Baby Bells."

- Price Regulation: Telling a utility company "you aren't allowed to charge more than X."

- Blocking Mergers: Stopping two huge companies from joining forces to become a monopoly.

It's never simple. Determining what is monopoly in economics in a digital age is way harder than it was in the days of railroads and steel. How do you define a "market" for Facebook? Is it "social media"? Is it "advertising"? Is it "online attention"? Depending on how you define the borders, they either look like a scary monopoly or just one of many tech giants.

Actionable Insights for Navigating Monopolized Markets

Understanding the power dynamics of a monopoly helps you make better decisions as a consumer, an investor, or an entrepreneur. Here is how to apply this knowledge:

Identify the Moat

If you are investing in a company, look for "monopoly-like" qualities. Warren Buffett calls this a "moat." High barriers to entry—like proprietary tech or massive infrastructure—protect a company’s profits from being eaten by competitors. If a business has no moat, it will eventually face "price wars" that kill margins.

Watch for Substitution

The only thing that really kills a monopoly besides the government is a "substitute." People didn't break the horse-and-buggy monopoly by making better horses; they invented the car. If you feel trapped by a monopoly, look for the "lateral" solution. Don't like the cable monopoly? Starlink and 5G home internet are the "substitutes" currently breaking that grip.

Advocate for Transparency

In "Natural Monopolies" like power or water, your power is in the voting booth and at public utility commission meetings. These companies are legally required to serve the public interest in exchange for their monopoly status. If service is bad, the pressure must be political, not just commercial.

Evaluate "Free" Services Carefully

In the modern economy, many monopolies (like search engines or social networks) don't charge you money. They are "monopsonies" or data monopolies. Remember that if the product is free, your data and your attention are the currency. Knowing that they have a monopoly on your data should change how much of it you're willing to give away.