You’ve probably seen the headlines screaming about "criminal inquiries" and "political pressure." Honestly, it’s a lot to take in while you're just trying to figure out if your mortgage payment is going to go up or if you can finally afford that new truck.

The short answer? The Fed didn't change interest rates today—their big meeting isn't until January 27. But what did the federal reserve do today that actually matters? They spent today, January 15, 2026, digging in their heels. Between a high-stakes panel on stablecoins and a messy legal fight with the White House, the central bank is currently in the middle of a literal brawl over who actually controls your money.

The Stablecoin Showdown and Governor Barr

While most people are watching the drama between Chair Jerome Powell and President Trump, Governor Michael Barr was actually the one doing the heavy lifting this morning. At 9:15 a.m., he sat down at the Wharton School’s "Future of Finance Forum" in D.C. to talk about stablecoins.

It sounds boring. It's not.

Stablecoins are basically digital currencies pegged to the dollar, and the Fed is terrified they could cause a bank run if not regulated properly. Barr’s panel discussion today signaled that the Fed isn't backing down on its push for strict federal oversight. They want to make sure that if a "digital dollar" crashes, it doesn't take the rest of the banking system with it. For you, this means the Fed is still very much in the "policeman" role, trying to stay relevant as crypto keeps trying to eat their lunch.

👉 See also: To Whom It May Concern: Why This Old Phrase Still Works (And When It Doesn't)

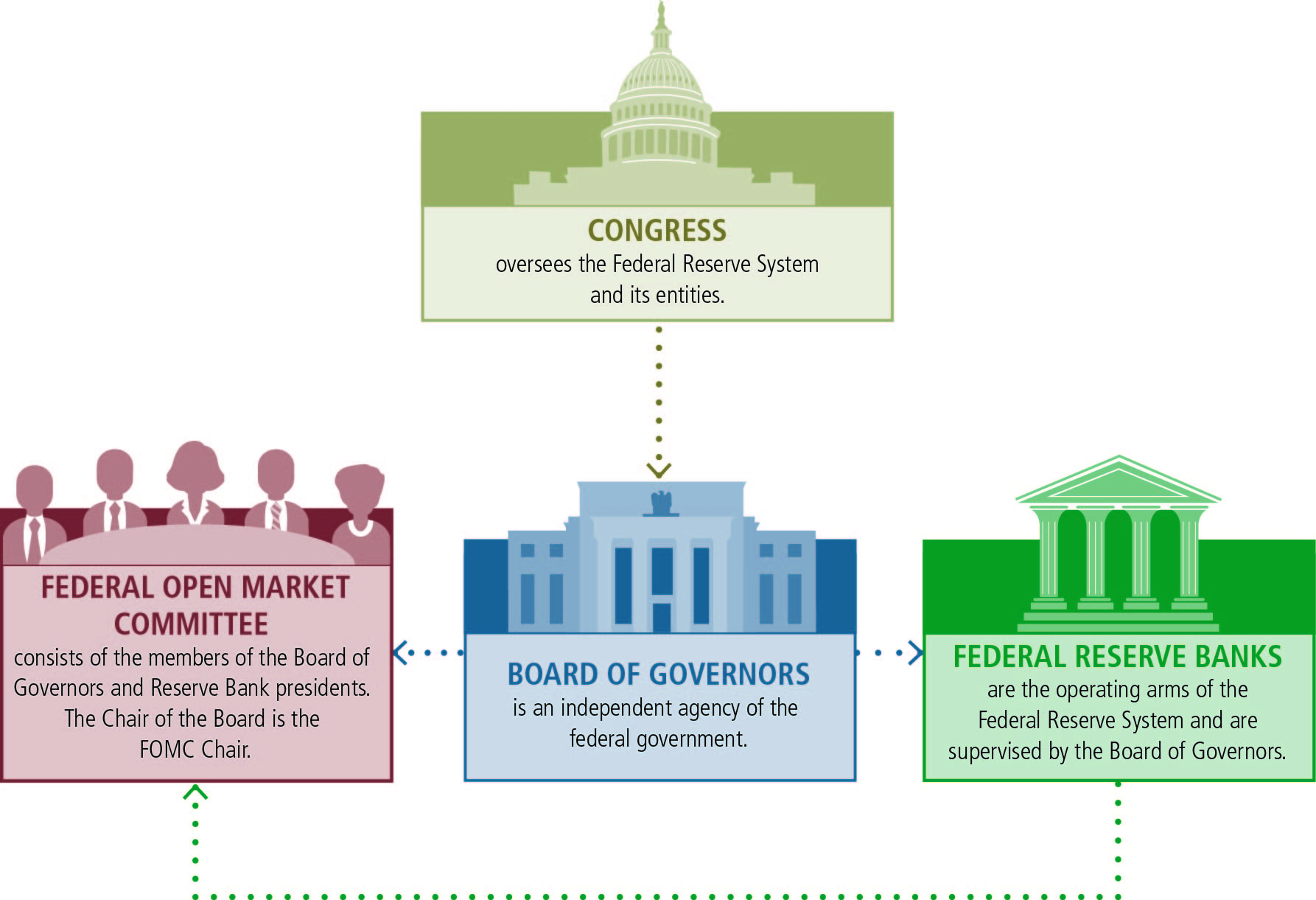

Why the Fed is Currently Under Investigation

You can't talk about what the Fed did today without mentioning the elephant in the room: the Department of Justice investigation into Jerome Powell.

This is wild.

The DOJ is looking into Powell’s previous testimony regarding the renovation of the Federal Reserve’s headquarters in Washington. Trump has been calling Powell a "jerk" and demanding he slash interest rates faster. Powell, being the mild-mannered guy he is, basically said "no" today by letting his allies do the talking.

- The DOJ Subpoena: This dropped recently, and today, Fed officials are basically in "defense mode."

- Political Independence: Austan Goolsbee, the Chicago Fed President, went on NPR to warn that if the Fed loses its independence, inflation is going to "come roaring back."

- The Standoff: Powell’s term as Chair ends in May. He’s dug in. He isn't quitting early, even though the White House is making things incredibly uncomfortable.

Let’s Talk About Your Wallet: Mortgage Rates Today

If you were looking for a rate cut today, you didn't get one. But that doesn't mean the market stood still.

✨ Don't miss: The Stock Market Since Trump: What Most People Get Wrong

The average 30-year fixed mortgage rate is sitting at 5.87% as of today, January 15. That’s actually a huge improvement from where we were a year ago when rates were north of 7%. The 15-year rate is even better, holding steady at 5.25%.

Here’s the catch: the Fed is looking at the "Beige Book" (their report on economic conditions) and seeing that while high-income people are still out there buying luxury goods and traveling, lower-income families are hurting. They're seeing "price sensitivity." Basically, people are tapped out. The Fed knows this, but they’re scared that if they cut rates too fast to help those families, the 2.7% inflation we’re seeing will jump back up to 4% or 5%.

What the Beige Book Revealed Yesterday

The Fed released its summary of economic activity, and the details are pretty telling. Eight out of twelve districts saw slight growth, but it’s a weird kind of growth.

- Tariffs are the new villain: Businesses are starting to pass tariff costs onto you.

- The Job Market: It’s "meh." Most hiring is just to replace people who quit, not to grow.

- AI is everywhere: Companies told the Fed they’re looking at AI to save money on labor, though it hasn't started replacing everyone just yet.

What Really Happened With the Interest Rate Pause?

Even though there was no formal FOMC meeting today, the Fed’s "implied" action was a pause. They are signaling that they aren't in a hurry to cut rates in January. Why? Because the latest inflation data showed food prices jumped 0.7% in December alone. That’s the biggest spike since 2022.

🔗 Read more: Target Town Hall Live: What Really Happens Behind the Scenes

The Fed's "quiet period" starts soon, so today was one of the last chances for officials like Michael Barr to set the tone. The vibe? Cautious. Very cautious.

They are stuck between a rock (the President wanting 0% rates) and a hard place (rising food costs due to tariffs). If they cut rates now, they look like they’re caving to political pressure. If they don’t cut, the stock market—which already took a hit recently—might continue to wobble.

Actionable Insights: What You Should Do Now

Since the Fed didn't move the needle today, the ball is in your court. Don't wait for a "magic" rate cut that might not come as fast as you hope.

- Lock in Refinancing if it makes sense: If you bought a home in 2023 or 2024 when rates were 7.5%, today’s 5.87% is a massive win. You don't need to wait for 4%. A 1.5% drop is enough to save hundreds a month.

- Watch the 10-Year Treasury: This is the real number that controls mortgage rates. If it spikes because of the Trump-Powell feud, mortgage rates will go up even if the Fed does nothing.

- Audit your "Tariff-Sensitive" spending: The Fed’s report today confirmed that retail and restaurants are starting to hike prices because of import costs. If you’ve been meaning to buy big-ticket electronics or imported goods, do it before the "pre-tariff" inventory runs out.

- Stay Liquid: With the DOJ investigating the Fed Chair, we are in uncharted territory. Keep your emergency fund in a High-Yield Savings Account. Even if the Fed eventually cuts rates, these accounts are still paying way better than they were five years ago.

The Fed's next big move happens on January 28. Until then, expect more noise, more subpoenas, and a lot of posturing from both sides of Pennsylvania Avenue.