You're scrolling through Zillow. You find it—the perfect three-bedroom with the wrap-around porch and the kitchen island of your dreams. You're already mentally placing your couch. Then, you see the application link. Your stomach drops. You start wondering about that one late credit card payment from two years ago. Honestly, the question of what credit score do you need to rent a house is less about a "magic number" and more about how much a total stranger is willing to trust you with their biggest financial asset.

There is no federal law dictates a minimum score. None.

If you’re looking for a quick answer, most property management firms want to see a 620 or higher. But that is a massive oversimplification. If you're trying to snag a luxury condo in downtown Austin or a brownstone in Brooklyn, that 620 might as well be a zero. Conversely, a private landlord in a rural town might not even run your credit if you show up with a solid paycheck and a firm handshake. It's complicated. It's nuanced. And it's often unfair.

The Magic Numbers (And Why They’re Kinda Arbitrary)

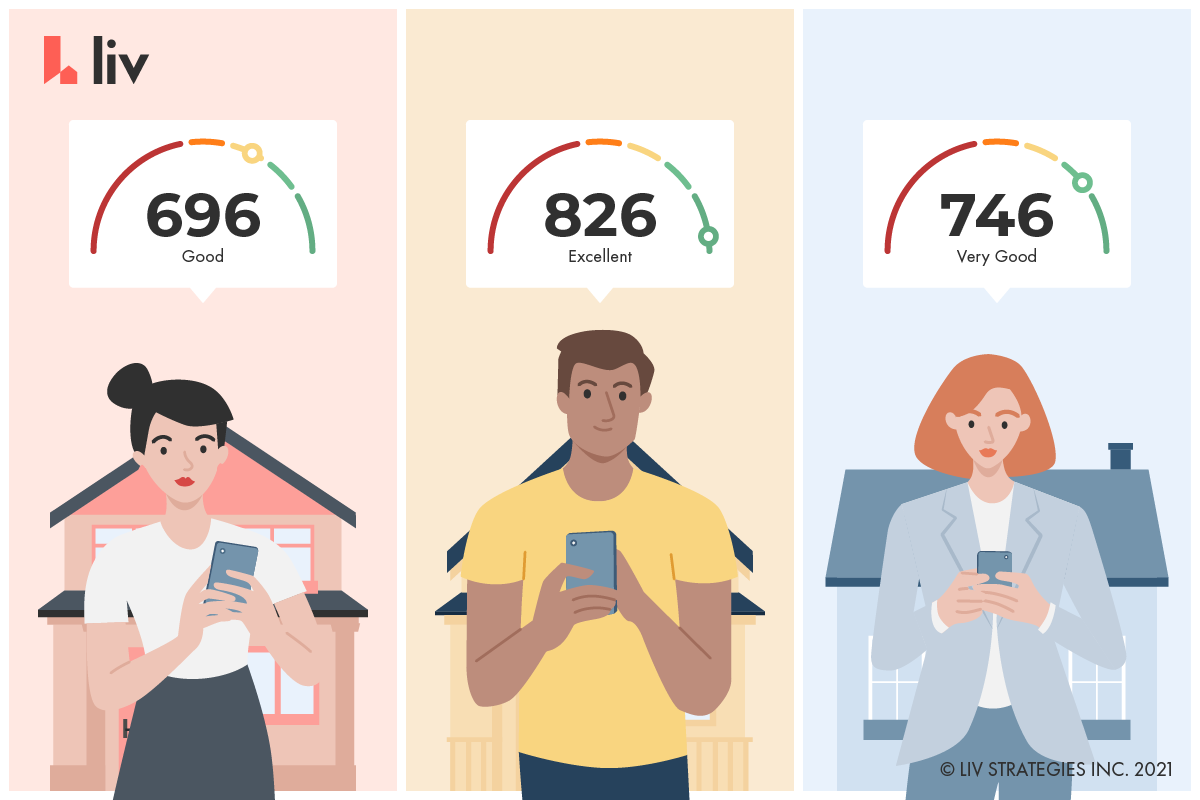

Credit scores range from 300 to 850. Most landlords use VantageScore or FICO. While they fluctuate, the "tiers" generally dictate your destiny in the rental market.

A score of 700+ makes you a rockstar. You’ll likely get approved within 24 hours. If you’re sitting between 650 and 690, you’re in the "safe but scrutinized" zone. Landlords might look closer at your debt-to-income ratio. Once you dip below 600, you’re entering the "red flag" territory where you'll probably need a co-signer or a massive security deposit.

But here is the kicker: Landlords care more about why your score is low than the number itself. A 580 caused by $50,000 in medical debt is viewed very differently than a 580 caused by three years of skipping out on utility bills. One suggests bad luck; the other suggests you’re a liability to the property’s overhead.

What Landlords Actually See When They Pull Your Report

They aren't just looking at the three digits. They are looking for "Rental Killers."

🔗 Read more: Finding the Right Word That Starts With AJ for Games and Everyday Writing

If you have an eviction on your record, your credit score is basically irrelevant. To a landlord, an eviction is a scarlet letter. It tells them you’ve already failed at the one thing they’re hiring you to do: pay rent and leave peacefully. According to data from the Eviction Lab at Princeton University, even a filed eviction that was later dismissed can haunt your screening report for seven years.

They also look for collections from utility companies. If you didn't pay your electric bill at your last place, why would this landlord believe you'll pay for the heat here?

Then there’s the debt-to-income ratio (DTI). You could have an 800 credit score, but if you make $5,000 a month and your car payment, student loans, and credit card minimums total $4,500, you are a high-risk tenant. Most professional landlords require your gross monthly income to be at least three times the monthly rent. If the rent is $2,000, you better be pulling in $6,000 before taxes.

The Difference Between Corporate and Private Landlords

This is where the strategy changes.

Large property management companies (the ones with "Apartment Homes" in the name) are algorithmic. They plug your data into a software like Yardi or RealPage. If the software says "Deny," the leasing agent literally cannot help you. They have no discretion. Their hands are tied by corporate policy and Fair Housing risk mitigation.

Individual landlords—the "mom and pop" owners—are human beings.

💡 You might also like: Is there actually a legal age to stay home alone? What parents need to know

They are often more flexible but also more terrified. They aren't backed by a multi-billion dollar REIT. If you don't pay rent, they might miss their own mortgage payment. If you're asking what credit score do you need to rent a house from an individual, the answer is often "whatever makes them feel safe." You can win them over with a "Rental Resume" or a letter of explanation. I’ve seen tenants with 550 scores get amazing houses because they provided three years of proof of on-time payments and a glowing recommendation from a previous landlord.

Strategies for the "Credit Challenged"

So, your score sucks. What now? You aren't doomed to live in your parents' basement forever.

Find a Guarantor

A co-signer or guarantor is someone with great credit (usually 700+) who signs the lease with you. They are legally responsible if you bail. It’s a huge ask, but it’s the fastest way to bypass a low score.

Offer More Cash Upfront

Money talks. If the landlord is hesitant, offer to pay the last month’s rent in advance or increase the security deposit. Note: Some states, like New York or California, have strict caps on how much a landlord can legally take for a security deposit, so check your local tenant laws first.

Show, Don't Just Tell

Print out your bank statements for the last six months. Show them the steady deposits. Show them that you have a "cushion." Transparency kills suspicion.

Look for "No Credit Check" Rentals

They exist, mostly on platforms like Facebook Marketplace or Craigslist. Be careful, though. These can sometimes be "slumlords" who don't care about your credit because they don't plan on maintaining the property either. Or worse, they’re scams. Never wire money before seeing the inside of a house.

📖 Related: The Long Haired Russian Cat Explained: Why the Siberian is Basically a Living Legend

Why Your Score Might Be Different Than You Think

You check Credit Karma. It says 680. The landlord pulls your report and says it’s a 642.

You feel cheated.

But here’s the reality: there are dozens of different credit scoring models. Most "free" apps use VantageScore 3.0. However, many landlords still use FICO Score 8 or even older versions specifically tuned for the housing industry. Furthermore, different bureaus (Equifax, Experian, TransUnion) might have different information. If a medical collection is only reporting to TransUnion and your landlord only pulls Experian, you might get lucky. But you can't count on that.

The Impact of 2026 Economic Trends on Renting

It's 2026. The rental market has shifted. We've seen a massive influx of "Build-to-Rent" communities. These are entire neighborhoods of houses owned by institutional investors. These entities are notoriously strict about credit scores. They use AI-driven risk assessment models that look at your "alternative data"—like whether you pay your Netflix subscription on time or how often you use "Buy Now, Pay Later" services like Affirm.

If you’ve been leaning heavily on "Buy Now, Pay Later" for groceries or clothes, be aware that these are starting to impact your internal risk score with these large agencies. They see frequent use of these services as a sign of cash-flow instability.

Actionable Steps to Take Right Now

Stop guessing and start prepping. If you want to rent in the next six months, do this:

- Pull your own "Big Three" reports. Go to AnnualCreditReport.com. It's free. Look for errors. A single incorrectly reported late payment can drag your score down 50 points. Dispute everything that isn't 100% accurate.

- Pay down your revolving balances. Your credit utilization—how much of your limit you're using—counts for 30% of your FICO score. If you can get your cards below 10% utilization, your score will jump quickly.

- Write a "Statement of Credit." If you have a specific blemish (a divorce, a medical emergency), write a one-paragraph explanation. Keep it professional. No sob stories, just facts and how you've fixed the situation.

- Get a "Verification of Rent" (VOR). Ask your current landlord to provide a ledger showing every payment you've made for the last year. This is more powerful than a credit score because it proves you can actually handle the specific responsibility of rent.

- Target older listings. If a house has been on the market for 45 days, the landlord is bleeding money. They are much more likely to overlook a 610 credit score on day 46 than they were on day one.

The bottom line? A credit score is a gatekeeper, but it's not a brick wall. Focus on the total package of your application. Professionalism, proof of income, and a clean rental history can often outweigh a mediocre number on a screen.

Next Steps for Your Search

Identify your actual FICO 8 score through your bank or a paid service, as this is what most landlords will see. Once you have that number, filter your search by property type; aim for privately owned condos or townhomes where you can speak directly to the owner, rather than massive apartment complexes managed by third-party software. Finally, prepare a folder with your two most recent paystubs, a copy of your ID, and your VOR so you can apply the second you find a place you love. Speed is often just as important as your score in a competitive market.