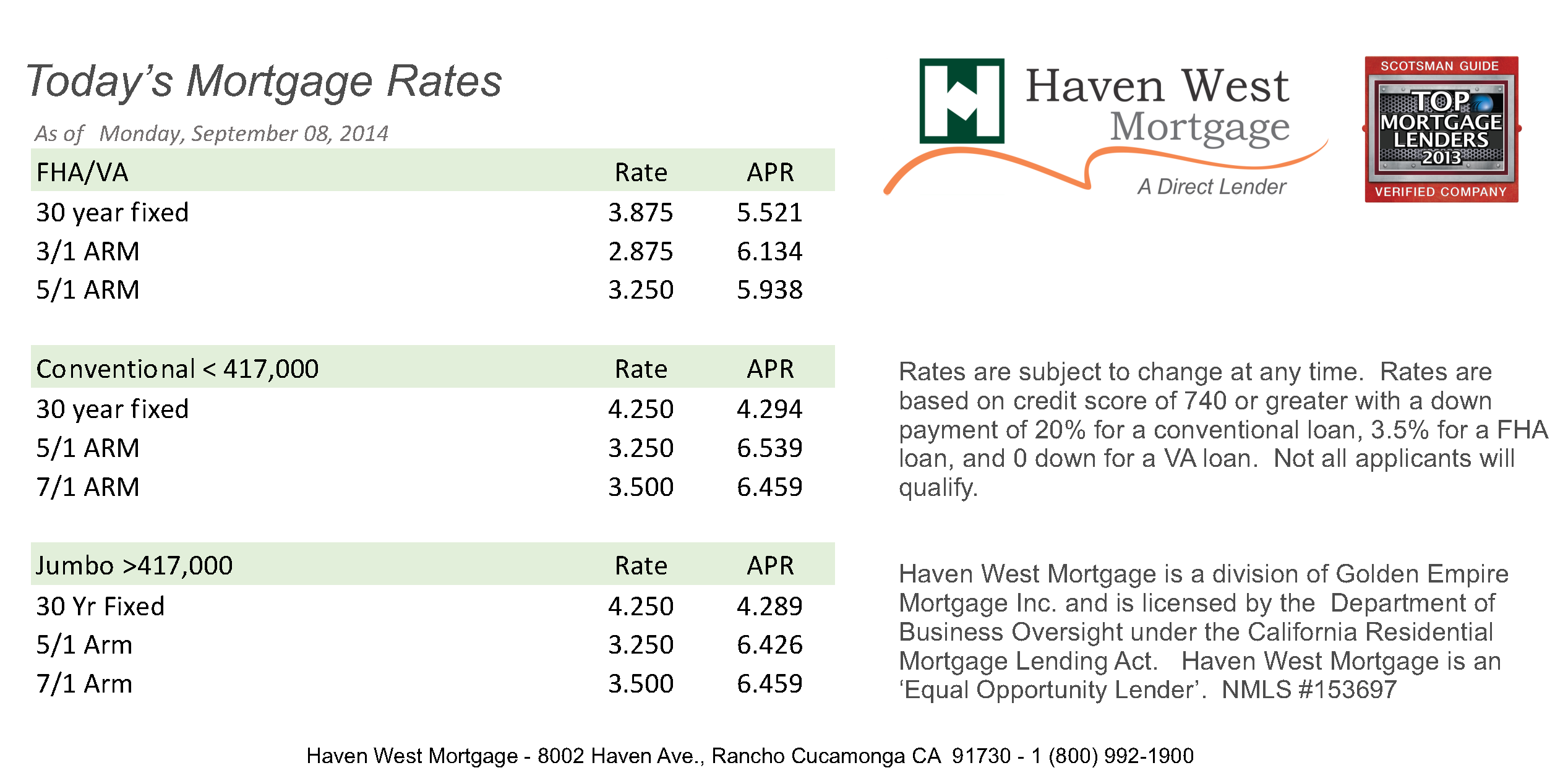

Honestly, if you took a nap for most of 2024 and 2025, you might wake up today and think the housing market finally decided to be chill. It’s been a wild ride. But as of Wednesday, January 14, 2026, the numbers on those mortgage apps are actually starting to look halfway decent for a change.

We’ve spent a long time staring at 7% and 8% rates like they were some kind of permanent weather pattern. Now, the clouds are breaking. Today’s average 30-year fixed mortgage rate is sitting right at 5.99%, according to the latest data from Zillow. Bankrate is a bit more conservative, tagging the national average APR at 6.20%, but the trend is clear.

We are officially flirting with the "fives" again.

What are the mortgage interest rates today for different loan types?

If you're hunting for a house right now, "average" is a loose term. Your actual rate depends on which door you walk through. A 15-year term is always going to be cheaper than a 30-year one, but the gap is feeling pretty significant this week.

Here is a breakdown of what the street is saying for mid-January 2026:

- 30-Year Fixed-Rate: 5.99% to 6.14% (The standard choice, finally dipping under 6% at some lenders).

- 15-Year Fixed-Rate: 5.25% to 5.53% (Great for saving on interest if you can swing the higher monthly bill).

- 30-Year FHA Loans: 6.24% (Often carries a slightly higher APR because of those mortgage insurance premiums).

- 30-Year VA Loans: 6.49% (Technically higher in some surveys this week, but with zero down, it’s still a powerhouse).

- Jumbo Loans: 6.38% (For the big spenders buying above the conforming loan limits).

Refinancing is also seeing a bit of a localized boom. If you were one of the unlucky folks who closed on a house in early 2025 when rates were screaming, today’s 30-year refinance rate is averaging about 6.52%. It’s not a "drop everything and call your broker" moment for everyone, but for some, it’s a couple of hundred bucks back in the pocket every month.

📖 Related: PDI Stock Price Today: What Most People Get Wrong About This 14% Yield

Why the sudden shift in early 2026?

You can thank a mix of government intervention and a very cautious Federal Reserve.

A big headline from just a few days ago really moved the needle: the government-sponsored enterprises (GSEs) were instructed to purchase $200 billion in mortgage-backed securities (MBS). If that sounds like nerd-speak, basically it means the government is putting its thumb on the scale to force mortgage rates lower, even if the Fed is taking its sweet time.

Speaking of the Fed, they haven't been "fast." They’ve been deliberate. After a string of 25-basis-point cuts throughout late 2025, the federal funds rate is currently sitting in a range of 3.50% to 3.75%. Jerome Powell hinted in his last presser that the economy is "resilient," but the housing market has been the "weak link."

Basically, they know you're struggling to afford a 3-bedroom ranch in the suburbs.

The Bond Market's Influence

Mortgage rates don't actually follow the Fed; they follow the 10-year Treasury yield. Right now, that yield is hovering around 4.17%. When investors feel better about inflation staying in its lane, they buy bonds. When they buy bonds, yields go down. When yields go down, your mortgage quote looks a whole lot prettier.

👉 See also: Getting a Mortgage on a 300k Home Without Overpaying

What most people get wrong about credit scores and rates

You see a 5.99% rate on a billboard and think, "Sweet, I'm getting that."

Slow down.

Those "headline" rates are usually reserved for the "perfect" borrower—someone with a 780 credit score and a 20% down payment. If your credit is more in the "okay" range (think 640 to 680), you aren’t seeing 5.99%. Honestly, you’re likely looking at something closer to 7.02% or 7.15% for a conventional 30-year loan.

The Credit Score Gap in 2026:

The difference between a 660 and a 760 score can literally cost you $200 or more on your monthly payment for the exact same house. In today’s market, it’s less about "getting a loan" and more about "not getting penalized for your score."

Is it actually a good time to buy?

It's a "maybe."

✨ Don't miss: Class A Berkshire Hathaway Stock Price: Why $740,000 Is Only Half the Story

Inventory is finally recovering. Active listings are up nearly 9% compared to this time last year. That means you might actually get to see a house twice before making an offer, rather than bidding $50k over asking while standing in the driveway.

But there’s a catch.

Because rates are dropping, more buyers are coming out of the woodwork. Purchase applications are up 20% from a year ago. It's the classic "Goldilocks" problem: you want rates low enough to afford the payment, but not so low that 50 other people are bidding against you on a Tuesday morning.

The "Lock-In" Effect is Cracking

For the last two years, nobody wanted to sell because they were sitting on a 3% rate from 2021. Why trade 3% for 7%? Now that market rates are hitting the 5s, that math is changing. We’re seeing more "move-up" buyers finally listing their starter homes.

Actionable steps for your mortgage search

If you're serious about figuring out what are the mortgage interest rates today for your specific situation, don't just trust a Google snippet.

- Check your median FICO score. Not the one your credit card app gives you (which is often a VantageScore), but the actual FICO versions lenders use.

- Get three quotes. This is the one thing everyone says to do, but nobody does. A 0.25% difference in your rate over 30 years is the price of a mid-sized SUV.

- Watch the January 28 Fed meeting. While they might not cut rates again immediately, their "tone" will dictate where rates go in February.

- Lock your rate if you're under contract. Volatility is still a thing. If you see a 5.8% or 5.9% quote and you're happy with it, grab it. Waiting for 4% might mean waiting for a recession that hasn't arrived yet.

The housing market isn't exactly "cheap" in 2026, but it is finally becoming navigable. With rates dipping below that 6% psychological barrier, the leverage is slowly shifting back toward the people actually living in the houses, rather than just the people financing them.