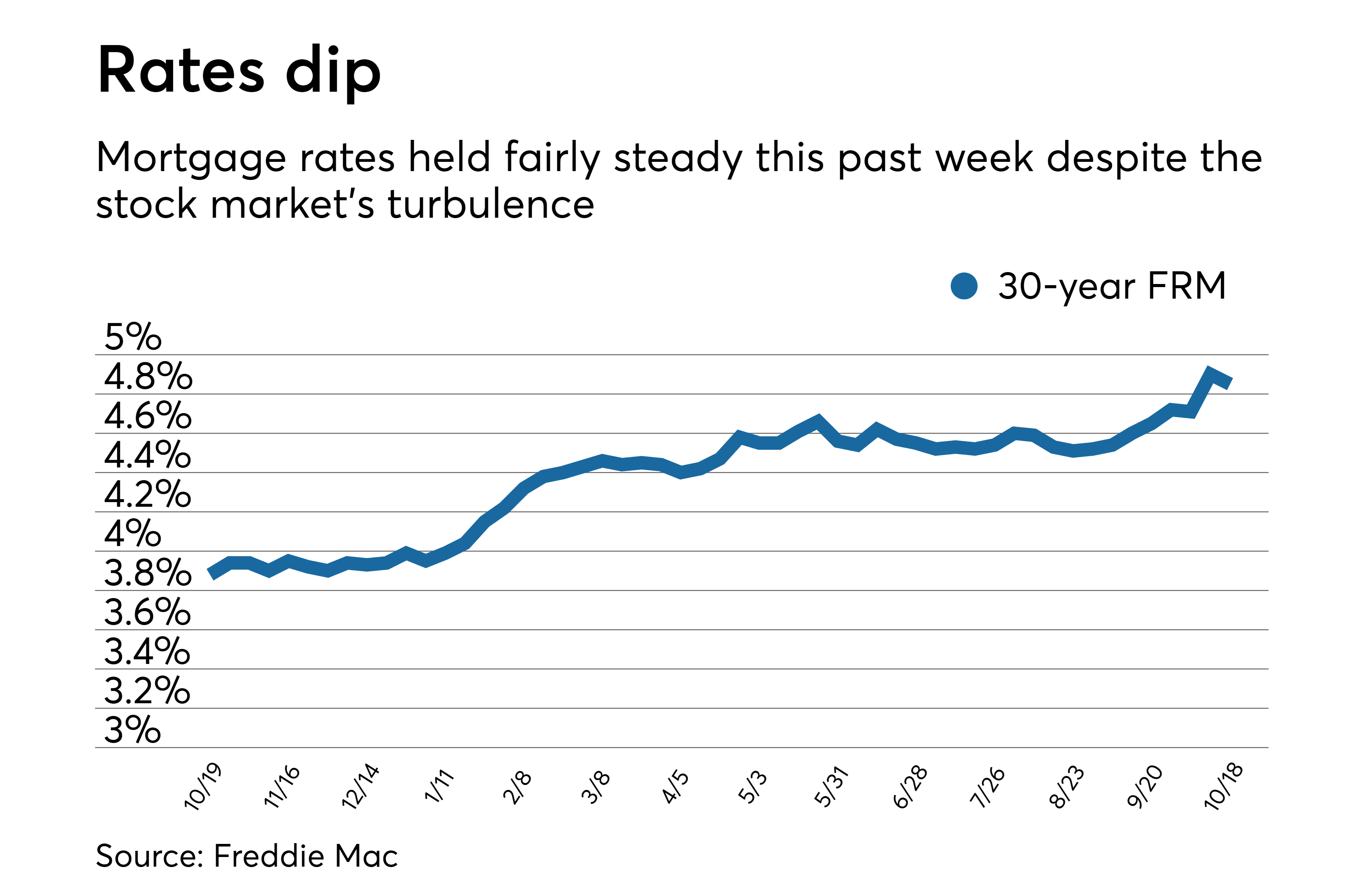

You’ve probably heard the rumors. Or maybe you’ve been refreshing your browser every morning, hoping for a miracle. Well, it’s officially Sunday, January 18, 2026, and the miracle is sort of—finally—here.

For the first time in what feels like an eternity, we are seeing the 30-year fixed mortgage rate dip its toes into the "fives."

Honestly, it’s about time.

But before you go pop a bottle of champagne or call your Realtor in a frenzy, let’s look at the actual numbers. The national average for a 30-year fixed mortgage is sitting right around 6.11% today. However, if you look at specific lenders like Zillow Home Loans, you’ll find some quotes hitting 5.99%.

That tiny difference is a huge psychological win.

Seeing a "5" at the front of a mortgage quote changes the entire vibe of the housing market. It’s like the "open" sign finally flipped over after a long, dark winter. But don't get it twisted—the market is still weird. Refinance rates are actually behaving a bit differently, often sticking closer to 6.56% or even 6.62% depending on who you ask.

What Are Mortgage Rates Right Now and Why Are They Moving?

It isn't just one thing. It's a messy cocktail of Federal Reserve vibes, government interventions, and the general "lock-in" effect that’s been holding the country hostage for years.

The big story right now is the directive given to Fannie Mae and Freddie Mac. They were told to buy roughly $200 billion in mortgage bonds. When the government (or government-adjacent entities) starts buying up those bonds, it creates demand. Higher demand for bonds means lower yields, and lower yields usually mean lower interest rates for you.

👉 See also: Why Amazon Stock is Down Today: What Most People Get Wrong

It's a bit of a brute-force way to lower borrowing costs, but hey, it’s working.

The Reality Check: 30-Year vs. 15-Year Fixed

If you’re looking to buy, the 30-year is still king. It's the standard. But the 15-year fixed is looking pretty juicy right now, averaging around 5.4% to 5.56%.

- 30-Year Fixed: ~6.11% (with some "5.99%" sightings)

- 15-Year Fixed: ~5.47%

- 30-Year FHA: ~5.78% (great for smaller down payments)

- 30-Year VA: ~6.26% (oddly higher than conventional in some spots today)

One weird thing happening? The 5-year ARM (Adjustable Rate Mortgage). Usually, these are the "cheap" option, but right now, some 5-year ARMs are quoted at 7.19%.

That’s what we call an inverted situation. It makes zero sense to take an ARM when you can get a fixed rate for 1% less. It's basically the market telling you, "We have no idea what's happening in five years, so we're going to charge you extra for the risk."

What the Experts Get Wrong About 2026

Most people expected 2026 to be the year of the "great crash" in rates. It hasn't quite happened that way. Fannie Mae predicts we’ll end the year at 5.9%, while the Mortgage Bankers Association is a bit more pessimistic, eyeing 6.4%.

There is a massive divide in the "expert" community right now.

Some, like Goldman Sachs, think the Fed will pause its rate-cutting cycle this month before starting again in March. Others think the Fed is terrified of inflation making a comeback. Remember, the Consumer Price Index (CPI) just clocked in at 2.7%. That’s not quite the 2% target the Fed obsesses over.

✨ Don't miss: Stock Market Today Hours: Why Timing Your Trade Is Harder Than You Think

Then you have the "lock-in" effect. Roughly 69% of American homeowners have a mortgage rate at or below 5%.

Why would they sell? Even with rates at 5.99%, moving means their monthly payment could still jump by hundreds of dollars. This keeps inventory low, which keeps home prices high. It’s a frustrating cycle where lower rates actually make people want to buy, but they don't necessarily make people want to sell.

The Refinance Window is Cracking Open

If you bought your house in 2023 or 2024 when rates were pushing 7.5% or 8%, you are probably itching to refinance.

Refinance demand is already up over 100% compared to last year. People are tired of paying "the trauma tax" on those high-rate loans. If your current rate is 7.2% and you can snag a 6.1%, that’s a massive win.

On a $400,000 loan, that 1% drop saves you roughly **$250 to $300 a month**. That’s a car payment. Or a lot of groceries.

However, keep an eye on the closing costs. Refinancing isn't free. If it costs you $6,000 in fees to save $250 a month, it’ll take you two years just to break even. If you plan on moving in 18 months, don't do it.

Your Move: Actionable Steps for This Week

Stop waiting for 3%. It's not coming back. Unless there’s another global catastrophe (which none of us want), those 3% pandemic rates are historical anomalies.

🔗 Read more: Kimberly Clark Stock Dividend: What Most People Get Wrong

1. Get a "Mortal" Credit Score

Lenders are being picky. To get that 5.99% headline rate, you generally need a credit score of 740 or higher. If you're at 680, you’re looking at a rate closer to 6.6%. Clean up your reports now.

2. Shop Three Lenders (Minimum)

I can't stress this enough. One bank might give you 6.2% with $2,000 in fees, while a local credit union might give you 6.1% with $5,000 in fees. You have to look at the APR, not just the interest rate. The APR includes the fees, giving you the "true" cost.

3. Watch the 10-Year Treasury Yield

Mortgage rates don't follow the Fed funds rate perfectly. They follow the 10-year Treasury yield. If you see news that the 10-year yield is dropping toward 3.75%, mortgage rates will follow. If it spikes to 4.5%, mortgage rates will head back toward 7%.

4. Consider the "Buy-Down"

If you find a house you love but the rate still stings, ask the seller for a credit to "buy down" your rate. A 2-1 buy-down could give you a rate in the 4% range for the first year, giving you time for the market to (hopefully) settle even further.

The "Wait and See" game is dangerous because as rates drop, more buyers jump in. More buyers mean more competition, which leads to bidding wars. You might save $100 on your mortgage payment only to pay $30,000 more for the house because you were fighting ten other people for it.

Bottom line: We are in a "good enough" territory. It's not the 2021 gold rush, but it's a far cry from the 2023 nightmare. Grab a quote, run the numbers, and see if they make sense for your specific life, not just the national average.