If you’ve been glued to your phone waiting for a sign from the housing market, today is a bit of a milestone. As of Friday, January 16, 2026, we are looking at some of the most interesting numbers we’ve seen in years. Basically, the drama isn't over, but it’s definitely changed its tune.

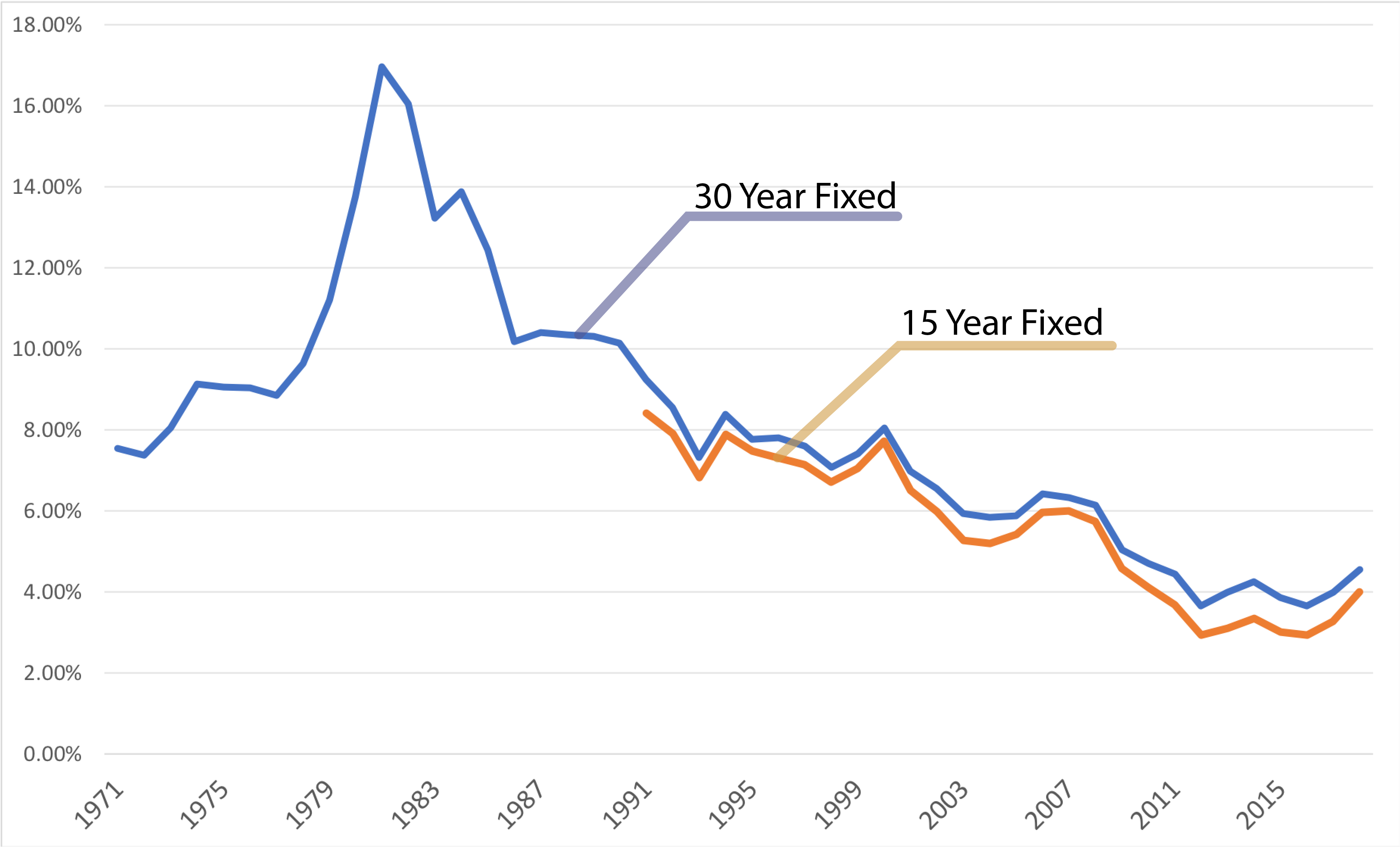

Right now, the national average for a 30-year fixed mortgage sits at approximately 6.11%.

Some lenders are dipping lower—I’ve seen quotes as low as 5.87% for buyers with pristine credit—but for the average person walking in off the street, 6.1% is the neighborhood you’re living in. Compared to the 7% or 8% nightmares of 2024 and early 2025, this feels like a win. Is it a 3% rate? No. Honestly, we might never see those again in our lifetime. But it is a three-year low, and that matters.

What are mortgage rates now and why do they keep shifting?

The "now" is a moving target. Just yesterday, Freddie Mac reported that the 30-year average dropped to 6.06%, down from 6.16% just a week ago. That’s a decent slide. If you’re looking at a 15-year fixed mortgage, you’re looking at about 5.38%.

Why the sudden dip?

It’s a mix of politics and math. Last week, a surprise announcement regarding Fannie Mae and Freddie Mac buying up $200 billion in mortgage-backed securities sent a shockwave through the bond market. When the government (or those government-adjacent giants) starts buying, yields tend to drop, and mortgage rates follow them down like a shadow.

👉 See also: Sands Casino Long Island: What Actually Happens Next at the Old Coliseum Site

But don't get too comfortable.

The Federal Reserve is currently in a "wait and see" mode. While they hacked away at rates in late 2025, the vibe for 2026 is much more conservative. J.P. Morgan’s chief economist, Michael Feroli, recently suggested that the Fed might not cut rates at all this year. If inflation stays sticky—and it’s currently hovering above that 3% mark the Fed hates—we might be stuck in this 6% range for a long while.

The Refinance Reality Check

If you bought your house when rates were peaking at 7.5% or 8%, you’re probably itching to refi.

- 30-year Refinance: Currently averaging 6.58%.

- 15-year Refinance: Averaging 5.91%.

Wait, why are refi rates higher? Lenders view them as slightly riskier, and they don't have the same "new purchase" incentives. You’ve gotta run the math on the "break-even" point. If it costs you $5,000 in closing costs to save $150 a month, you need to stay in that house for three years just to get your money back.

The Battle Between the Fed and the Market

There is a massive tug-of-war happening right now. On one side, you have the Trump administration pushing for lower rates to stimulate the economy. On the other, you have the Fed members, who are notoriously protective of their independence.

✨ Don't miss: Is The Housing Market About To Crash? What Most People Get Wrong

Goldman Sachs and Barclays are betting on a rate cut maybe by June, but that’s a "maybe" with a capital M.

The unemployment rate just fell to 4.4%. Usually, a strong job market is great, but for mortgage rates, it’s a double-edged sword. If everyone has a job and is spending money, inflation stays high. If inflation stays high, the Fed keeps the "higher for longer" stance.

It’s a bit of a catch-22 for the average homebuyer.

Regional Differences and "Hidden" Rates

Not all 6% rates are created equal. If you’re in California, for instance, programs like CalHFA are offering conventional rates around 5.875% for certain buyers. Meanwhile, if you’re looking for a Jumbo loan—loans that exceed the standard limits—you’re likely looking at 6.4% or higher.

Lenders are also getting creative with "buy-downs." You might see an advertised rate of 4.99%, but look at the fine print. Usually, that’s a "2-1 buy-down" where the rate is low for the first year, slightly higher the second, and then hits the market rate in year three. It’s a great tool if you expect your income to rise, but it’s a gamble if you’re on a fixed budget.

🔗 Read more: Neiman Marcus in Manhattan New York: What Really Happened to the Hudson Yards Giant

What Most People Get Wrong

People often think the Fed sets mortgage rates. They don't. They set the Federal Funds Rate, which is what banks charge each other for overnight loans. Mortgage rates actually track the 10-year Treasury yield.

The "spread"—the gap between the 10-year yield and mortgage rates—is usually about 1.7 percentage points. Lately, it’s been much wider, closer to 2.5 or 3 points because of market volatility. If that spread "normalizes," mortgage rates could drop to the mid-5s even without the Fed doing a single thing.

Actionable Steps for Today's Market

If you are looking at what are mortgage rates now and trying to decide whether to pull the trigger, here is the ground-level strategy:

- Check your DTI (Debt-to-Income): Lenders are being incredibly picky right now. Even a small car loan can bump your interest rate up by 0.25% if it pushes your DTI over the 43% threshold.

- Lock, don't gamble: If you find a rate under 6.1% and you’ve found a house you love, lock it. The market is too jumpy to try and time the "bottom."

- Look at the 15-year option: If you can swing the higher monthly payment, a 5.38% rate will save you literally hundreds of thousands of dollars in interest over the life of the loan.

- Ignore the "Wait for 4%" crowd: Most experts, from Fannie Mae to the Mortgage Bankers Association, see rates hovering between 5.9% and 6.4% for the foreseeable future. Waiting for a massive drop might mean you end up paying a higher purchase price as competition heats up in the spring.

The bottom line is that the "floor" for mortgage rates seems to be forming right around that 6% mark. While we might see occasional dips into the high 5s, the era of "free money" is firmly in the rearview mirror. Focus on the monthly payment you can afford today, rather than the "perfect" rate that might not arrive until 2027.

To get started, pull your credit report today and dispute any errors immediately, as a 20-point swing in your score can be the difference between a 6.1% and a 6.5% rate. Once your credit is polished, get pre-approved by at least three different types of lenders—a big bank, a credit union, and an online mortgage broker—to ensure you’re seeing the full spectrum of available rates.