Honestly, walking into a bank branch feels kinda old school these days. But when you look at wa federal cd rates—or WaFd Bank as they're officially called now—you realize there’s a reason people still do it. Most of us just default to the massive national banks because they have the slickest apps. The thing is, those big banks often pay pennies on your savings. Washington Federal (WaFd) has been carving out a weirdly specific niche by offering "Special" CDs that actually keep up with inflation, even in 2026.

I’ve spent a lot of time looking at the numbers for this year. The rate environment is shifting. With the Fed hinting at a couple of cuts later in 2026, locking in a rate right now isn't just a "maybe" move; it's sorta a "must-do" if you want to protect your cash.

The Reality of Wa Federal CD Rates Right Now

If you go to a standard big-name bank, you might see 0.01% on a savings account. It’s a joke. WaFd doesn't play that game with their promotional products. They have these "Special" terms that don't follow the usual 12-month or 24-month logic.

As of early 2026, their 7-month Special CD is the star of the show, sitting at around 3.50% APY.

Now, is that the highest in the entire country? No. You can find online-only banks like E*TRADE or Ally hitting 4.00% or higher. But for a brick-and-mortar bank with actual human beings you can talk to in Washington, Arizona, or Idaho, 3.50% is surprisingly aggressive. They also have a 13-month Special at 3.30% APY.

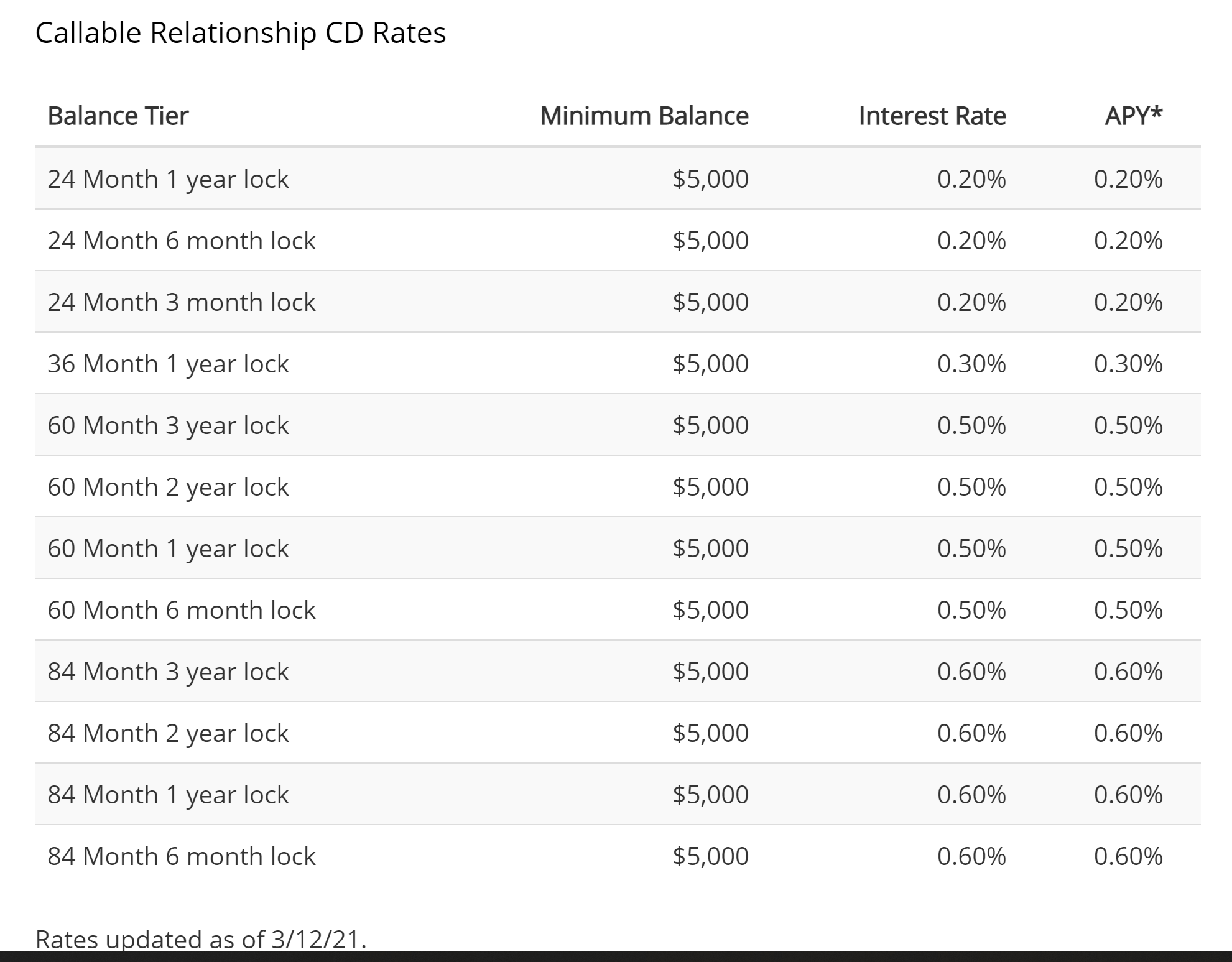

What’s interesting is the "drop-off." If you ignore the specials and just look at their standard fixed-rate CDs—like a 36-month or 60-month—the rates plummet to almost nothing, sometimes as low as 0.20% to 0.35%. It’s a classic bank move. They want you in the door with the short-term high-yield stuff, hoping you'll stick around for the long haul.

💡 You might also like: New Zealand currency to AUD: Why the exchange rate is shifting in 2026

Breaking Down the Current Specials

You’ve gotta be careful with the terms. Here is what the landscape looks like for the "worth it" accounts:

- 7-Month Special: 3.50% APY ($1,000 minimum). This is the "sweet spot" for most people.

- 13-Month Special: 3.30% APY ($1,000 minimum). Good if you want to bridge into next year.

- 19-Month Special: 3.15% APY. Still decent, but the yield curve is definitely inverted here.

- 30-Month Special: 2.95% APY. This is where it starts to feel a bit thin.

Why the "Special" Tag Matters

You might wonder why they don't just give these rates to everyone on every term. It's about liquidity and bank strategy. WaFd is trying to balance their books for the next year. By offering a 7-month special, they’re betting that they can use your capital now and that rates might be lower when they have to pay you back.

If you’re the type who likes to "ladder" your money, these weirdly timed specials are actually great. You can put a chunk in a 7-month and another in a 13-month. This way, you have cash coming "due" at different times. If rates go up (unlikely this year), you can reinvest. If they go down, you at least locked in a portion for over a year.

The Fine Print (The Stuff That Bites)

Everything isn't sunshine and high yields. There’s a reason people get annoyed with traditional banks.

First off, the early withdrawal penalty. If you suddenly need that money for a car repair or a medical bill before the 7 months are up, WaFd is going to take a bite out of your interest. Usually, it's several months' worth of earnings. If you’re not 100% sure you can leave that money alone, look at their High Yield Money Market instead. It pays less (around 2.50% for higher balances), but you can actually touch it.

📖 Related: How Much Do Chick fil A Operators Make: What Most People Get Wrong

Also, these "Specials" usually require "New Money." This is a phrase banks use to mean money that isn't already sitting in a WaFd account. They want to attract new customers or additional deposits. If you just move money from your WaFd checking to a CD, you might not get the promo rate. You’ve gotta bring it in from the outside.

How WaFd Compares to Others in 2026

I mentioned earlier that online banks are beating these rates. Let’s be real. If you are purely chasing the highest possible number, you're going to Marcus by Goldman Sachs or a credit union.

But WaFd is a different beast. They were recently named one of the "Best-in-State" banks by Forbes. That's not just about the wa federal cd rates; it’s about the fact that they don't have the "hidden" fee culture that some of the mega-banks do. They have a massive footprint in the Pacific Northwest and the Southwest. For a lot of folks, having a local branch matters more than an extra 0.50% in interest.

The 2026 Economic Factor

CEO Brent Beardall has been pretty vocal about the bank's stability. While some regional banks got shaky a few years back, WaFd has kept a pretty conservative balance sheet. Their efficiency ratio is improving, and they're actually growing their wealth management arm. This matters because a CD is only as good as the bank behind it. Since they are FDIC insured, your first $250,000 is safe anyway, but it's nice to know the company isn't a mess.

Is It Time to Lock In?

The big question: Should you do it now?

👉 See also: ROST Stock Price History: What Most People Get Wrong

Most analysts, and even the leadership at WaFd, expect the Federal Reserve to cut rates at least once or twice this year. When the Fed cuts, CD rates follow almost immediately. If you wait until June to open a CD, that 3.50% might be 2.75%.

If you have $5,000 or $10,000 sitting in a standard savings account earning 0.10%, you are literally losing money to inflation every single day. Even if you don't go with WaFd, move it somewhere.

Actionable Steps for Your Cash

Don't just read this and forget about it. Your money is losing value while it sits idle.

- Check your current "New Money" status. If you have cash in a different bank, you’re a prime candidate for the WaFd specials.

- Aim for the 7-month window. It’s the highest yield they offer right now. It gives you a great return without locking your life away for years.

- Minimums. Make sure you have at least $1,000. That’s the "ticket to entry" for almost all their decent CD products.

- Automate the exit. When the CD matures, WaFd (and most banks) will automatically renew you into a standard CD. Remember how I said standard rates are terrible? Like 0.20%? If you don't move your money within the 10-day grace period after it matures, you’ll be stuck in a low-interest trap for another 7 months. Mark your calendar the day you open the account.

Moving your money into a CD isn't a get-rich-quick scheme. It's a "don't-get-poor-slowly" scheme. With the way things are looking for the rest of 2026, grabbing a guaranteed 3.50% is a solid, boring, and very smart move for your emergency fund or short-term savings.