Money is weird. Especially when we're talking about thirty-four trillion dollars. Honestly, if you look at a US national debt historical graph, the first thing you’ll notice is that it looks like a literal mountain climber’s nightmare. It starts as a flat line for about a century, then it starts to crawl, and suddenly, around the year 2000, it just teleports into the stratosphere.

But here is the thing.

Most people look at that line and think the country is going bankrupt tomorrow. They see the spikes and panic. While the numbers are undeniably massive—bordering on the surreal—the graph doesn't always tell the story people think it does. You've got to look at what was happening behind the scenes. Wars, pandemics, and weird tax shifts change the context of that "scary" line. It's not just a receipt for a shopping spree; it's a map of every major crisis the United States has survived since the late 1700s.

The Early Days: When Being Debt-Free Was Actually a Goal

Believe it or not, there was a time when the US actually paid off its debt. Just once. It was 1835. Andrew Jackson hated the idea of a national debt so much that he sold off vast amounts of government land and vetoed basically every spending bill he could find. For one brief moment in history, that US national debt historical graph actually touched zero.

It didn't last.

📖 Related: The Death of the Mall: Why Most People Are Reading the Post-Mortem All Wrong

The Panic of 1837 hit, the economy tanked, and the government had to start borrowing again. Before that, the debt was mostly a leftover from the Revolutionary War. Alexander Hamilton, the first Treasury Secretary, actually thought a "public debt" was a good thing—a "national blessing" if it wasn't too big. He figured if we owed people money, they’d have a vested interest in the country succeeding. It’s a bit like staying friends with someone just because they owe you twenty bucks.

The Civil War was the first real "vertical" move on the chart. In 1860, the debt was roughly $65 million. By 1865? It was $2.7 billion. That’s a jump that changes the entire scale of a graph. But even then, the country spent the next several decades slowly paying it down, or at least letting the growing economy make the debt look smaller by comparison.

Why the World Wars Changed the Scale Forever

If you look at the 20th-century portion of the US national debt historical graph, everything changes around 1917. World War I cost a fortune. But World War II? That was the game-changer.

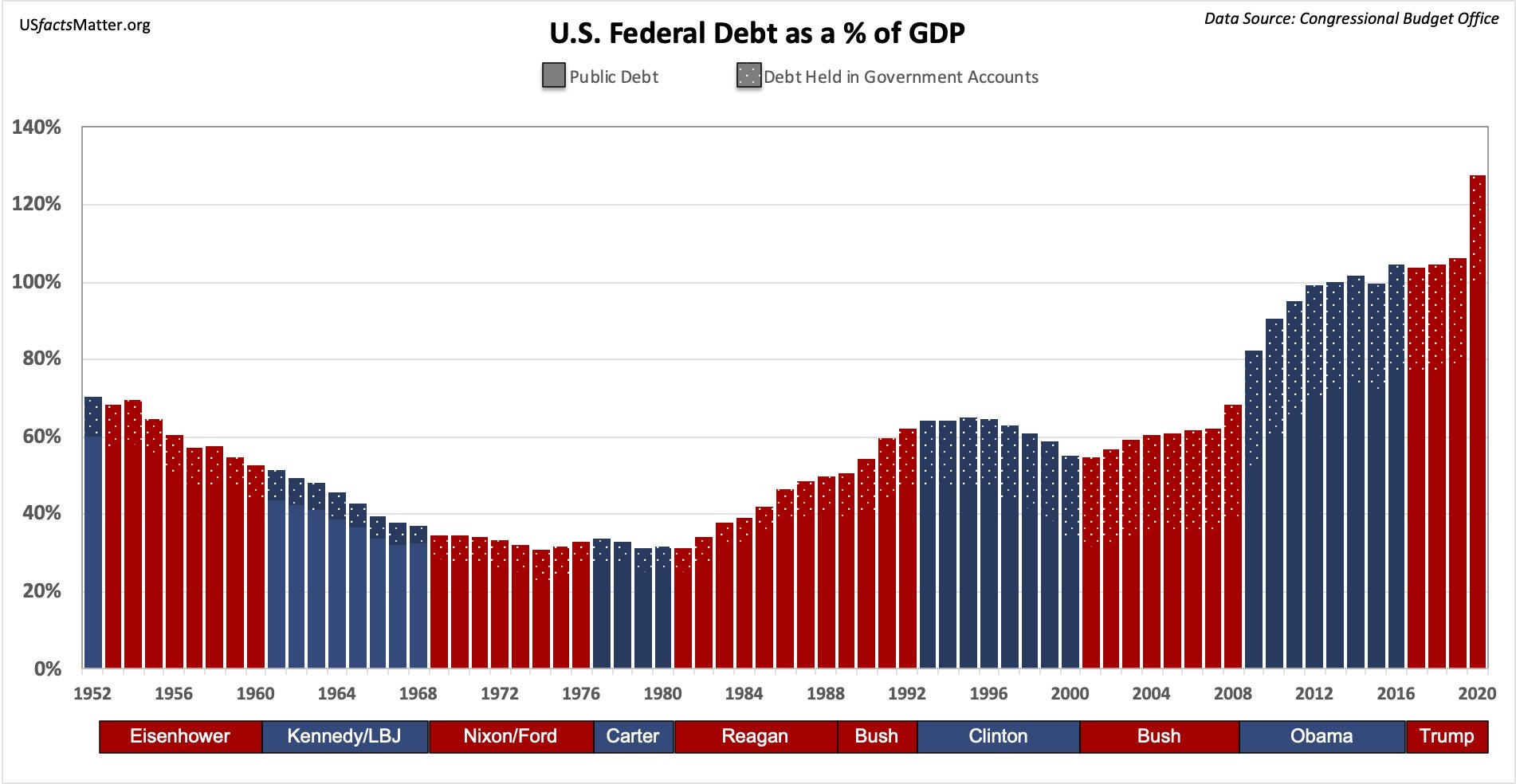

By the end of WWII, the debt-to-GDP ratio hit about 106%. That is a crucial metric. Economists often care less about the raw dollar amount and more about how much we owe compared to how much we produce. In 1946, the debt was huge, but the US was the only major industrial power left standing. We grew our way out of it. The line on the graph didn't necessarily drop in dollars, but as the American economy exploded in the 50s and 60s, the "burden" of that debt became a tiny fraction of our income.

It’s like having a $10,000 credit card balance. If you make $20,000 a year, you’re in trouble. If you suddenly start making $200,000 a year, that same $10,000 is barely a footnote in your monthly budget.

The Modern Era: Why the Line Just Won't Stop Going Up

Since the early 1980s, the graph has stopped behaving. We entered an era of "permanent" deficits. Reagan-era tax cuts combined with increased military spending started a trend that hasn't really reversed. Then you have the 2008 financial crisis.

When the housing market collapsed, the government stepped in with massive stimulus packages. The debt jumped. Then came COVID-19 in 2020. That spike is the most dramatic thing you'll see on the modern US national debt historical graph. The government injected trillions of dollars into the economy to keep things from totally disintegrating during the lockdowns.

A few things drive this today:

- Mandatory Spending: Social Security and Medicare take up a huge chunk of the pie. As the population gets older, these costs just keep rising.

- Interest Rates: This is the sneaky one. When the Federal Reserve raises rates to fight inflation, the cost of "carrying" the debt goes up. We end up borrowing money just to pay the interest on the money we already borrowed.

- Tax Revenue: We generally spend more than we take in. Every year the "gap" (the deficit) gets added to the total "pile" (the debt).

Understanding the "Intragovernmental" Weirdness

One thing the typical US national debt historical graph doesn't always show is who we actually owe the money to. People love to talk about "China owning our debt," but that’s actually a bit of a myth in terms of scale.

✨ Don't miss: Charles Kuck Immigration Attorney: Why the Most Feared Name in ICE Trials Still Matters

The biggest chunk of the debt is actually owed to... ourselves.

The Social Security Trust Fund, for instance, holds a massive amount of Treasury bonds. The Federal Reserve holds another huge portion. About 20% to 30% of the debt is "intragovernmental," meaning one part of the government owes it to another. The rest is "public debt," held by individual investors, pension funds, and foreign countries like Japan and China.

It's a weird loop. If the government "defaults" on its debt, it's basically defaulting on the retirement funds of its own citizens. That’s why the stakes are so high every time there is a debate about the debt ceiling in D.C.

Is the Graph Actually Sustainable?

There is no consensus here. That’s the messy truth.

Some economists, especially those who lean toward Modern Monetary Theory (MMT), argue that as long as a country prints its own currency, it can’t really "go broke" the way a household does. They think the limit isn't a dollar amount on a graph, but inflation. If we print too much, prices go up. If prices stay stable, keep spending.

Others, the "fiscal hawks," are terrified. They see the US national debt historical graph as a ticking time bomb. They worry that eventually, investors will lose trust in the US dollar. If people stop buying Treasury bonds, the whole system collapses.

The reality is probably somewhere in the middle. The US has a "reserve currency" status. The world runs on dollars. This gives us a "superpower" that other countries don't have. We can carry way more debt than, say, Greece or Argentina, because everyone still wants our currency. But that trust isn't infinite.

Practical Insights for the Average Person

Seeing that line go up on the US national debt historical graph can feel overwhelming, but it's better to use that information for your own financial planning rather than just stressing about it.

First, realize that the national debt is a major driver of inflation. When the government pumps money into the system, your dollars might lose purchasing power over time. This makes "hard assets" like real estate or a diversified stock portfolio more important for long-term savings.

Second, keep an eye on interest rates. The national debt and the Federal Reserve are locked in a dance. When the debt gets too high, the government might eventually feel pressured to keep interest rates lower than they "should" be just to keep the interest payments manageable. This affects everything from your mortgage rate to the yield on your savings account.

Lastly, don't buy into the "we're broke" rhetoric too easily. The US owns trillions in assets—land, gold, buildings, and the power to tax the most productive economy on earth. The graph is a warning sign, sure, but it's not a death certificate.

To stay informed, you should track the "Debt to GDP" ratio rather than just the raw number. It's a much more accurate reflection of the country's actual financial health. Check the Congressional Budget Office (CBO) reports once a year. They provide the most sober, non-partisan look at where the line is headed. Also, consider looking at your own "personal debt-to-income" ratio. It's the only graph you actually have total control over, and in an unstable macro-economy, having a clean personal balance sheet is the best hedge you can have.

🔗 Read more: Is the Stock Market Open on Christmas? What Most People Get Wrong

Understand that the debt is a policy choice. It’s the result of decades of decisions made by both parties. Until there is a fundamental change in how the country views spending versus taxation, that line on the US national debt historical graph is going to keep pointing toward the ceiling. Focus on what you can control: your own diversified investments, your skills, and your understanding of how these big macro-economic shifts actually trickle down to your grocery bill.