Money feels weird right now. You’ve probably noticed it at the checkout counter or when you’re staring at your utility bill. One day eggs are a bargain, the next they’re a luxury item. Honestly, everyone is trying to figure out what is current inflation rate in us and, more importantly, when it’s going to actually stop biting into their paychecks.

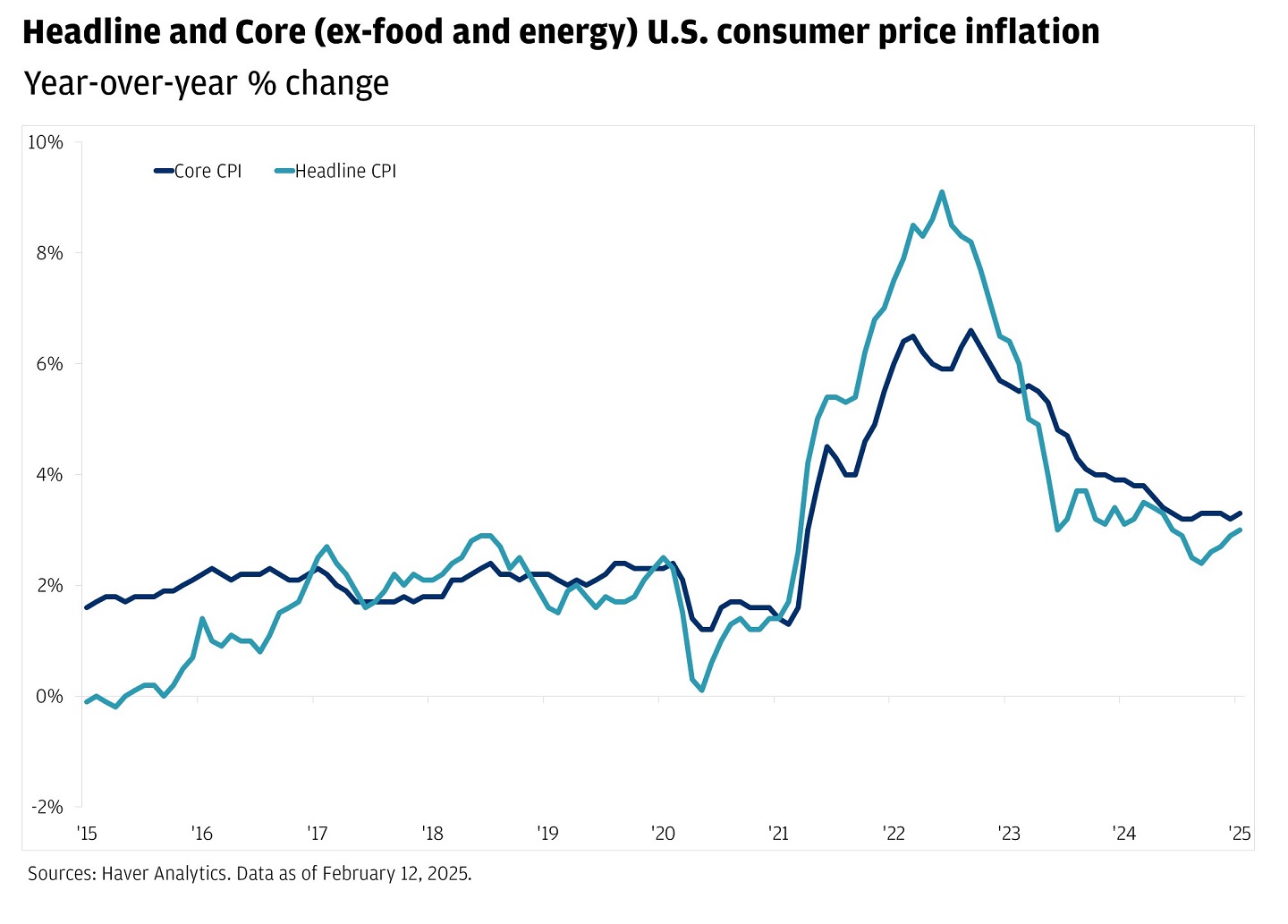

As of the latest data released by the Bureau of Labor Statistics (BLS) on January 13, 2026, the annual inflation rate in the US is sitting at 2.7%.

That number might sound low compared to the wild 9% peaks we saw a few years back, but it's a bit of a "sneaky" stat. It means prices are still going up—just at a slower pace than before. Think of it like a car that was going 90 mph and is now going 27 mph. You’re still moving forward; you're just not flying through the windshield anymore.

Breaking Down the 2.7% Number

Basically, that 2.7% headline number is the Consumer Price Index (CPI). It’s the "everything" bucket—milk, rent, gas, haircuts, you name it. But if you strip out the volatile stuff like food and energy (which jump around whenever there’s a storm or a geopolitical spat), you get what economists call Core CPI.

Right now, Core CPI is hovering around 2.6%.

Here is how that actually hits your wallet on a month-to-month basis:

- Food prices: They rose about 3.1% over the last year. If you’ve felt like eating out is becoming a "special occasion only" activity, that’s why. Full-service meals are up significantly, while your grocery store staples have stayed a bit flatter.

- Shelter: This is the big one. It’s the largest factor in the current inflation rate. Rent and "owners' equivalent rent" are still up over 3%, making it the stickiest part of the economy to cool down.

- Energy: This has been the "good news" recently. Gasoline prices actually dropped about 3.4% year-over-year, which is basically the only reason the headline inflation rate isn't much higher.

Why the Fed Is Sweating

The Federal Reserve has a target. They want inflation at 2%. We aren't there yet. Because the labor market is still relatively solid and people are still spending—thanks in part to those tax cuts from the "One Big Beautiful Bill Act" (OBBBA)—the Fed is being super cautious.

👉 See also: Rite Aid West Kittanning PA: What’s Actually Going On With Your Local Pharmacy

Jerome Powell, whose term ends this May, is walking a tightrope. If he cuts interest rates too fast to help the housing market, he risks sparking another round of price hikes. If he holds them too high, he might accidentally trip the economy into a recession. Currently, the federal funds rate is between 3.5% and 3.75%, following a few cuts at the end of 2025.

The "Real" Cost of Living vs. The Official Stats

If you talk to most people, they’ll tell you 2.7% feels like a lie.

That’s because inflation is cumulative. Prices didn't drop back to 2019 levels; they just stopped rising so fast. Since 2020, the total cost of living has jumped more than 25% for many households. So, while the rate of increase is lower, the level of prices is still at an all-time high.

For seniors, this is a massive deal. The Social Security Administration announced a 2.8% Cost-of-Living Adjustment (COLA) for 2026. While that’s an extra $50 or $60 a month for the average retiree, many advocacy groups like The Senior Citizens League argue it’s not enough to cover the surging costs of healthcare and senior-specific needs.

What’s Coming Next for Prices?

Forecasters from places like Goldman Sachs and J.P. Morgan are cautiously optimistic, but they aren't popping champagne yet. Most experts think we'll see a "low-grade fever" of inflation throughout the first half of 2026.

There are a few "wildcards" that could change what is current inflation rate in us by the end of the year:

- Tariff Pressures: New trade policies have put upward pressure on the cost of imported goods. This is likely to keep "goods inflation" from dropping to zero anytime soon.

- The Housing Lag: Shelter costs take a long time to show up in official data. We’re finally seeing new lease rates slow down, which should help pull the official inflation number down toward 2.4% by December.

- Fiscal Stimulus: Between tax refunds and potential new spending before the mid-term elections, there’s a lot of cash flowing into the system. More cash usually means more spending, which can keep prices "sticky."

Actionable Steps to Protect Your Wallet

Since we’re likely stuck with these price levels for a while, you've gotta be proactive. You can't control the Fed, but you can control your own "personal inflation rate."

- Audit Your Subscriptions (Again): Service inflation is higher than goods inflation. Check those "ghost" subscriptions you signed up for in 2025.

- Lock in Fixed Costs: If you’re a renter and see a chance to sign a longer lease while the market is slightly cooling, take it. Shelter is the most persistent cost.

- High-Yield is Still Your Friend: With interest rates still above 3.5%, keep your emergency fund in a high-yield savings account. You’re finally earning a real return that actually beats the current inflation rate.

- Watch the "Big Beautiful" Tax Changes: Make sure you’re taking advantage of the new tax breaks on overtime and tips if you work in those sectors. It’s basically a government-subsidized hedge against rising prices.

Inflation is a slow-moving beast. While the 2.7% we're seeing in early 2026 is a far cry from the crisis levels of a few years ago, it still requires a strategy. Pay attention to the next CPI release on February 11—that's the one that will tell us if the New Year's price hikes are actually starting to fade or if we’re in for a longer "fever" than we hoped.