Money is weird. We talk about it constantly, yet most of us are basically guessing when it comes to what everyone else is actually making. If you look at the official data for the US household average income, the numbers look one way on a spreadsheet and completely different when you're staring at a grocery bill in a city like Seattle or a small town in Ohio.

The most recent data from the U.S. Census Bureau—specifically the "Income in the United States: 2023" report released in late 2024—tells us the real median household income was $80,610. That was a 4% increase from the year before. Sounds great, right? Honestly, it’s the first time since 2019 that we’ve seen a statistically significant raise after adjusting for the inflation monster that’s been eating our paychecks. But here is the thing: average and median are not the same. If Jeff Bezos walks into a dive bar, the average income in that room becomes billions of dollars. The median, however, stays the same. That’s why the median is usually the number you should actually care about.

The Massive Gap Between "Average" and "Reality"

When people search for the US household average income, they often get hit with a number that feels... high. According to the St. Louis Fed and Census data, the mean (average) household income often sits well above $110,000. Why the massive gap between the $80k median and the $110k+ average?

It’s the top 5%.

In the U.S., income inequality isn’t just a political talking point; it’s a mathematical reality that skews the data. If you’re living in a household making $80,000, you are right in the middle. You’re the "typical" American experience. But because the highest earners pull in such astronomical sums, the "average" gets dragged upward, making the rest of us feel like we’re falling behind even when we’re actually doing okay compared to our neighbors.

Geography changes everything. You can't compare a $100k salary in San Francisco to $100k in Gulfport, Mississippi. In Mississippi, you’re basically royalty. In the Bay Area, you might be looking for a roommate.

Why 2026 is Feeling Different

We are deep into the mid-2020s now, and the "vibecession"—that weird period where the data said the economy was good but everyone felt broke—is finally starting to scab over. But the scars are there. Rent is still sticky. Insurance premiums for cars and homes have skyrocketed by 20% or more in some states. So even if the US household average income is technically rising, the "disposable" part of that income feels smaller than ever.

It's about purchasing power.

🔗 Read more: Enterprise Products Partners Stock Price: Why High Yield Seekers Are Bracing for 2026

The Demographic Divide: Who is Actually Making the Money?

Age matters. A lot.

If you’re in your 20s, looking at the national average is a recipe for a mid-life crisis at age 24. Householders aged 45 to 64 typically see the highest earnings, often averaging well over $110,000 as they hit their peak career years. Meanwhile, the Gen Z crowd and the retirees are naturally pulling the numbers down.

Then you have the education factor. It’s a cliché because it’s true: households headed by someone with a bachelor’s degree earn roughly double what high school-only households bring home. According to the Bureau of Labor Statistics (BLS), the gap hasn't narrowed; if anything, the premium for specialized skills in AI, healthcare, and green energy is widening the divide.

The Race and Gender Narrative

We have to talk about the gaps. They’re real.

Asian households consistently report the highest median incomes, often crossing the $100,000 threshold. White households follow, while Black and Hispanic households continue to trail, though the gap has narrowed slightly in the last 36 months due to a tight labor market that forced employers to raise wages at the bottom of the ladder.

- Asian: ~$109,000

- White (Non-Hispanic): ~$84,000

- Hispanic: ~$65,000

- Black: ~$53,000

Note: These are approximations based on the most recent Census trends.

It isn't just about "effort." It's about systemic access, types of industries worked, and generational wealth. When we look at the US household average income, we are looking at a mosaic, not a monolith.

Inflation: The Silent Paycheck Eater

You got a 3% raise? Cool. Inflation was 3.5%? You actually got a 0.5% pay cut.

This is the "Real Income" trap. The Census Bureau uses the Consumer Price Index (CPI-U-RS) to adjust these numbers so we can compare 2026 to 1996. When you hear that the US household average income is at an all-time high, you have to ask if that’s in "nominal" dollars or "real" dollars.

💡 You might also like: Dollar Against Saudi Riyal: Why the 3.75 Peg Refuses to Break

Most people are just tired.

They are tired of the "side hustle" culture. In 2026, about 39% of Americans have a side job. That income counts toward the household total. So, if the average is going up, is it because jobs are better, or because Mom and Dad are both working 50 hours a week plus driving Uber on Saturdays? The data suggests it’s a bit of both. We are working more to stay in the same place.

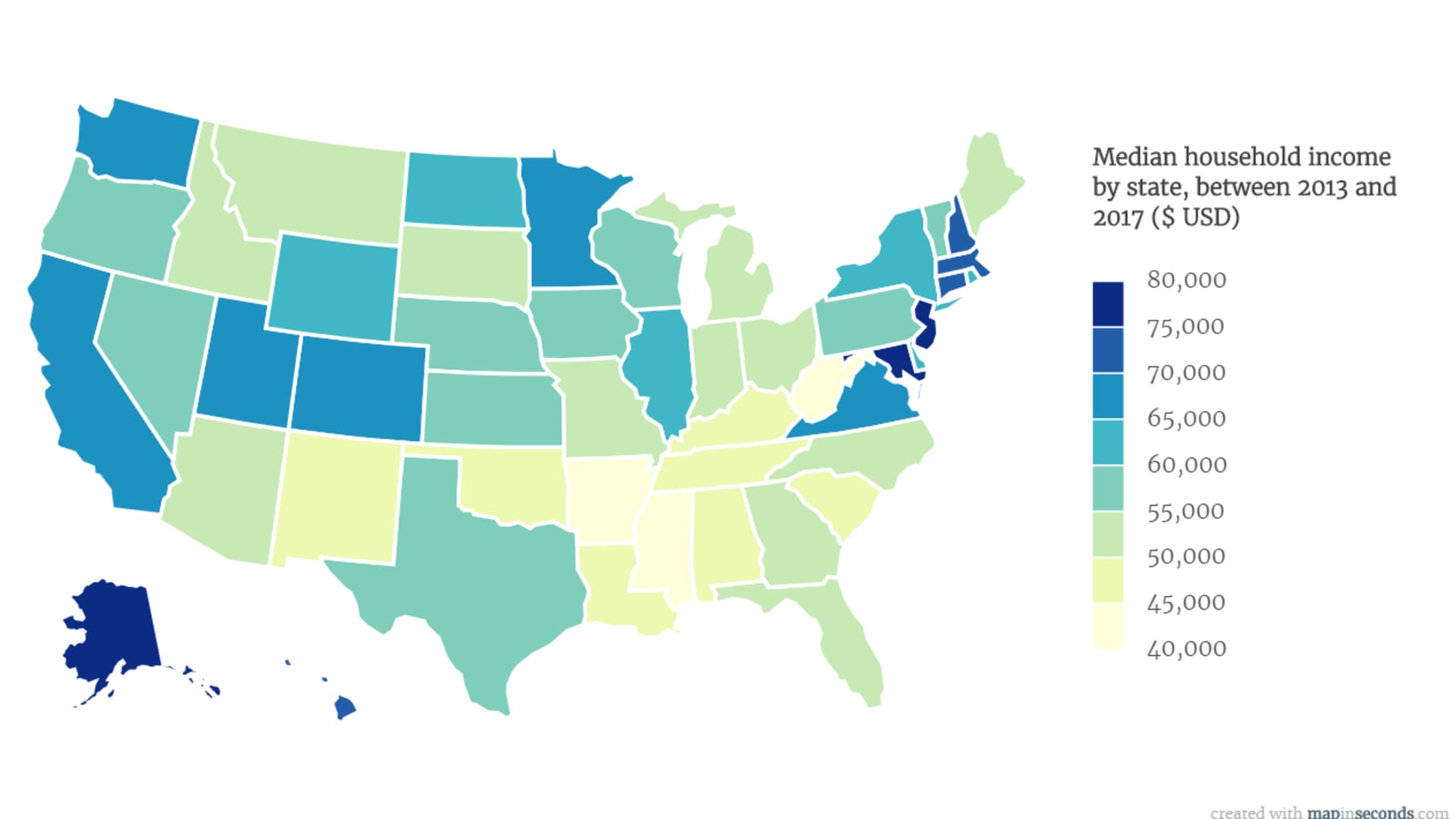

The Regional Reality Check

Let’s look at the states. Maryland, Massachusetts, and New Jersey consistently fight for the top spot, with median incomes often flirting with six figures. On the flip side, West Virginia and Mississippi usually sit at the bottom.

But look at the "Real Regional Price Parities." This is a fancy term the Bureau of Economic Analysis uses to show what a dollar actually buys. A $75,000 income in Arkansas might actually give you a better lifestyle than $130,000 in New York City.

People are moving because of this.

The "Great Migration" to the Sunbelt wasn't just about the weather. It was a mathematical escape. People left high-tax, high-cost-of-living areas to find a place where the US household average income actually meant you could buy a three-bedroom house without selling a kidney.

What Most People Get Wrong About These Stats

Most people think "Household" means "Family."

Nope.

A household is anyone living in a housing unit. It could be a single guy and his dog. It could be four roommates in a college town. It could be a traditional nuclear family. When you see that the US household average income is $80k, remember that a lot of those "households" have two or even three earners.

📖 Related: Cox Tech Support Business Needs: What Actually Happens When the Internet Quits

If you’re a single person making $60,000, you might feel "below average." But compared to other single-person households, you’re actually doing quite well. The data gets skewed because we’re lumping together a dual-income power couple in D.C. with a single retiree in Florida.

Actionable Steps: How to Benchmarking Your Own Income

Stop comparing yourself to the national average. It’s useless. Instead, do this:

Check your local ZIP code data. The Census Bureau’s "American Community Survey" (ACS) lets you drill down to your specific town. That is your actual competition for housing and services. If the median in your town is $100k and you're making $70k, you'll feel poor. If the median is $50k, you’re the wealthy neighbor.

Calculate your "Real" wage growth. Take your percentage raise from last year and subtract the current inflation rate. If the number is negative, it's time to negotiate or jump ship. The "loyalty discount" is real; people who change jobs every 2-3 years still see higher income growth than those who stay put.

Look at your Debt-to-Income (DTI) ratio. Income is only half the story. A household making $150,000 with $4,000 in monthly debt payments is in worse shape than a household making $70,000 with zero debt.

Max out the "Invisible" income. If your employer offers a 401k match, that is part of your income. It doesn't show up in the Census US household average income stats, but it’s the difference between retiring at 60 or working until you’re 75.

Diversify your income streams. The most resilient households in 2026 aren't just relying on one W-2. Even a small stream of dividends, rental income, or freelance work creates a buffer.

The national average is a benchmark, a pulse check for the country's health. But your household is a micro-economy. Focus on your personal "Real Income" and your local cost of living. That’s the only way to make the numbers actually mean something for your life.

To get a true sense of where you stand, use the IRS Tax Bracket tables alongside the Census data. This helps you see how much of that "average" income is actually hitting your bank account after Uncle Sam takes his cut. Understanding the difference between gross income and net take-home pay is the first step toward actual financial literacy in an increasingly expensive world.