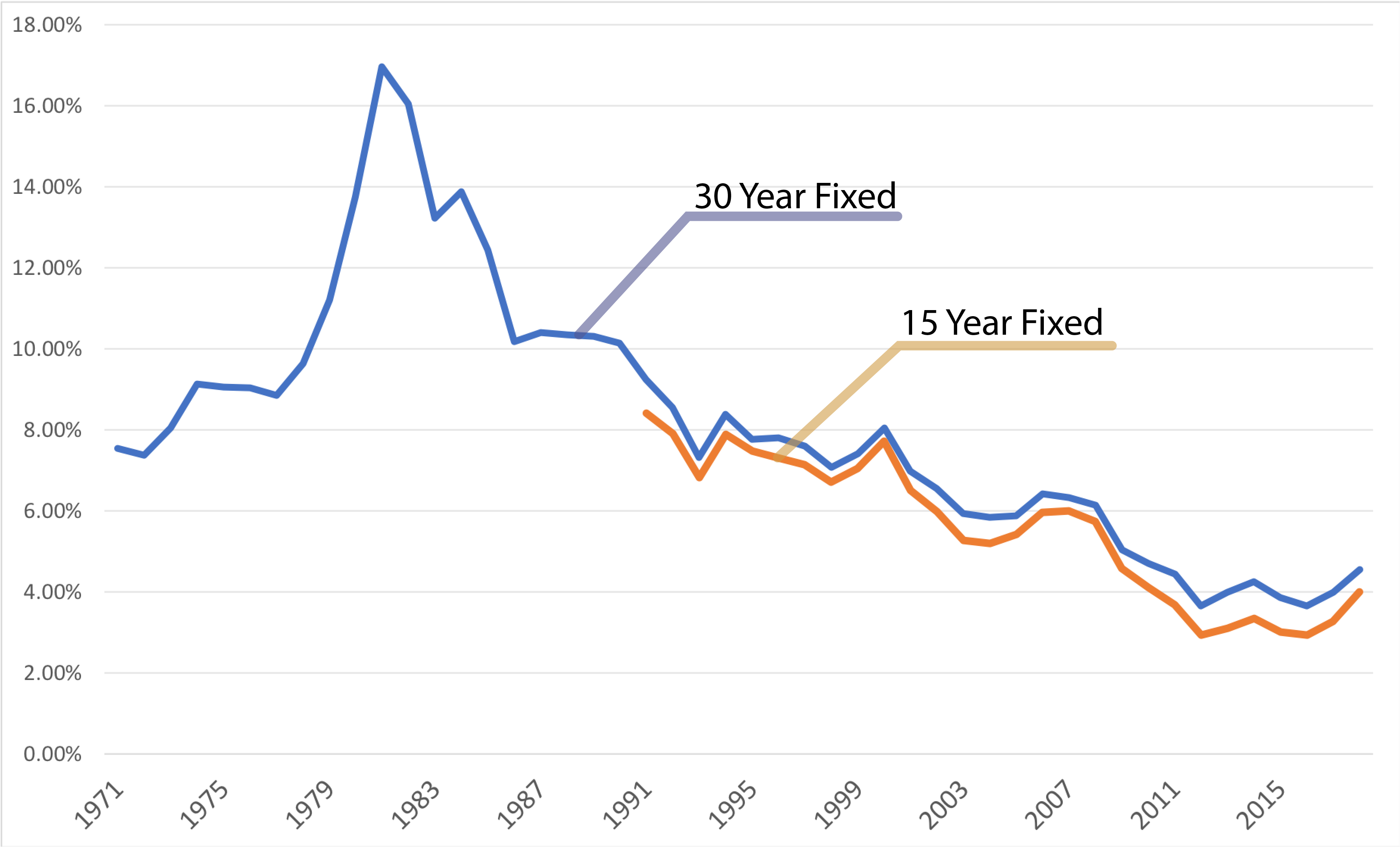

If you look at a US historical interest rates chart, you’ll see something that looks less like a steady climb and more like a terrifying EKG. It’s messy. It’s chaotic. Honestly, it’s a direct reflection of every major panic, boom, and "oops" moment in American economic history since the 1950s. Most people checking these charts today are just trying to figure out if they should buy a house or if their savings account is finally going to pay for a decent dinner. But the truth is, where we are right now isn’t actually that weird—it’s the last decade that was the anomaly.

Money used to cost something. For most of the 20th century, you couldn't just borrow cash for basically free. We’ve been living in a strange, low-rate bubble since 2008, and our collective memory has suffered for it. When the Federal Reserve nudges the "federal funds rate," they aren't just playing with numbers; they are trying to keep the entire ship from sinking or overheating.

Why the 1981 Peak Still Scares Economists

The 1980s were wild for more than just hairspray and synth-pop. If you find a US historical interest rates chart and look at the year 1981, you’ll see a spike that looks like a mountain peak. The federal funds rate hit an unbelievable 20%. Imagine trying to get a mortgage when the base rate is 20%. People were paying 18% or more on home loans. It sounds like a fever dream today, but back then, it was a desperate necessity to kill the monster of "Great Inflation."

Paul Volcker, the Fed Chair at the time, basically decided to break the economy's back to save its soul. He was not a popular man. He faced protests and "wanted" posters from homebuilders. But inflation was running at nearly 15% in 1980, and the dollar was losing value so fast that people were hoarding goods. By cranking rates to the moon, Volcker stopped the bleeding. It caused a brutal recession, but it also set the stage for two decades of relative stability.

The lesson here is simple: the Fed will hurt you to save the currency. They’ve done it before, and they’ll do it again. It’s a blunt instrument. When you see that 20% spike on a chart, you’re looking at the ultimate economic "reset button."

The Long Slide into the Zero-Bound Era

After the Volcker shock, the general trend on any US historical interest rates chart is a long, jagged slide downward. From the mid-80s through the 90s, rates bounced between 3% and 10%. This was the era of "Great Moderation." Alan Greenspan became a sort of economic rockstar by fine-tuning the dial. Whenever things got a little slow, he’d drop rates. When the "irrational exuberance" of the dot-com bubble hit, he’d nudge them back up.

🔗 Read more: We Are Legal Revolution: Why the Status Quo is Finally Breaking

Then came 2008.

The Great Financial Crisis didn't just change the rules; it burned the rulebook. For the first time, the Fed dropped rates to effectively zero. They stayed there for years. This is what economists call the "Zero Lower Bound." It was supposed to be a temporary emergency measure, like an adrenaline shot to a stopped heart. Instead, we stayed on the IV drip for nearly a decade. This distorted everything. It made "risky" investments look safe because there was nowhere else to put your money. If your bank account pays 0.01%, you're going to buy tech stocks or crypto or anything that moves.

The Real Cost of "Free" Money

When money is free, people do weird stuff. We saw the rise of "zombie companies" that only stayed alive because they could borrow cheaply to pay off old debt. We saw housing prices rocket because a $500,000 mortgage is a lot easier to swallow at 2.5% than at 7%.

- 1970s: Rates averaged around 7-9%.

- 2010-2015: Rates averaged near 0%.

- The 2020s: We are currently seeing a "return to normalcy" that feels like a crisis because we forgot what normal looks like.

Understanding the "Real" Rate vs. the Nominal Rate

Looking at a US historical interest rates chart only tells half the story if you don't look at inflation. If the bank pays you 5% interest, but bread prices go up 10%, you’re actually losing 5% of your purchasing power. That’s the "real" interest rate. In the late 70s, even though rates were high, they were often lower than inflation. You were actually being paid to borrow money because you’d pay it back with dollars that were worth significantly less.

Today, the Fed is trying to keep the real rate positive. They want your money to actually grow in the bank, but only just enough to keep you from spending it all at once and driving prices up. It’s a balancing act that usually ends in someone getting hurt. Usually, that’s the labor market.

💡 You might also like: Oil Market News Today: Why Prices Are Crashing Despite Middle East Chaos

How Policy Shifts Ripple Through Your Wallet

When the Fed moves, everyone else reacts. Banks look at the federal funds rate and then add their "spread."

- The Fed sets a target (say, 5%).

- Banks look at their risk and add a couple of percentage points for a mortgage.

- Credit card companies add a lot of percentage points (sometimes 15-25%).

- Suddenly, your "affordable" car payment is $200 more a month.

Misconceptions About Why Rates Move

A lot of people think the President controls interest rates. They don't. At least, they aren't supposed to. The Federal Reserve is designed to be independent. They have a "dual mandate": keep prices stable (low inflation) and keep people employed. Sometimes these two goals fight each other. If everyone is working and spending, prices go up. To stop prices from going up, the Fed has to slow down the economy, which might make people lose jobs.

It's a grim trade-off.

Another myth is that high rates are always bad. Honestly, for savers and retirees, the 2010s were a nightmare. If you were living on a fixed income, you got nothing from your CDs or bonds. Higher rates mean you can actually get a return on your "safe" money without having to gamble in the stock market. It brings balance back to the system.

Historical Data Points You Should Know

Looking back at the St. Louis Fed (FRED) data, you can see specific moments where the chart breaks.

📖 Related: Cuanto son 100 dolares en quetzales: Why the Bank Rate Isn't What You Actually Get

- October 1979: The "Saturday Night Special." Volcker announced a radical shift in how the Fed managed the money supply. Rates jumped almost instantly.

- The 1950s: Rates were incredibly low, often below 2%, as the US paid off WWII debt. This was a period of "financial repression" where the government intentionally kept rates low to make their own debt cheaper.

- 2022-2023: One of the fastest hiking cycles in history. After years of saying inflation was "transitory," the Fed realized they were behind the curve and slammed on the brakes.

Actionable Insights for the Current Market

So, what do you actually do with this information? Staring at a US historical interest rates chart is only useful if it changes your behavior.

First, stop waiting for 3% mortgages. Unless there is a catastrophic global recession, we aren't going back to the "free money" era of 2020 anytime soon. That was a black swan event. Planning your life around a return to 2% or 3% rates is a losing game. Historically, a 5-6% mortgage is actually pretty good.

Second, look at your "Real" yield. If you’re sitting on cash, make sure it’s in a High-Yield Savings Account (HYSA) or a money market fund. If the Fed is at 5% and your big-name bank is paying you 0.1%, you are literally giving your money away to the bank.

Third, watch the "Inverted Yield Curve." This is when short-term interest rates are higher than long-term rates. It’s a weird glitch on the chart that has predicted almost every recession in the last 50 years. When it happens, it means investors are pessimistic about the near future. If you see people talking about an "inversion," it's time to check your emergency fund.

Finally, understand that the Fed is reactionary. They don't predict the future; they react to last month's data. This means they often overcorrect. They stay too low for too long, then they stay too high for too long. If you're looking to borrow, the best time is often right when the "pain" in the economy becomes unbearable for the general public, because that's when the Fed is forced to pivot.

Don't let the headlines panic you. Interest rates are a tool, not a death sentence. By understanding the historical context, you can see that we aren't in "unprecedented" times—we're just back to the way the world worked for most of the last century.

To manage your own finances effectively, start by calculating your total debt-to-income ratio under current rates versus a potential 2% increase. This "stress test" will tell you more about your financial health than any chart ever could. Check your credit card APRs today; many have crept up to 25% or higher without users noticing. Moving that balance to a fixed-rate loan or a 0% transfer card should be your immediate priority if the "high rate" era continues.