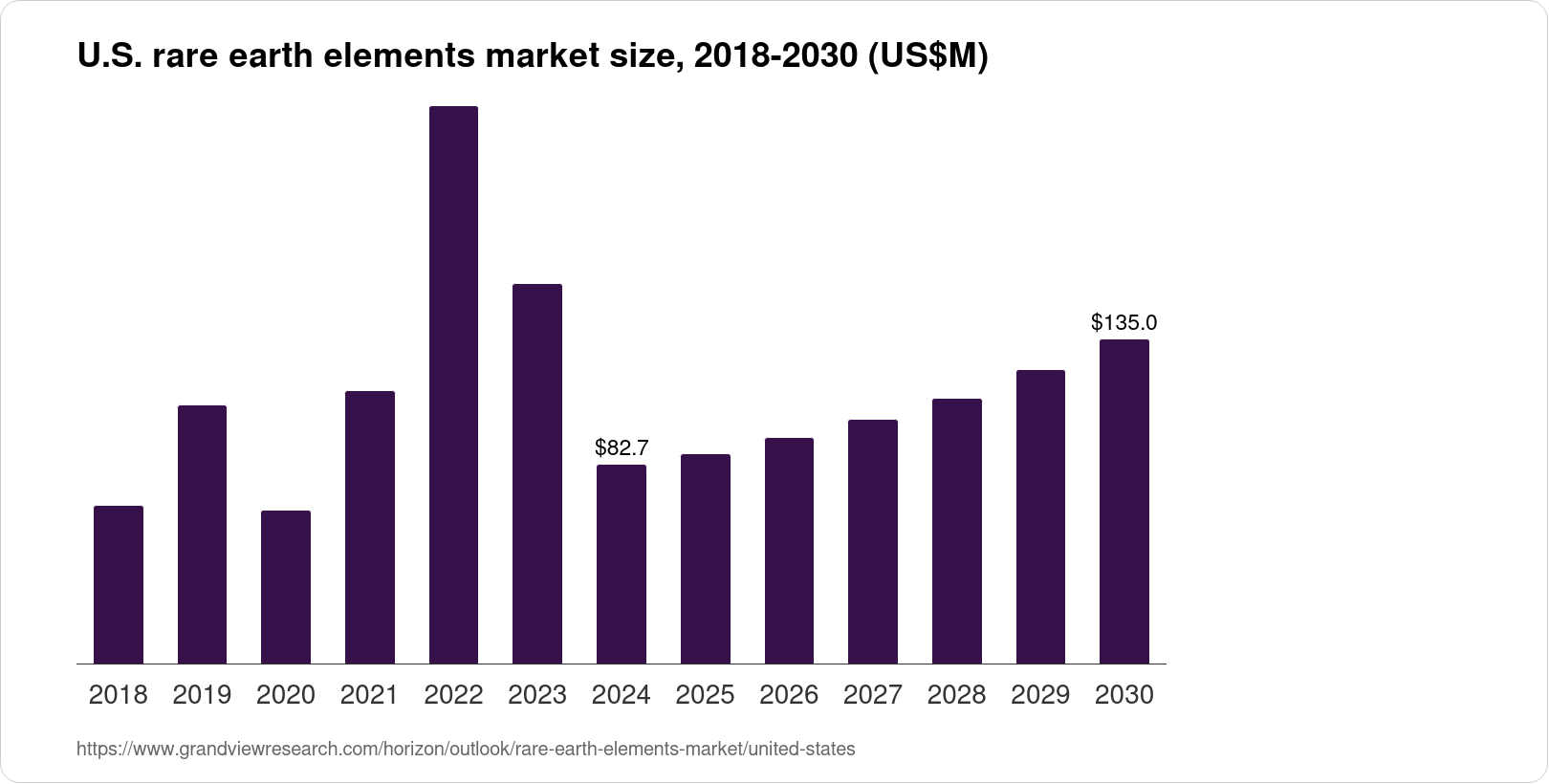

Honestly, most people think rare earth elements are actually rare. They aren’t. You can find cerium or lanthanum in the dirt in your backyard if you look hard enough. The problem isn't finding them; it's the nightmare of getting them out of the ground without destroying the environment and then processing them into something useful. For decades, the United States rare earth industry basically hit the snooze button. We let China take over the entire board because it was cheaper and easier to let someone else handle the toxic chemical baths required for separation.

Now? Everything is different.

If you look at the magnets in an F-35 fighter jet or the motor of a Tesla, you’re looking at a massive geopolitical headache. We’ve realized that being 100% dependent on a single trade partner for the "vitamins" of modern technology is a bad strategy. It’s a scramble. It's messy. And it's happening right now in places like Mountain Pass, California, and tiny industrial towns in Texas.

The Mountain Pass Resurrection

You can't talk about United States rare earth production without starting at Mountain Pass. It's this massive open-pit mine in San Bernardino County. Back in the 60s and 70s, it was the world's primary source. Then, environmental regulations got tighter, labor costs went up, and Molycorp (the former owner) went bankrupt after a spectacular, billion-dollar failure to modernize.

MP Materials bought the site out of bankruptcy in 2017.

For a few years, they were just digging up the ore and shipping it straight back to China for processing. It was kind of ironic. We were mining our own dirt just to buy it back as finished magnets. But as of late 2024 and heading into 2026, the "Stage II" optimization at Mountain Pass is finally humming. They are actually separating the heavy and light rare earths on-site. This is a huge deal because it cuts the cord on the mid-stream processing monopoly.

👉 See also: 1 dirham us dollar: Why the rate never actually moves

James Litinsky, the CEO of MP Materials, has been vocal about this being a "mission-critical" endeavor for national security. It’s not just about profit margins anymore. It’s about making sure that if a trade war turns into a cold war, the US isn't left with a bunch of high-tech designs and no materials to build them.

Why Neodymium Is the Real King

Forget gold. If you want to understand the modern economy, watch Neodymium (Nd) and Praseodymium (Pr).

These are the "magnet metals."

When you mix them with iron and boron, you get the strongest permanent magnets known to man. Without these, your electric vehicle (EV) motor would be twice as big and half as efficient. Your iPhone wouldn't vibrate. Your wind turbines wouldn't generate nearly as much juice.

The United States rare earth strategy is currently obsessed with these two elements.

While there are 17 rare earth elements in total, most of them—like Holmium or Thulium—are used in tiny amounts for niche medical lasers or research. The big money and the big risk are in the magnet metals. The Department of Defense (DoD) has been throwing money at companies like Lynas Rare Earths to build a separation facility in Texas. Why? Because a single Virginia-class submarine requires about 9,200 pounds of rare earth materials. You can't just "innovate" your way out of needing the raw atoms.

The Hidden Cost of "Clean" Energy

Here is the awkward truth no one likes to discuss at dinner parties: mining is dirty.

Rare earth ores are often found alongside thorium and uranium. They’re radioactive. To get the metals out, you have to crush the rock and douse it in a cocktail of acids. In the past, the US struggled with this because the tailings ponds (the big pools of leftover toxic sludge) kept leaking.

China’s dominance wasn't just about cheap labor; it was about a lower barrier for environmental compliance in the 90s.

To make United States rare earth mining viable again, companies are using "closed-loop" systems. They’re trying to recycle the water and the chemicals. It’s more expensive. A lot more. But the "green" transition is a bit of a lie if we’re destroying a mountain range in another country to build "eco-friendly" cars here. The push for domestic mining is forcing a reckoning with how much we’re willing to pay for "clean" tech.

Breaking the Monopoly in Round Top

Out in Hudspeth County, Texas, there's a project called Round Top. It’s being developed by USA Rare Earth.

👉 See also: Documented Loss Cash Payment Meaning: What You Actually Get After a Claim

What makes this spot weird is that it’s not just a rare earth mine. It’s a rhyolite-hosted deposit, which sounds boring, but it means the metals are tucked into the rock in a way that might be easier to leach out with heap leaching—basically dripping acid over a pile of rocks.

They’re also looking for lithium there.

This "multi-commodity" approach is basically the only way to make the economics work. If you only mine for one thing, and the price of that thing drops because China decides to flood the market (which they’ve done before), you go broke. If you’re mining for five different high-value minerals at once, you have a safety net.

The Recycling Pipe Dream vs. Reality

You’ll hear a lot of people say, "Why don't we just recycle the magnets in old hard drives?"

It's a great idea. In theory.

In reality, it’s a logistical nightmare.

Apple has robots like "Daisy" that can tear apart iPhones, but the volume of rare earths recovered is tiny compared to the demand for new EV fleets. Companies like Solvay and Umicore are working on better recovery methods, but we are decades away from a circular economy for these metals. We have to dig. There is no way around the shovel.

The Biden-Harris administration (and likely whoever follows) has leaned heavily into the Defense Production Act to fund these mines. It’s one of the few things both sides of the aisle actually agree on. Nobody wants to be the politician who let the US military run out of the magnets needed for missile guidance systems.

What Most People Get Wrong About Prices

People see the price of United States rare earth stocks cratering and think the industry is dying. It’s not. It’s just volatile.

💡 You might also like: Today Myanmar Money Exchange Rate: Why the Official Numbers Are Only Half the Story

China controls the "faucet." If they want to kill off US competition, they can just turn the faucet on, drop prices, and wait for the American startups to run out of cash. This is why "offtake agreements" are so important. This is basically a contract where a company like GM or Tesla says, "We will buy your Neodymium at X price for the next ten years, no matter what the global market does."

Without those contracts, no bank will lend the hundreds of millions needed to build a refinery.

Actionable Steps for the Near Future

If you’re watching this space—whether as an investor, a tech enthusiast, or someone worried about the supply chain—here is how the next 24 months actually play out.

- Watch the heavy separation plants: Keep an eye on the progress of the HRE (Heavy Rare Earth) facility in Seadrift, Texas. This is the real litmus test for whether we can handle the "heavy" elements like Dysprosium, which are even harder to process than the light ones.

- Track the Pentagon's checks: The DoD is the biggest venture capitalist in this space right now. If they stop funding a project, it’s probably dead. If they double down, it’s a strategic priority.

- Look for "China Plus One" sourcing: When you buy tech, look at where the components are sourced. Companies are starting to brag about "Non-Chinese Sourced" magnets as a selling point for reliability.

- Monitor the Permitting Reform: The biggest bottleneck for United States rare earth growth isn't the geology; it's the paperwork. If the federal government doesn't streamline the 7-to-10-year waiting period for new mines, the US will remain behind the curve.

The reality of the United States rare earth landscape is that we are in a transition period. We’ve moved from "complete dependence" to "active construction." It’s a long road. It involves a lot of sulfuric acid, a lot of government grants, and a lot of grit. But the days of 100% reliance on a single source are ending, mostly because they have to. There isn't a Plan B.