Honestly, trying to figure out the United States inflation rate right now feels a bit like trying to read a map while someone is shaking the car. One day you hear everything is fine, and the next, your grocery bill makes you want to crawl under a rock.

As of January 2026, the official numbers are out, and they tell a story that isn't exactly a horror movie, but it's definitely not a fairy tale either.

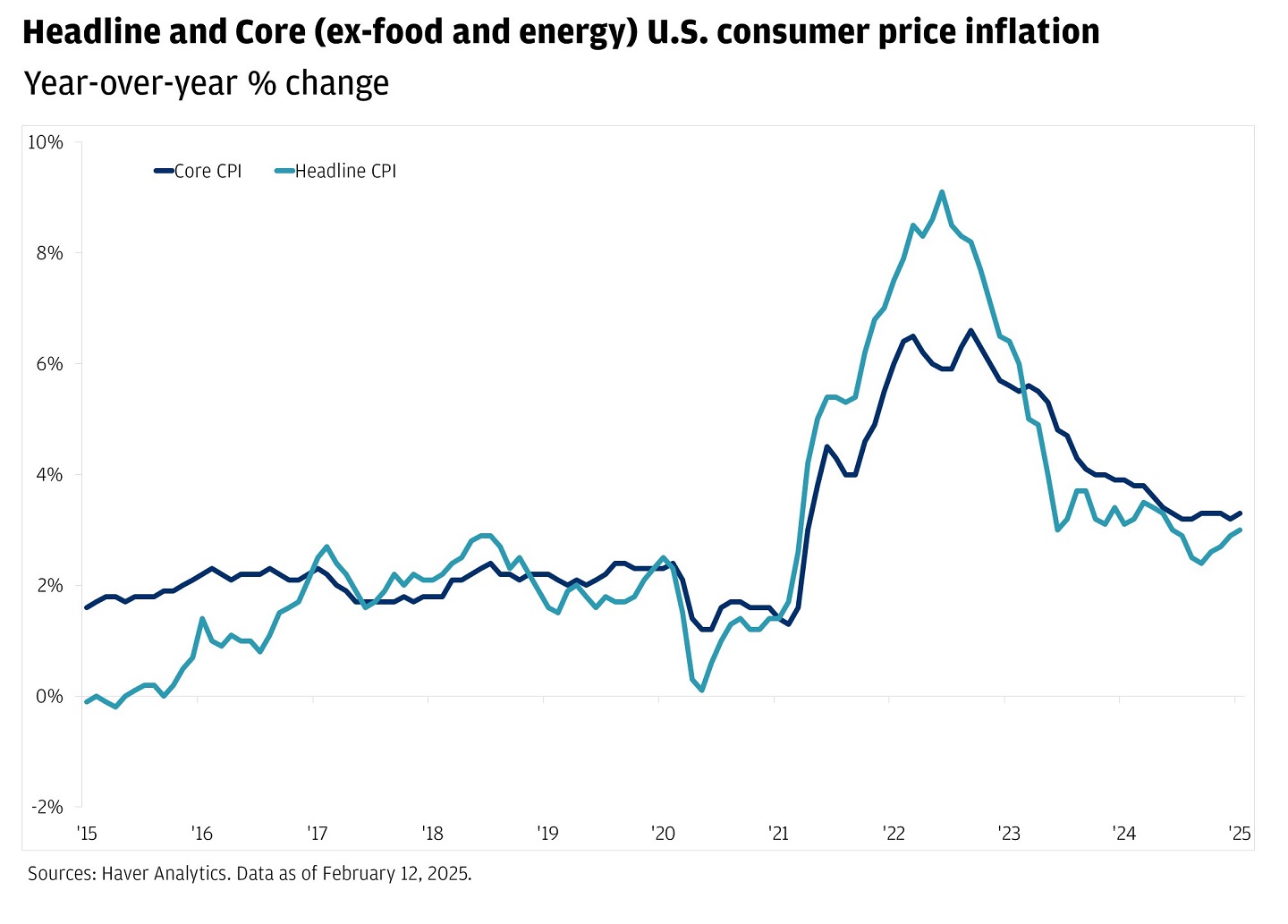

The latest data from the Bureau of Labor Statistics (BLS) shows the annual inflation rate sitting at 2.7%.

👉 See also: Is My Money Safe in the Bank? What the Experts Won't Say Out Loud

That’s basically where it’s been hanging out for a few months. It sounds low compared to the wild 9% peaks we saw back in 2022, but if you’re waiting for prices to actually drop, you might be waiting a long time. Inflation just means prices are rising slower, not that they’re going back to what they were in 2019.

The Reality Behind the 2.7% Number

Numbers are kinda cold. They don't care that you just paid eight dollars for a box of cereal.

When the government says the United States inflation rate is 2.7%, they’re looking at a massive basket of goods called the Consumer Price Index (CPI). But your personal "inflation rate" depends entirely on what you buy.

Why your wallet feels thinner

If you’re driving a gas-guzzler, you might actually be feeling okay. Gasoline prices dropped about 3.4% over the last year. That’s a win.

But then you walk into the grocery store. Food at home is up 2.4%, and if you like eating out, "food away from home" has jumped a whopping 4.1%.

It’s this weird tug-of-war.

Energy is pulling the number down, while the stuff you actually need to survive—like a roof over your head and a sandwich—is pulling it back up. Shelter costs, which include rent and "owners' equivalent rent," are still the biggest headache, rising 3.2% year-over-year.

The Core Inflation Problem

Economists love to talk about "Core CPI." This is basically the inflation rate if you ignore food and energy.

Why? Because gas and eggs are "volatile." Their prices jump around like a toddler on a sugar high.

Right now, Core inflation is at 2.6%. The Federal Reserve (those folks who control your interest rates) really wants that number to be 2.0%. We’ve been stuck above that target for 58 months now. That is a long time to be "almost there."

What’s Actually Driving Prices in 2026?

You've probably heard a dozen different reasons for why things are expensive. Is it corporate greed? Government spending?

It's usually a messy mix of both, plus a few things people don't talk about enough.

The Tariff Effect

Tariffs are the big talking point in early 2026. Goldman Sachs economists, like David Mericle, have pointed out that tariffs have been "masking" progress. Basically, as other costs were coming down, new import taxes on goods like semiconductors and apparel were pushing them back up. Experts at RBC Economics think this "tariff passthrough" won't even peak until the second quarter of this year.

The Labor Squeeze

People are getting paid more, which is great for them, but it can be sticky for inflation. Wage growth is hovering around 3.5% to 3.9%. When companies have to pay more for help, they eventually pass that cost to you. It's the "Service Inflation" trap.

The Shelter Lag

Housing is the weirdest part of the math. The way the government tracks rent is notoriously slow. It takes months—sometimes over a year—for real-world rent drops to show up in the official United States inflation rate. Even though new leases are getting cheaper in some cities, the official stats are still catching up to the expensive leases people signed in 2024 and 2025.

What the Experts are Predicting

Nobody has a crystal ball, but some of the biggest names in finance are placing their bets.

- Goldman Sachs: They’re the optimists. They think Core inflation will fall to 2.1% by December 2026.

- Vanguard: A bit more cautious. They see Core inflation peaking over 3% early this year before settling around 2.6%.

- JP Morgan: They expect a "low-grade fever." Higher than the Fed wants, but not a total crisis.

The International Monetary Fund (IMF) also expects the U.S. to end the year around 2.4%.

Basically, the consensus is: "It’ll get better, but slowly."

The Federal Reserve and Your Interest Rates

This is where the rubber meets the road. If inflation is "sticky," the Fed won't lower interest rates.

Right now, the federal funds rate is in the 3.5% to 3.75% range. If you’re looking for a mortgage or a car loan, you’ve noticed those rates are still pretty high.

In December 2025, the Fed gave us a little 25-basis-point cut. But they aren't in a hurry to do it again. Jerome Powell and his team are terrified of cutting too fast and watching the United States inflation rate rocket back up.

🔗 Read more: Why the Yen Canadian Dollar Exchange Rate is Acting So Weird Lately

Most traders expect the Fed to sit on their hands during the January meeting. If the job market stays strong—and it has been, with unemployment around 4.4%—there’s no "emergency" reason for them to lower rates.

How to Protect Your Money Right Now

Waiting for the government to fix things isn't a great strategy. You've got to be a bit more proactive.

Watch the "Shelter" weights

If you're a renter, the fact that the official rate is 3.2% doesn't mean your landlord can't ask for more. However, "real-time" rental data from places like Zillow shows that the market is actually cooling. If your lease is up, use that data to negotiate.

The Cash Trap

With inflation at 2.7% and high-yield savings accounts still offering decent returns, you're actually "winning" slightly by keeping money in the bank. But keep an eye on those rates. As soon as the Fed starts cutting more aggressively, those 4% or 5% savings accounts will disappear.

Smart Substitution

It sounds silly, but the data shows huge gaps between categories. While "Food Away from Home" is up 4.1%, some electronics and used cars are actually getting cheaper. If you were planning a big purchase, 2026 might be the year for a used car rather than a luxury vacation where "service inflation" will eat you alive.

The Bottom Line

The United States inflation rate is currently in a "boring but annoying" phase. We aren't in the middle of the 2022 price explosion, but we also aren't back to the "everything is cheap" days of the 2010s.

Inflation is cumulative. A 2.7% increase this year is stacked on top of the 3.4% from last year and the 6.5% from the year before.

The real question for 2026 is whether the new tariffs and fiscal stimulus will spark a "second wave" of inflation or if the cooling housing market will finally bring us back to that 2% sweet spot.

💡 You might also like: Real porn at work: Why employees risk it and how companies actually respond

Actionable Insights for the Week Ahead:

- Check your HYSA: Ensure your savings account is still paying significantly more than the 2.7% inflation rate. If not, move it.

- Audit your food spend: With a 4.1% hike in restaurant prices, switching even two meals a week to home-cooked can offset the annual inflation "tax" on your budget.

- Lock in debt if you can: If you're looking at a fixed-rate loan, don't necessarily wait for a "crash" in interest rates; the Fed is signaling they will be "higher for longer" throughout most of 2026.