You're sitting at your kitchen table, staring at a stack of medical bills that Medicare didn't quite cover, and honestly, it’s frustrating. You thought you were set. But then the "20% coinsurance" monster rears its head, or maybe you realized your basic plan doesn't touch dental work unless it's a literal emergency. This is exactly where United Healthcare supplemental plans (often branded under the AARP name) come into play. People tend to think of health insurance as a single shield, but it's more like a set of armor pieces—if you’re missing the greaves or the helmet, you’re going to feel the sting eventually.

Insurance is confusing.

Most folks treat "supplemental" as a dirty word or an unnecessary upsell, but let’s be real: Medicare has massive gaps. United Healthcare (UHC) is the biggest player in this space, largely because of their massive partnership with AARP. If you see a Medigap plan with a sunrise logo, that’s them. They aren't just one thing, though. We’re talking about a fragmented ecosystem of Medigap, dental, vision, and "indemnity" plans that pay out cash if you end up in a hospital bed for three days.

The Medigap Reality Check

When we talk about United Healthcare supplemental plans, the conversation usually starts with Medicare Supplement Insurance, also known as Medigap. These plans (labeled A through N) are standardized by the government, which is a weird quirk of the industry. A "Plan G" from United Healthcare has to cover the exact same medical benefits as a "Plan G" from Cigna or Aetna.

So why do people pick UHC?

It’s usually the "perks" and the pricing stability. UHC uses something called "community-rated" or "issue-age-rated" pricing in many states. This is a big deal because some competitors use "attained-age" pricing, which starts cheap but climbs like a mountain as you get older. If you're 65, you might not care. When you're 82 and your premium has tripled, you’ll care a lot.

👉 See also: Does Birth Control Pill Expire? What You Need to Know Before Taking an Old Pack

UHC’s Plan G is the current heavyweight champion. It covers basically everything Medicare Part A and B leave behind except for the Part B deductible. You pay that small amount once a year, and then? Your out-of-pocket costs for covered medical services basically drop to zero. It feels like magic, but you're paying a monthly premium for that peace of mind. Some people prefer Plan N, which is cheaper but makes you pay a $20 copay at the doctor. It's a trade-off. Do you want to pay more every month to never see a bill, or pay less monthly and keep some skin in the game?

It’s Not Just About Medigap

Don't ignore the "ancillary" stuff. United Healthcare offers supplemental coverage that isn't tied to Medicare at all—things like the Hospital Indemnity or Critical Illness plans.

Imagine you’re diagnosed with a serious condition. Even with great insurance, you’re missing work. You’ve got gas money for trips to the specialist. You’ve got specialized diet needs. A critical illness plan from UHC just cuts you a check. It’s "supplemental" in the sense that it supplements your life, not just your doctor’s bill.

Then there’s the dental and vision side. Medicare famously ignores your teeth and eyes unless there’s a disease involved (like glaucoma). UHC’s supplemental dental plans are some of the most widely accepted in the country because they use the DentalProvider network. If you've ever tried to find a dentist who takes "discount cards," you know how miserable that is. Having an actual UHC PPO plan is a different league entirely.

Common Misconceptions About the AARP Connection

- You don't have to be "retired" to get an AARP-branded UHC plan, but you usually need to be 50+ for membership.

- The plans aren't run by AARP. AARP just puts their stamp of approval on it and collects a royalty; United Healthcare is the one processing your claims and managing the network.

- Pricing isn't always the lowest. While UHC is often competitive, they occasionally get beat on price by smaller, regional carriers. You're paying for the "big brand" stability.

The "Network" Myth in Supplemental Insurance

Here is a nuance most people miss: if you buy a United Healthcare supplemental plan that is a true Medigap policy, there is NO NETWORK.

✨ Don't miss: X Ray on Hand: What Your Doctor is Actually Looking For

I’ll say it again because it’s the most misunderstood part of the industry. If a doctor accepts Medicare, they HAVE to accept your UHC Medicare Supplement plan. It doesn't matter if they "take United Healthcare" or not. If they take the red, white, and blue Medicare card, the supplemental plan just follows along and pays its share automatically. This is why people who travel in RVs or spend winters in Florida love these plans. You aren't trapped in a local HMO cage.

However, if you choose a Medicare Advantage plan (Part C) from United Healthcare, that is NOT a supplemental plan. People confuse these constantly. Advantage plans replace your original Medicare and put you in a network. Supplemental plans (Medigap) sit on top of original Medicare. It’s an expensive distinction if you get it wrong.

When Does a Supplemental Plan Actually Make Sense?

Basically, if you have a lot of doctor visits, or if the idea of an unexpected $5,000 hospital bill makes you lose sleep, the supplement is worth it.

Think about it this way: Medicare Part B covers 80%. That 20% you're left with has no "cap." If you have a $100,000 heart surgery, 20% is $20,000. That’s a lot of money to find in a couch cushion. The United Healthcare supplemental plans act as a ceiling. They stop the bleeding.

There are also niche products like "Accident Expense" insurance. These are popular with younger families or active seniors. If you trip, break an arm, and end up in the ER, the plan pays out a fixed amount. It’s simple. It’s transactional. It’s honestly sorta refreshing compared to the labyrinth of standard health insurance.

🔗 Read more: Does Ginger Ale Help With Upset Stomach? Why Your Soda Habit Might Be Making Things Worse

Specific Details: The Renewability Factor

One thing UHC does well is "Guaranteed Renewability." As long as you pay your premiums, they cannot kick you off the plan because you got sick. You could develop a chronic condition the day after you sign up, and they are legally bound to keep covering you.

This is why the "Initial Enrollment Period" is so critical. When you first turn 65 and sign up for Medicare Part B, you have a six-month window where United Healthcare must accept you for any Medigap plan they offer, regardless of your health. No medical underwriting. No questions about your blood pressure or that "thing" with your knee. If you miss that window and try to buy a supplemental plan later, you might have to answer health questions, and they can—and will—deny you if you're too high-risk.

How to Actually Choose One Without Losing Your Mind

- Check your meds first. Supplemental plans (Medigap) do not cover prescription drugs. You’ll need a separate Part D plan for that. UHC has several, like the "Walgreens" specific plans that can save you a bundle if you use that pharmacy.

- Look at the "Household Discount." UHC is famous for this. If you live with someone else who is also on a UHC supplemental plan (or sometimes just someone over 18, depending on the state), you can get a percentage off your premium. It’s usually around 5% to 10%, which adds up over a decade.

- Evaluate the "Renew Active" program. This is UHC’s version of SilverSneakers. It’s a free gym membership. If you’re already paying $40 a month for a gym, and the supplemental plan gives it to you for free, you have to factor that $40 "savings" into the cost of the insurance.

- Ignore the "Introductory" rates. Some companies lure you in with a "New to Medicare" discount that disappears after 12 months. UHC does this too, but they are usually more transparent about how the rate will step up in year two.

The Limitations Nobody Mentions

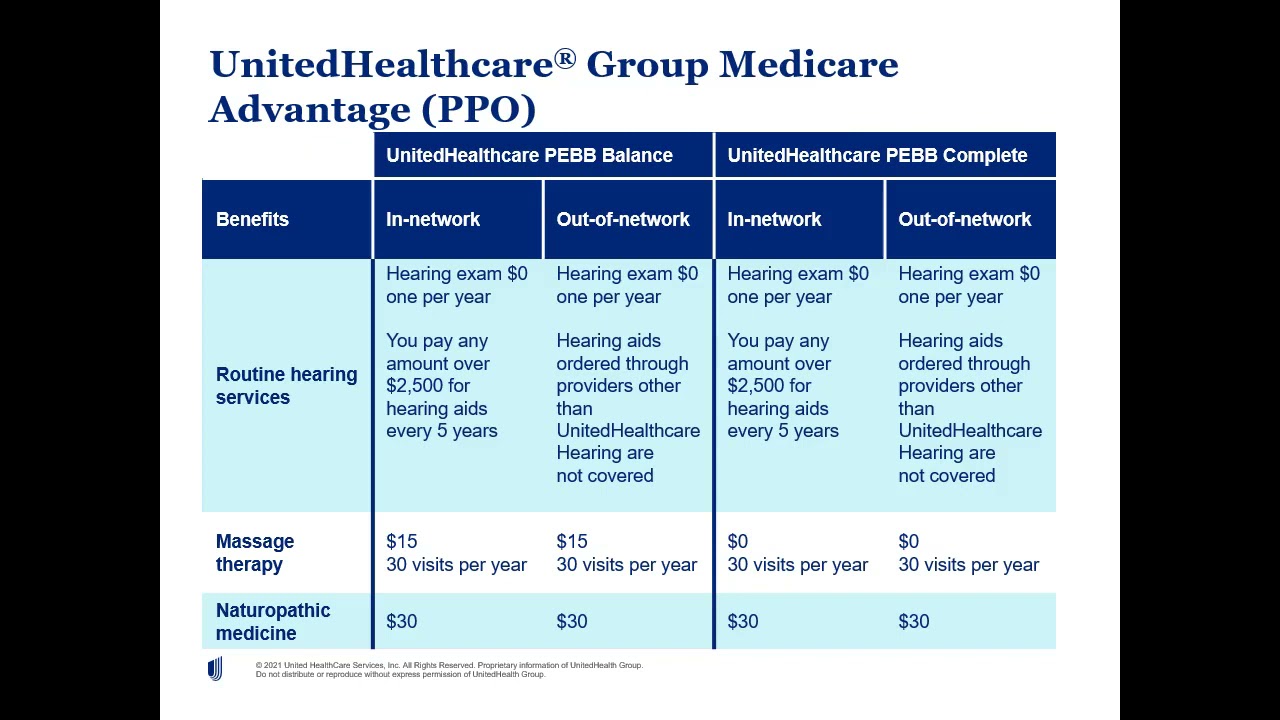

It’s not all sunshine. United Healthcare supplemental plans aren't a "get out of jail free" card for every cost. They don't cover long-term care (nursing homes). They don't cover private-duty nursing. They don't cover hearing aids in the standard Medigap versions—you usually have to buy a separate rider or a specific "ancillary" plan for that.

And let's talk about the paperwork. While UHC is generally efficient, their size can be a double-edged sword. If you have a billing dispute, you are dealing with a massive bureaucracy. You aren't calling a small office down the street; you're calling a call center that might be halfway across the globe. Most of the time, the "crossover" system works—where Medicare pays their part and then electronically tells UHC to pay theirs—but when it breaks, it takes some patience to fix.

Actionable Next Steps

If you're ready to stop guessing, here is exactly what you should do:

- Pull your last 12 months of medical bills. Add up what you paid out of pocket. If that number is higher than the annual premium of a Plan G (usually $1,500–$2,400 depending on your area), the supplement is a mathematical win.

- Verify your "Initial Enrollment" date. If you are within 6 months of your Part B effective date, you are in the "Golden Window." Buy the best plan you can afford now, because you might not be able to get it later.

- Check the Dental network. If you're eyeing a UHC dental supplement, go to their provider search tool and plug in your zip code. If your favorite dentist isn't on there, the plan loses 80% of its value immediately.

- Compare the "Total Cost of Ownership." Don't just look at the monthly premium. Look at the gym benefits, the household discount, and the reputation for rate stability in your specific state. State insurance departments often publish "rate increase histories" for companies—look for UHC's history in your state to see if they've been hiking prices aggressively or keeping them steady.

Ultimately, picking a plan isn't about finding the "best" company, because "best" is subjective. It’s about finding the plan that makes your healthcare costs predictable. For most, United Healthcare offers that predictability through sheer scale. Just make sure you aren't buying more than you need, and definitely don't wait until you're sick to try and get the "good" coverage. By then, the window might already be closed.