You're sitting there looking at a premium quote and wondering if you’re being ripped off. It’s a common feeling. Honestly, trying to pin down a typical health insurance cost is like trying to nail Jell-O to a wall because the "average" doesn't really exist for you. It only exists for actuaries.

The math is messy.

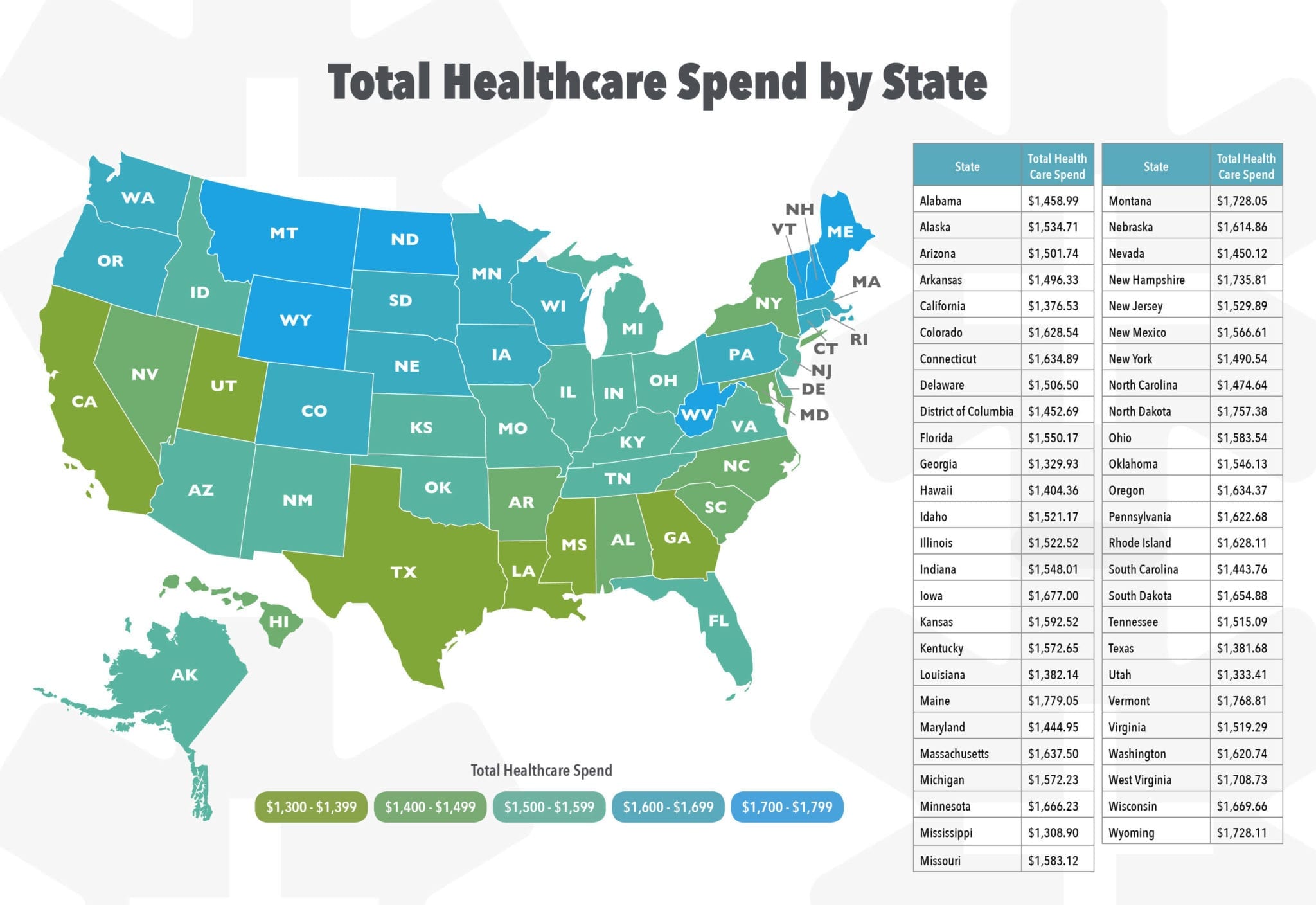

Most people think they’re just paying for doctor visits. You aren't. You’re paying for the collective risk of every person in your "rating area," a geographic zone determined by your state. If you live in a county where everyone seems to have a chronic back issue or where the local hospital charges $5,000 for a simple MRI, your "typical" cost is going to skyrocket compared to someone three towns over.

✨ Don't miss: Sex in the Nose: Why We Get So Confused About Nasal Sex Biology

According to the KFF (Kaiser Family Foundation) 2024 Employer Health Benefits Survey, the average annual premium for employer-sponsored family coverage hit $25,572. That is a staggering number. But here’s the kicker: most employees don't feel that full weight because their boss covers about 73% of it. If you’re a freelancer or a small business owner buying on the ACA Marketplace, that $2,100 a month comes straight out of your pocket unless you qualify for subsidies. It's a massive wealth transfer that happens every single month, often without us noticing the nuance of where that money actually goes.

Why the "Average" Price is Basically a Lie

We talk about averages to feel comfortable, but health insurance is hyper-individualized. Age is the big one. Under the Affordable Care Act, insurers can charge older adults up to three times more than younger ones. This is called the "age rating ratio."

If you’re 24, your typical health insurance cost might be $300 a month for a Silver plan. If you’re 62, that same plan—with the exact same doctors and the exact same deductible—could easily cost you $1,100. It’s the same product. The only difference is your birth certificate.

Then there’s the "Metal Tier" trap.

People see a Bronze plan with a $350 premium and think they’ve found a bargain. They haven't. They’ve just deferred their payments. A Bronze plan usually covers about 60% of healthcare costs, leaving you to foot the bill for the other 40% until you hit a massive deductible, often exceeding $7,000 for an individual. On the flip side, a Gold plan might cost $700 a month but covers 80%. If you have a chronic condition like Type 1 diabetes or Crohn's disease, the "expensive" Gold plan is actually the cheapest way to live.

The Subsidy Shield

We can't talk about cost without talking about the Advanced Premium Tax Credits (APTC). Since the Inflation Reduction Act was extended, more people than ever qualify for these.

If your income is between 100% and 400% of the Federal Poverty Level, the government basically sends a check to the insurance company on your behalf. For many, this drops the "sticker price" of $500 down to $50 or even $0. But if you earn just one dollar over the cliff—though the "subsidy cliff" was temporarily removed—you might find yourself paying the full freight. It’s a binary experience. You’re either protected by the government or you’re out in the cold, facing the raw market rates.

Geography: The Silent Cost Driver

Where you sleep matters more than what you eat when it comes to premiums.

📖 Related: Is 38.2 C a Fever? Converting 38.2 C to Fahrenheit and What to Do Next

In 2024, states like West Virginia and New York saw some of the highest average premiums in the country. Why? Lack of competition. If only one or two insurers are willing to cover a rural county, they have zero incentive to lower prices. Conversely, in a place like Florida or Texas, the sheer volume of providers keeps the typical health insurance cost slightly more anchored, though "cheap" is still a relative term.

- Network Size: Narrow networks (HMOs) are cheaper but restrict you to specific buildings.

- PPOs: These give you freedom but come with a 20-30% premium surcharge.

- Point of Service (POS): A weird middle ground that most people find confusing and frustrating.

There is also the "Provider Consolidation" effect. When a massive hospital system buys up all the small primary care practices in a city, they gain immense leverage. They tell the insurance companies, "Pay us 20% more, or we’re leaving your network." The insurer pays, and then they pass that cost directly to you in next year's premium hike. You’re paying for a corporate merger you never asked for.

The Hidden Costs: Deductibles and Out-of-Pocket Maximums

If you only look at the monthly premium, you're doing it wrong. You have to look at the "Total Cost of Ownership."

Let’s say you choose a plan with a $400 premium and an $8,000 deductible.

Your guaranteed annual cost is $4,800 (premiums).

Your potential annual cost is $12,800.

Most Americans can't cover a $400 emergency expense, yet the "typical" individual deductible for a Bronze plan is now well over $6,000. It’s insurance for catastrophes, not for health. It’s basically "bankruptcy insurance." You pay every month so that if you get hit by a bus, you only lose $8,000 instead of $200,000.

Real World Example: The "Typical" Family of Four

Imagine a family in suburban Ohio. Parents are 40, two kids under 14.

Without subsidies, a mid-level Silver plan might run them $1,500 a month.

That’s $18,000 a year just to have the card in their wallet.

If one kid breaks an arm and the dad needs a minor gallbladder surgery, they might hit their $10,000 family deductible.

Total cost for the year: $28,000.

That is more than many people spend on their mortgage. This is the reality of the American healthcare landscape that "average" statistics often gloss over.

Tobacco Use and the 50% Surcharge

One of the few personal choices that still impacts your typical health insurance cost is smoking. Under the ACA, insurers can charge smokers up to 50% more through a "tobacco surcharge."

Interestingly, the subsidies don't cover this surcharge. If your plan costs $500 and you get a $450 subsidy, you pay $50. But if you’re a smoker and the insurer adds a 50% surcharge ($250), your subsidy stays at $450. Your monthly bill jumps from $50 to $300. It is a massive financial penalty that hits lower-income individuals the hardest.

Prescription Drug Tiers

Don't ignore the formulary.

You might find a plan that saves you $100 a month in premiums, but if it moves your brand-name medication to "Tier 4" or "Specialty," you could end up paying a 40% coinsurance instead of a $40 copay. One month of a specialty drug like Humira can cost $7,000. If your plan has a high coinsurance for specialty drugs, you’ll hit your out-of-pocket maximum in January. In that specific case, the "expensive" plan with the $0 drug copay is actually the only logical choice.

How to Actually Lower Your Costs

Stop looking for the cheapest premium. It’s a trap.

Instead, do a "utilization audit" of your last 12 months. How many times did you actually go to the doctor? If the answer is "once for a physical," then a High Deductible Health Plan (HDHP) paired with a Health Savings Account (HSA) is your best friend. The money you save on premiums goes into the HSA tax-free, stays yours forever, and can be invested.

If you go to the doctor every month, the HDHP is a disaster. You need a PPO or a Gold-tier HMO.

Also, check for "Off-Exchange" plans. Sometimes, insurers sell plans directly on their websites that aren't listed on Healthcare.gov. These don't qualify for subsidies, so if you're a high earner, you might find a better provider network for the same price by going direct.

Actionable Steps for Your Next Enrollment

Don't just auto-renew. Insurers change their formularies and doctor networks every single year. Your doctor might have been "In-Network" in 2024 but dropped the contract for 2025.

- Verify your doctors every year. Call the office directly; don't trust the insurer's website, which is often outdated.

- Run the "Max Cost" calculation. Add (Monthly Premium x 12) + Out-of-Pocket Maximum. This is your "worst-case scenario" number. Compare this number across three different plans.

- Check for HSA eligibility. If you're healthy, the tax advantages of an HSA often outweigh the benefits of a lower deductible.

- Look at the Summary of Benefits and Coverage (SBC). It’s a standardized document every plan must provide. Skip the marketing fluff and go straight to the "Examples" page at the end, which shows exactly what you’d pay for a pregnancy or a broken foot.

The typical health insurance cost is a baseline, but your actual cost is a choice based on how much risk you’re willing to carry. You can pay the insurance company to take the risk (high premium), or you can keep the risk yourself (high deductible). Just make sure you have the savings to back up that second choice.

Next Steps:

Review your last three months of healthcare spending, including pharmacy receipts. Use that data to run a "Max Cost" comparison against your current plan's renewal notice. If your total potential cost has increased by more than 10%, it is time to shop the marketplace for a different metal tier.