Let’s be honest. When you see a clock ticking up toward $36 trillion, your brain kinda just shuts off. It’s too big. Most of us can’t even visualize what a billion dollars looks like, let alone thirty-six thousand of them. But here we are. The total US national debt is sitting at levels that would have seemed like science fiction just two decades ago. Back in 2000, the debt was roughly $5.6 trillion. Now? We add that much to the tab every few years. It’s wild.

It’s easy to get caught up in the doom-scrolling and the "we’re all going broke" headlines. But the reality is actually more nuanced and, frankly, a bit more interesting than just a scary number on a screen.

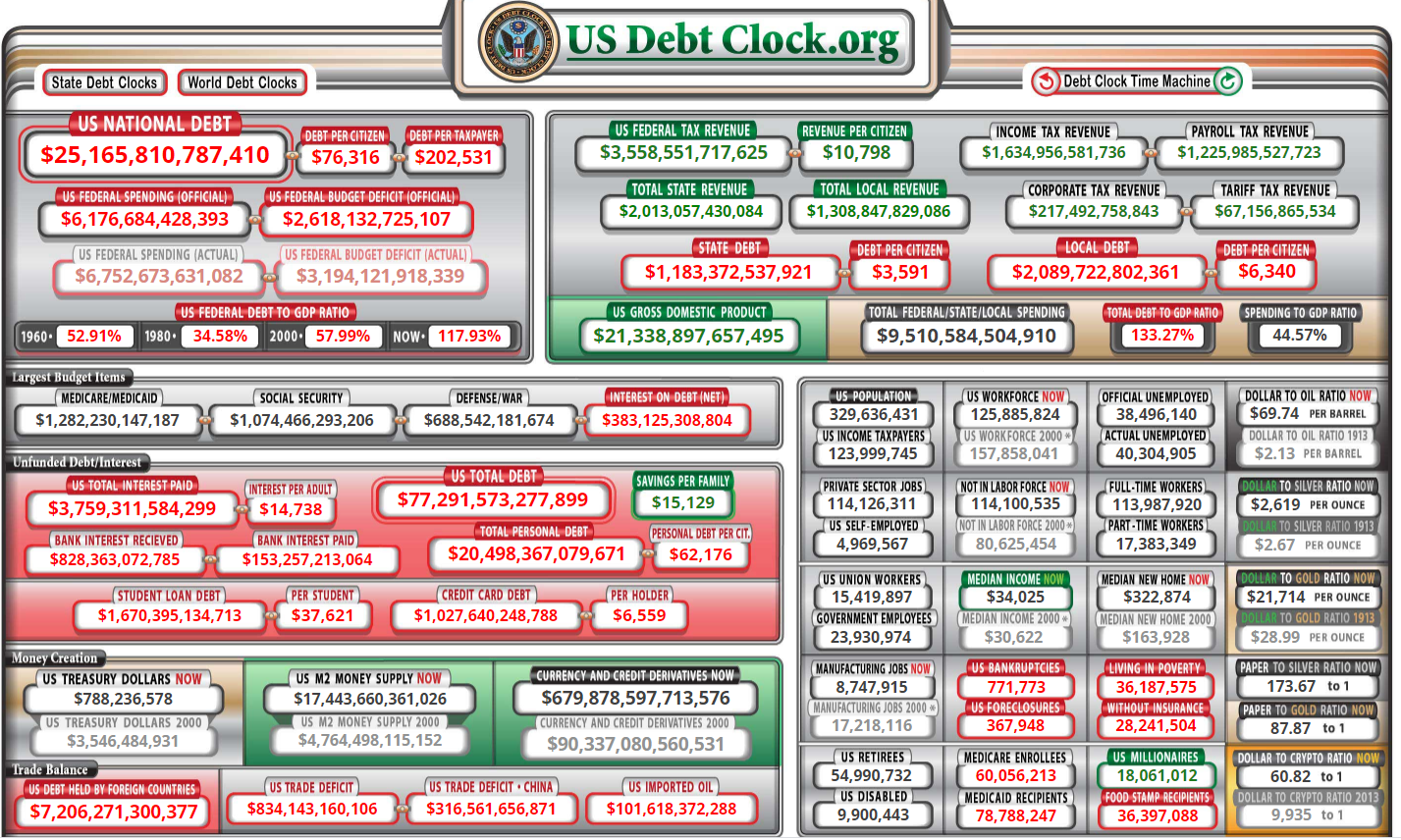

What the Total US National Debt Actually Is (And Who We Really Owe)

Most people think of debt like a credit card bill. You buy a TV, you owe the bank, you pay it back or they take your house. The federal government doesn’t work like that. Basically, the debt is the accumulation of every yearly deficit the US has run since the founding of the country. When the government spends more than it takes in via taxes—which happens almost every year—it issues Treasury securities. These are essentially "I owe yous" sold to investors.

The interesting part is who holds the receipts. It’s not just "China," which is a common myth people love to shout about during election years. As of late 2025, foreign holders only account for about a quarter of the debt. A massive chunk of the total US national debt is actually held by us. Well, not you and me personally (unless you have some T-bills in your brokerage account), but by domestic entities like the Federal Reserve, pension funds, and even the Social Security Trust Fund.

It’s a bit of a loop. The government borrows money from its own future obligations to pay for today’s stuff.

The Debt Held by the Public vs. Intragovernmental Holdings

When you look at the Treasury’s data, you’ll see two main categories. There is "Debt Held by the Public" and "Intragovernmental Holdings." The public part is what most economists worry about because that’s the money we actually have to compete for in the open market. It’s held by individuals, corporations, and foreign governments.

The intragovernmental part is basically the government borrowing from itself. For example, Social Security takes in more in payroll taxes than it pays out in benefits (or it used to, things are getting tighter now), so it takes that extra cash and buys Treasuries. The government then spends that cash on other things, like roads or defense. It’s like taking money out of your savings account to pay your electric bill and leaving a sticky note saying "I'll pay you back."

💡 You might also like: Jersey City Shooting Today: What Really Happened on the Ground

Why Did It Get This Big?

It didn’t happen overnight, but it definitely sped up. If you look at the trajectory, there are a few "hockey stick" moments where the line just shoots upward.

- The 2008 Financial Crisis: The Great Recession required massive bailouts and stimulus.

- The 2017 Tax Cuts: The Tax Cuts and Jobs Act significantly reduced revenue.

- COVID-19: This was the big one. Trillions in emergency spending to keep the economy from cratering.

Honestly, it’s a bipartisan effort. Neither side of the aisle has a great track record here. One side likes to cut taxes without cutting spending; the other likes to increase spending without increasing taxes enough to cover it. The result is a total US national debt that grows regardless of who is in the White House.

According to the Congressional Budget Office (CBO), the primary drivers moving forward aren’t even the "discretionary" stuff like foreign aid or NASA. It’s the "big three": Medicare, Social Security, and the interest on the debt itself.

The Interest Trap

This is the part that keeps economists like Maya MacGuineas, president of the Committee for a Responsible Federal Budget, up at night. For a long time, interest rates were basically zero. Borrowing was cheap. If you have a million-dollar mortgage but your interest rate is 0.5%, you’re fine. But if that rate jumps to 5%, you’re in trouble.

The US is feeling that right now. As the Federal Reserve raised rates to fight inflation over the last few years, the cost of servicing the total US national debt skyrocketed. We are now spending more on interest payments alone than we do on the entire Department of Defense budget. Just let that sink in. We are paying over $1 trillion a year just to exist in our current state of debt, without even touching the principal.

Is the US Going Bankrupt?

Probably not in the way you’re thinking. A country that prints its own currency can’t "run out" of money the way a household does. They can always print more to pay the debt. The problem isn't running out of cash; it's the value of that cash.

📖 Related: Jeff Pike Bandidos MC: What Really Happened to the Texas Biker Boss

If we print too much to pay off the debt, we get hyperinflation. Your $20 bill might only buy a loaf of bread. This is the "hidden tax" of debt. Even if the government doesn't raise your taxes, the debt can eat your savings through the loss of purchasing power.

There’s also the "crowding out" effect. When the government borrows so much money, it leaves less for everyone else. Businesses might find it harder to get loans, or interest rates for mortgages might stay higher for longer because the government is hogging all the available credit. It slows down innovation. It makes the whole economy feel... sluggish.

The Debt-to-GDP Ratio

Economists often look at the Debt-to-GDP ratio rather than the raw number. It’s like comparing a $50,000 car loan for someone making $20,000 a year versus someone making $500,000. Right now, our debt is over 120% of our annual GDP. That means we owe more than the value of every single thing produced in the US in a year.

Historically, once a country passes the 90% or 100% mark, economic growth starts to stall. We’ve been living above that for a while now. Some say we’re in uncharted territory. Others, like proponents of Modern Monetary Theory (MMT), argue that as long as we don't have runaway inflation, the total amount doesn't actually matter. It’s a huge debate with no clear consensus.

Common Misconceptions About the Debt

People love to simplify this, but it’s messy.

- "We should just run the government like a business." Businesses actually love debt. Most major corporations carry massive amounts of it to fund expansion. The difference is they use it to generate a return. The debate is whether the US is using its debt for "growth" (like infrastructure) or just "consumption" (like daily operations).

- "China owns us." As mentioned, they own a lot, but they’ve actually been selling off their Treasuries lately. Japan is currently the largest foreign holder. And even then, they can't just "call in" the debt. These are bonds with set maturity dates. They can sell them to someone else, but they can't demand the US pay up tomorrow.

- "Cutting foreign aid will fix it." Foreign aid is less than 1% of the federal budget. You could eliminate it entirely and it wouldn't even be a rounding error on the total US national debt.

What Actually Happens Next?

There’s no "easy button" here. Fixing the debt requires some combination of three things that everyone hates:

👉 See also: January 6th Explained: Why This Date Still Defines American Politics

- Cutting Spending: This means touching Social Security or Medicare, which is political suicide.

- Raising Taxes: This is unpopular for obvious reasons and can slow down the economy if done poorly.

- Growth: If the economy grows faster than the debt, the problem gets smaller relatively. But it’s hard to grow your way out of $36 trillion.

Most likely, we’ll see a "muddle through" approach. Small tweaks to the tax code, maybe raising the retirement age slightly over the next 30 years, and hoping for a technological boom (like AI) that drives massive GDP growth.

Actionable Steps for the Average Person

You can’t control the total US national debt, but you can control how it affects your life. The reality of a high-debt environment is that the future is likely to be "expensive."

Diversify your assets. If the dollar loses value due to debt-fueled inflation, you don't want all your eggs in one basket. Real estate, stocks, and even international investments can act as a hedge.

Watch interest rates. High national debt usually means higher-for-longer interest rates. If you’re planning on buying a home or taking out a large loan, don’t wait for "1990s rates" to come back. They might not.

Stay informed but don't panic. The US has had debt since its inception. While the current levels are unprecedented, the US still has the world's reserve currency and the most powerful military. That gives the government a lot of leverage that a normal person (or even another country) doesn't have.

Vote on fiscal policy. If the debt matters to you, look at the actual CBO scores of the policies being proposed by candidates. Ignore the rhetoric and look at the math. Most "plans" to fix the debt actually end up adding to it when you crunch the numbers.

The total US national debt is a massive, looming shadow over the economy, but it’s also a reflection of our collective choices over the last 50 years. Understanding it won't pay it off, but it will help you navigate the financial reality it creates.

Practical Next Steps:

- Review your retirement accounts to ensure you have an inflation hedge, such as TIPS (Treasury Inflation-Protected Securities) or diversified equities.

- Check the TreasuryDirect website if you want to see the "Debt to the Penny" live updates—it's eye-opening.

- Evaluate any variable-rate debt you hold (like credit cards) and prioritize paying them off, as high national debt service costs often correlate with higher consumer interest rates.