You’ve probably heard that bonds are the "boring" part of a portfolio. They’re supposed to be the ballast, the steady hand that keeps your investments from sinking when the stock market decides to have a mid-life crisis. But if you’ve looked at a total bond market index lately, things might feel a bit... off.

It isn't just you.

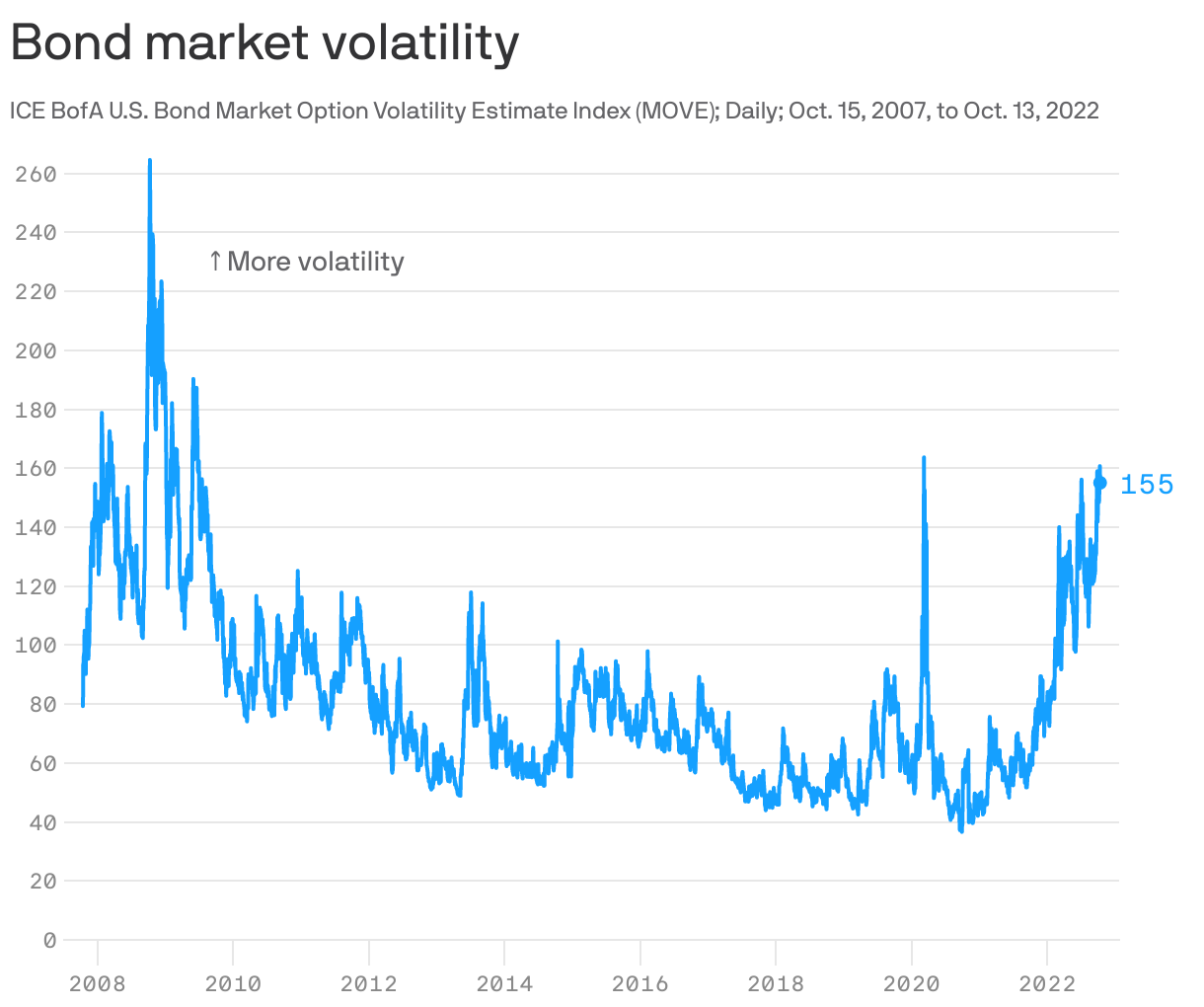

Bond markets have been through a literal buzzsaw over the last few years. We spent a decade where interest rates were basically zero, making bonds feel like a savings account that didn't pay anything. Then, inflation hit. The Federal Reserve started hiking rates like they were trying to win a marathon, and suddenly, those "safe" bond indexes saw drops that looked suspiciously like a tech stock crash. If you own an aggregate bond fund—think BND or AGG—you’ve likely seen some red.

It's weird. It’s frustrating. But honestly, it’s also the most interesting the bond market has been in twenty years.

What a Total Bond Market Index Actually Is (And What It Isn’t)

Most people assume "total" means everything. It doesn't.

When you buy a fund that tracks something like the Bloomberg US Aggregate Bond Index (the "Agg"), you aren't buying every single IOU in the world. You’re mostly buying two things: US Treasuries and mortgage-backed securities (MBS). There’s a sprinkling of investment-grade corporate debt in there too, but it’s heavily weighted toward the government.

Think of it as a giant bucket of high-quality debt.

Because the index is market-cap weighted, the biggest debtors get the most space. Since the US government is the biggest borrower on the planet, Treasuries dominate the landscape. This is why the total bond market index is often seen as a proxy for the health of the US economy and the direction of interest rates.

But here’s the kicker: it leaves out the spicy stuff. You won't find high-yield "junk" bonds here. You won't find international debt or inflation-protected securities (TIPS) in most standard total bond indexes. It’s the vanilla ice cream of the investing world. Reliable? Usually. Exciting? Rarely.

The Duration Trap

There is a concept called duration. You need to understand it if you want to keep your sanity while looking at your brokerage account. Duration isn't just the time until a bond pays you back; it’s a measure of how much the price will move when interest rates change.

If a total bond market index has a duration of 6 years, and interest rates go up by 1%, the value of that index will likely drop by about 6%.

For a long time, this didn't matter because rates only went down or stayed flat. But when the Fed started cranking rates up to fight the post-pandemic inflation surge, duration became a predator. Investors who thought they were in a "risk-free" asset suddenly realized that while the credit risk was low (the government will probably pay you back), the interest rate risk was massive.

The Vanguard Influence and the Bloomberg Agg

John Bogle, the legendary founder of Vanguard, basically changed the game when he launched the first retail bond index fund. Before that, if you wanted bonds, you had to pick them individually or pay a massive fee to a mutual fund manager who probably wouldn't beat the market anyway.

The Vanguard Total Bond Market Index Fund (VBTLX or BND) is the 800-pound gorilla in the room. It tracks the Bloomberg US Agg.

📖 Related: PDI Stock Price Today: What Most People Get Wrong About This 14% Yield

Why does this matter? Because trillions of dollars follow this specific recipe. When the index rebalances, the whole market feels it. It creates a weird feedback loop where the most indebted entities—the ones issuing the most bonds—become the biggest holdings in everyone's "safe" portfolio.

Some critics, like those at DoubleLine Capital or PIMCO, often argue that this is a flawed way to invest. They’ll tell you that weighting by debt is the opposite of how you should pick stocks. In stocks, you want the winners. In a bond index, you're technically giving the most money to the people who owe the most.

It’s a fair point. But for the average person, the low cost of these index funds—often with expense ratios as low as 0.03%—usually outweighs the structural weirdness.

Why the "Total" Market Felt Like a Total Mess

If you bought a total bond market index fund in early 2021, you might be feeling a bit burned. 2022 was actually the worst year for the US bond market in history. Literally. Ever.

The Bloomberg Agg dropped about 13%.

For a "safe" asset, that is a punch to the gut. The reason was a "perfect storm" of low starting yields and aggressive rate hikes. When you start with a yield of 1%, there isn't much of a cushion to soak up price drops.

But there’s a silver lining.

Bonds are math. Eventually, the math works in your favor. As old bonds in the index mature, the fund managers buy new ones that pay the current, higher interest rates. Slowly but surely, the "yield to maturity" of the index creeps up.

Today, the total bond market index is actually paying a decent income again. We’ve moved away from the "TINA" (There Is No Alternative) era where everyone had to buy stocks because bonds paid nothing. Now, you can actually get a 4% or 5% yield on high-quality debt. That’s a massive shift in the financial landscape.

A Quick Reality Check on Diversification

Does the 60/40 portfolio still work?

For years, the 60% stocks and 40% bonds split was the gold standard. In 2022, both crashed at the same time. People declared the 60/40 dead.

They were probably wrong.

Historically, bonds and stocks move in opposite directions most of the time. 2022 was an outlier because inflation was the primary driver of everything. When inflation is the problem, both stocks and bonds hate it. But in a normal recession—where growth slows down—the total bond market index usually does exactly what it's supposed to do: it goes up while stocks go down.

👉 See also: Getting a Mortgage on a 300k Home Without Overpaying

Comparing the Big Players: BND vs. AGG

If you’re looking to get into a total bond market index, you’re likely looking at two main ETFs: Vanguard’s BND and BlackRock’s AGG.

Honestly? They’re almost identical.

They both track the same index. They both have rock-bottom fees. If you look at a chart of their performance over five years, the lines overlap so perfectly you can’t tell them apart.

However, some people prefer BND because it includes some "sampling" techniques that Vanguard uses to try and slightly optimize the holdings without straying from the index. Others like AGG because it’s slightly more liquid for huge institutional traders. For you? It probably doesn't matter. Flip a coin. Or just pick the one that your brokerage lets you buy commission-free.

What Nobody Tells You About the Index Composition

The "Agg" is heavily tilted toward the housing market.

Roughly 25% to 30% of a total bond market index is comprised of Mortgage-Backed Securities (MBS). These are pools of home loans guaranteed by entities like Fannie Mae and Freddie Mac.

This introduces a weird risk called "prepayment risk."

When interest rates drop, people refinance their homes. They pay off their old high-interest loans, and the bondholders (you) get your money back sooner than you wanted. Then you have to reinvest that money at the new, lower rates.

Conversely, when rates go up, nobody refinances. The "duration" of the index actually extends because those mortgages are going to stay on the books for the full 30 years. This means your bond fund becomes more sensitive to interest rates exactly when you don't want it to be.

It’s a quirk of the US housing market that isn't present in many other countries’ bond indexes. It makes the US total bond market a very specific beast.

Real Talk: Is it Time to Buy?

Market timing is a loser's game, but let's look at the facts.

Real yields—which is the yield you get after subtracting inflation—are positive again. For a long time, they were negative. That meant you were guaranteed to lose purchasing power by holding bonds.

Now, the total bond market index offers a legitimate "real" return.

✨ Don't miss: Class A Berkshire Hathaway Stock Price: Why $740,000 Is Only Half the Story

If you think the Fed is done hiking or might even cut rates in the next 12 to 18 months, buying a total bond index now is basically locking in these higher yields. If rates fall, the price of your bond fund will go up. You get the "capital appreciation" on top of the monthly dividend.

But if inflation stays sticky and rates have to go even higher? You could see more price erosion.

The difference now is that the "yield cushion" is much thicker. A 4.5% yield can absorb a lot more price volatility than a 1% yield could back in 2021.

How to Actually Use This in Your Portfolio

Don't just dump everything into a bond index because "experts" say you should. Think about what you're actually trying to achieve.

- For Retirement Steadiest: Use a total bond index as your core holding. It covers the bases. It’s cheap. It’s easy.

- For Short-Term Needs: If you need the money in two years for a house down payment, a total bond index might actually be too risky. Remember that 6-year duration? A two-year window is too short to recover if rates spike again. Stick to a Money Market fund or a short-term Treasury ETF.

- For Taxable Accounts: Be careful. Bond interest is taxed as ordinary income. If you're in a high tax bracket, the "total bond market" might be less attractive than municipal bonds, which are often tax-free at the federal level.

The total bond market index is a tool. It's not a magic shield.

Actionable Steps for Your Bond Strategy

If you're looking at your portfolio and wondering what to do with that sea of bond fund red, here is the move.

First, check your expense ratio. If you are in a legacy mutual fund charging 0.50% or more for a "total bond" strategy, you're getting robbed. Switch to a low-cost ETF like BND or AGG immediately. In the bond world, fees are one of the few things you can actually control.

Second, match your duration to your timeline. If you aren't retiring for 10 years, the current volatility in the total bond market doesn't matter. In fact, it's good for you because your fund is reinvesting dividends at higher rates. If you need the money soon, trim your total bond index and move it into a "short-term" bond fund (duration of 1-3 years).

Third, don't ignore the "barbell" strategy. Some investors are splitting their bond holdings. They put half in very short-term T-bills (which pay high rates right now) and half in long-term bonds. This gives you high immediate income and a "hedge" if the economy crashes and long-term rates plummet.

Ultimately, the total bond market index remains the most efficient way to capture the "middle" of the debt market. It’s had a rough ride, but the fundamental math of bonds hasn't changed. They pay you to wait. And for the first time in a long time, that payment is actually worth something.

Keep an eye on the Fed, but don't obsess over every headline. The bond market is a slow-motion game. Play it that way.

The most important thing to remember is that bonds are a contract. Unless the US government and every major corporation in America goes bust simultaneously, those checks are going to keep clearing. In a world of volatile crypto and "to the moon" stocks, there's something deeply comforting about a boring old contract.

---