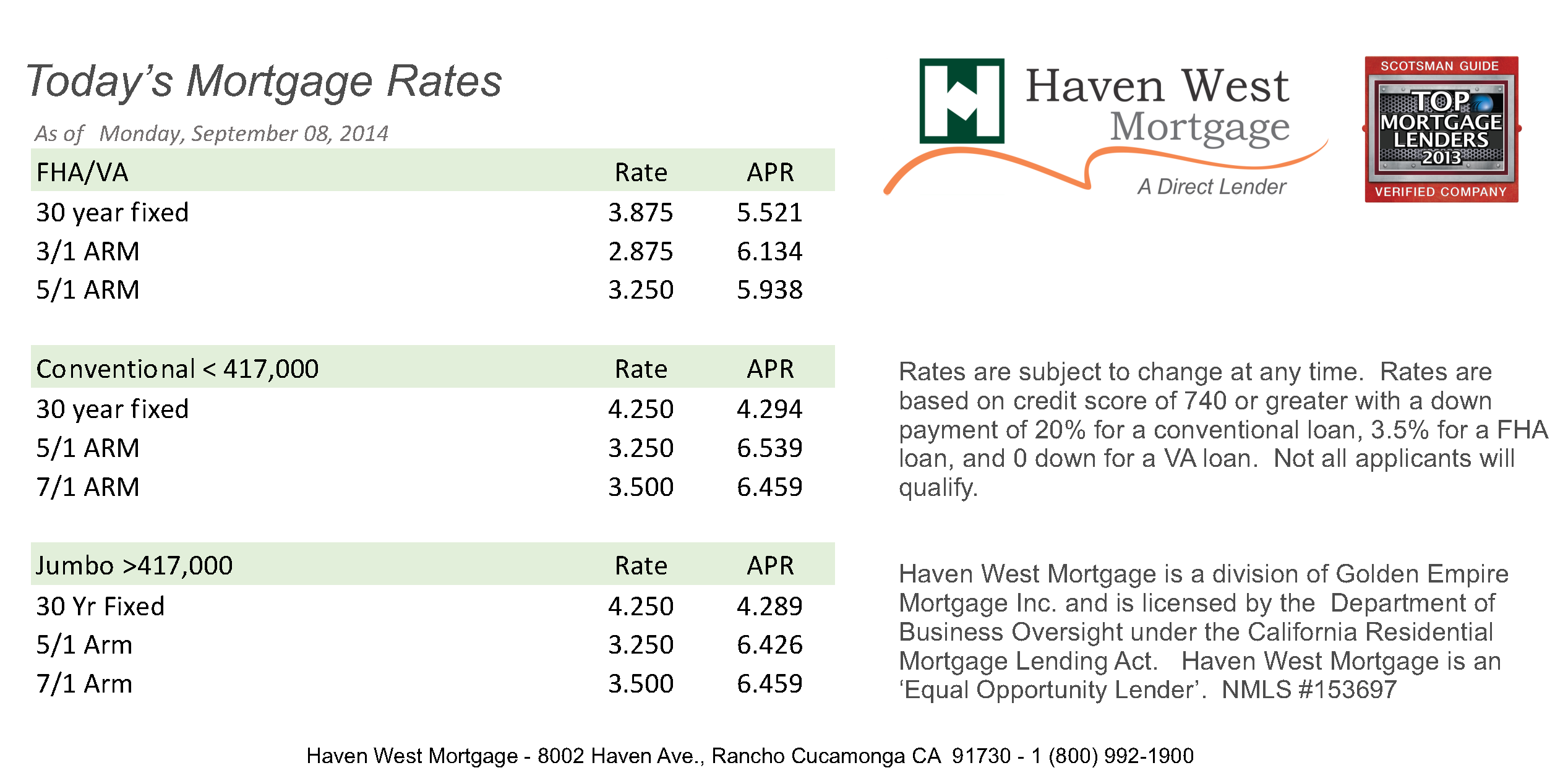

Honestly, the housing market has felt like a giant staring contest for the last two years. Buyers have been waiting for rates to cave, while the Federal Reserve has been waiting for inflation to stay dead and buried. Well, someone finally blinked. As of today, January 16, 2026, we’re seeing a shift that actually matters for your wallet.

The average 30-year fixed mortgage rate is sitting at 6.11% today.

💡 You might also like: Norwegian Krone to Canadian Dollar: What Most People Get Wrong About This Oil-Driven Pair

That might not sound like a miracle if you're still dreaming of those 3% pandemic unicorns. But compare it to this time last year when we were scraping 7.04%. It’s a massive psychological relief. For a $400,000 loan, that drop is the difference of nearly $250 a month. That's a car payment. Or, you know, a lot of groceries in 2026.

What’s Happening With Today Current Mortgage Rates?

The numbers aren't just drifting; they're reacting to some pretty specific moves in Washington. Just yesterday, January 15, Freddie Mac reported the weekly average for 30-year fixed loans hit 6.06%. It’s the lowest we've seen since late 2022.

If you're looking at a 15-year fixed mortgage, things look even better at 5.38%.

Here is a quick look at where the "street" averages are landing right now across different loan types:

- 30-Year Fixed: 6.11% (Purchase) / 6.58% (Refinance)

- 15-Year Fixed: 5.45% (Purchase) / 5.91% (Refinance)

- 5/1 ARM: 5.51%

- FHA 30-Year Fixed: 5.64%

- VA 30-Year Fixed: 6.14%

Why the gap between purchase and refinance? Lenders are still being a bit stingy with refis. They want to make sure you’re "sticky" before they give away the farm. If you bought your house back in late 2023 when rates were flirting with 8%, today’s numbers are basically a "Get Out of Jail Free" card. You’ve probably been waiting for this exact moment to pull the trigger on a refinance.

The "Hidden" Force Driving Rates Lower

Most people watch the Federal Reserve like hawks, but the Fed doesn't actually set mortgage rates. They set the Fed Funds Rate. Mortgage rates usually follow the 10-year Treasury yield.

But there’s a new player in the mix this year. The government-sponsored enterprises (GSEs) like Fannie Mae and Freddie Mac were recently instructed to buy about $200 billion in mortgage-backed securities. This is a big deal. By stepping in to buy these "mortgage bonds," they're artificially pushing the yields down.

🔗 Read more: Converting 149 Euro to US Dollars: What Most People Get Wrong About Exchange Rates

Zillow’s research team pointed out that this move alone could shave another 20 to 30 basis points off the rates we’re seeing. Without that intervention, we’d probably still be stuck at 6.4% or 6.5%. It’s a bit of a thumb on the scale, but if you’re trying to buy a house, you probably don't care about the ethics—you just want the lower payment.

The 6% Psychological Barrier

There is something almost magical about that 6% number. For the last 18 months, whenever rates dipped toward 6.1%, buyers would flood the market, and competition would drive home prices up. It’s a weird paradox. You want lower rates to save money, but lower rates bring out all the people who were sitting on the sidelines.

Lisa Sturtevant, the chief economist for Bright MLS, recently mentioned that 2026 is going to be a "transition year." It’s not a boom, and it’s not a bust. It’s just... better.

But here is the catch. If the 30-year fixed rate officially breaks below 6% and stays there, we could see a "feeding frenzy" in high-demand markets like the Sunbelt or the Pacific Northwest. If you wait for 5.8% to save another $40 a month, you might end up paying $20,000 more for the house because you’re suddenly in a bidding war with ten other people.

Will Rates Go Lower in 2026?

Predictions are messy. Honestly, anyone who tells you they know exactly where rates will be in July is probably selling something.

Goldman Sachs is betting that the Fed will pause its rate-cutting cycle this month (January) but might start up again in March. They're looking at a terminal rate of around 3.25% by the end of the year.

Then there's the "Powell Factor." Jerome Powell’s term as Fed Chair ends in May 2026. A change in leadership at the central bank always brings a certain amount of "what now?" to the markets. If a new chair is more aggressive about cutting rates to avoid a recession, we could see 5.5% by Christmas.

However, Ted Rossman at Bankrate warns that "stubbornly high inflation" could still pop up and ruin the party. We’re in a delicate balance. The economy is growing at about 2.3% (forecasted), and unemployment is steady around 4.4%. It’s a "Goldilocks" scenario—not too hot, not too cold.

The Real Cost of Waiting

Let’s look at the math. If you’re buying a $450,000 home with 20% down:

At 6.5%, your principal and interest is roughly $2,275.

At 6.11%, it’s roughly $2,185.

At 5.75%, it’s roughly $2,101.

💡 You might also like: California Marginal Tax Rates Explained (Simply)

Is it worth waiting six months to save $84 a month? Maybe. But if the house price goes up by 3% in that time because of increased demand, you’ve lost the gamble. The house price increase would cost you more in the long run than the interest rate savings.

Strategic Moves for Today’s Market

If you’re actually out there looking at houses right now, don't just take the first quote your bank gives you.

Lenders are hungry for volume. Because applications are finally ticking up (refinances jumped 40% recently!), banks are competing again. You have leverage.

- Check the local credit unions. They often don't have the same overhead as the big "monster" banks and can sometimes beat a 30-year fixed rate by 0.25%.

- Consider a 5/1 ARM if you aren't staying long. If you know this is a "five-year house," a rate of 5.51% is much more attractive than 6.11%. Just be sure you have a plan for when that rate resets.

- Ask about a "buy-down." Some sellers are so eager to close that they’ll pay to buy down your interest rate for the first two years. This is often better than a price cut.

Practical Next Steps

Stop watching the national news and start looking at your own credit score. A 760 FICO vs. a 680 FICO can be the difference between a 6.1% rate and a 6.8% rate. That gap is way bigger than any move the Fed is going to make this quarter.

First, get a pre-approval from at least three different types of lenders: a big national bank, a local credit union, and an online mortgage broker. The "spread" between their offers might surprise you.

Second, if you are a current homeowner with a rate above 7.25%, call your lender today. You don't necessarily need to wait for a full "refinance" if they offer a loan modification or a "streamline" refi.

Lastly, keep an eye on the January 28 Federal Reserve meeting. They likely won't cut rates then, but their "tone" will tell the bond market everything it needs to know for the spring. If they sound worried about the job market, mortgage rates will likely slide down another notch. If they sound worried about inflation, expect them to stay right where they are.