Houses are expensive. No, actually, they’re ridiculous. If you’ve looked at a Zillow listing lately and felt a sudden urge to scream into a pillow, you aren't alone. We are currently navigating one of the most confusing, frustrating, and statistically bizarre eras in the history of the United States housing market. It’s a mess.

For decades, the math was simple. You saved up, you bought a starter home, and you moved up. Now? That ladder feels like it’s been set on fire. We’re seeing a "lock-in" effect where homeowners with 3% mortgage rates refuse to move, coupled with a chronic shortage of millions of homes. It's a standoff. Nobody wants to sell, and nobody can afford to buy. But if you look under the hood, there’s a lot more happening than just "high rates."

The Inventory Crisis Is Not a Myth

We simply don't have enough roofs. According to data from Freddie Mac, the U.S. is short roughly 4 million housing units. This isn't just a leftover side effect of the 2008 crash, though that's where the rot started. After the Great Recession, homebuilders basically stopped building for a decade. They were scared. Who could blame them? But that decade of underbuilding created a massive hole that we are still trying to dig out of today.

When you have a shortage this massive, prices don't behave normally. Usually, when interest rates go up, prices go down. That’s Economics 101. But the United States housing market has decided to ignore the textbook. Even with mortgage rates hovering in the 6% to 7% range, prices in many metros—think Austin, Phoenix, or even parts of the Midwest—have remained stubbornly high or even climbed. Why? Because when there are only three houses for sale in a neighborhood and ten people need to move there, the price doesn't care about the Federal Reserve.

It’s local, too. You’ll see one town where prices are softening because a major employer left, while three towns over, people are still getting into bidding wars. It’s chaotic.

The 3% Mortgage Handcuffs

Let’s talk about your neighbor, Dave. Dave bought his house in 2021. He’s got a 2.75% interest rate. Dave might hate his kitchen, and he might really want an extra bedroom for his home office, but Dave is never leaving. To move to a similar house today, his monthly payment would nearly double.

This is the "Golden Handcuff" phenomenon. It has effectively frozen the secondary market. In a healthy United States housing market, you need churn. You need people moving for jobs, for growing families, or for downsizing. When that churn stops, the only thing left for buyers is new construction.

✨ Don't miss: Starting Pay for Target: What Most People Get Wrong

Builders are the New Kings

Since existing homeowners aren't selling, the big national builders like D.R. Horton and Lennar have stepped in to fill the gap. Honestly, they’re the only ones making the math work right now. How? Mortgage rate buydowns.

If you go to a builder today, they might offer you a 5.5% rate when the market is at 7%. They pay that difference upfront to get you in the door. It’s a brilliant move, but it also means that the "sticker price" of new homes is often inflated to cover the cost of those incentives. You're paying for the lower rate in the purchase price. It’s a shell game, basically.

The Institutional Buyer Boogeyman

You've probably heard that "BlackRock is buying all the houses." It's a popular talking point on TikTok. The reality is a bit more nuanced, though still pretty annoying for the average buyer. Institutional investors—companies that own more than 1,000 homes—actually own a relatively small percentage of the total single-family housing stock in the U.S., usually cited around 3% to 5%.

However, they are highly concentrated.

In cities like Atlanta, Charlotte, or Nashville, these firms sometimes buy up 20% of the entry-level homes that hit the market. They come in with all-cash offers and no contingencies. If you're a first-time buyer with an FHA loan and a 3.5% down payment, you can't compete with that. You just can't. It’s skewed the United States housing market in favor of capital over families in some of the fastest-growing regions of the country.

Why "Waiting for the Crash" Might Be a Bad Strategy

I hear this a lot: "I'm just waiting for 2008 to happen again."

🔗 Read more: Why the Old Spice Deodorant Advert Still Wins Over a Decade Later

I get it. A crash would make things affordable. But the fundamentals today are the polar opposite of 2008. Back then, we had an oversupply of homes and subprime loans given to anyone with a pulse. Today, we have an undersupply and some of the highest credit standards in history. Most homeowners today have a massive amount of equity. They aren't going to be forced into foreclosures en masse unless unemployment skyrockets to Great Depression levels.

Even if prices dip 5% or 10% in some overvalued markets, the lack of inventory acts as a floor. It keeps the bottom from falling out. If you’re waiting for a 40% drop to buy that house in the suburbs, you might be waiting until your kids are in college.

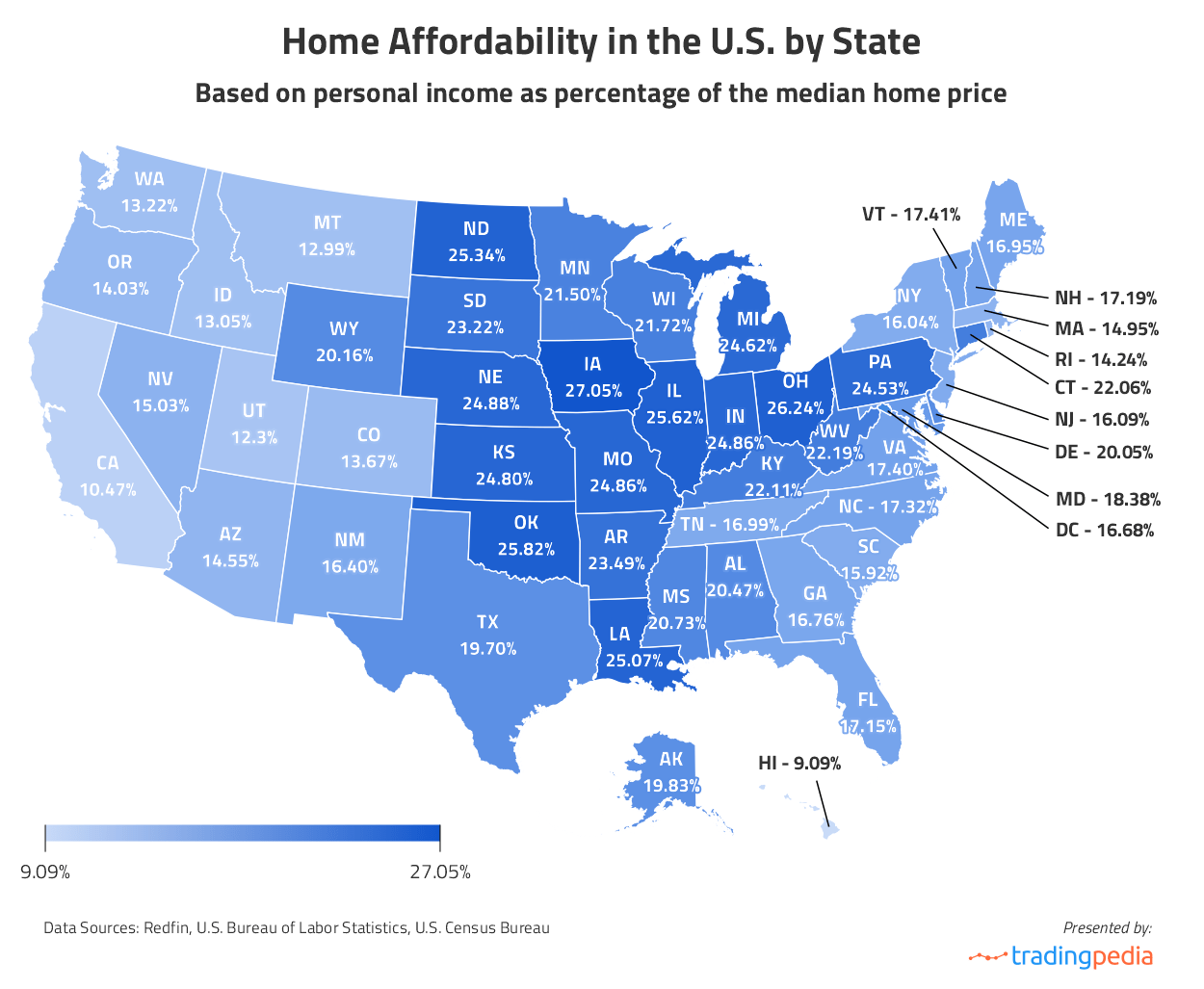

Regional Divides: The Tale of Two Markets

The United States housing market isn't one giant monolith. It’s thousands of tiny micro-markets.

- The Sunbelt: Places like Florida and Texas saw massive spikes during the pandemic. Now, they are seeing a lot of new inventory hit the market. In some parts of Florida, condo prices are actually dropping because insurance costs have become a nightmare.

- The Rust Belt: Cities like Columbus, Ohio, or Indianapolis are suddenly the "hot" markets. Why? Because they are actually affordable. You can still get a decent house for $300,000 there, which feels like a bargain compared to the coasts.

- The Coastal Giants: San Francisco and New York remain in their own stratosphere. Prices there don't go down; they just pause.

The Insurance Wildcard

We have to talk about insurance. It is becoming the "silent killer" of affordability. In states like California, Florida, and Louisiana, homeowners' insurance premiums are doubling or tripling. Some companies are leaving these states entirely. Even if you can afford the mortgage and the taxes, the insurance might push your monthly DTI (debt-to-income) ratio over the edge. This is a structural risk to the United States housing market that wasn't even on the radar five years ago.

The Rise of the Multi-Generational Workaround

People are getting creative. Or desperate. Depends on how you look at it.

We are seeing a massive uptick in "co-buying." Friends are buying houses together. Siblings are pooling resources. Parents are building ADUs (Accessory Dwelling Units) in the backyard so their adult kids have a place to live. It’s a return to a more communal way of living that the U.S. moved away from after World War II.

💡 You might also like: Palantir Alex Karp Stock Sale: Why the CEO is Actually Selling Now

Also, "house hacking" is no longer just for weird real estate investors on YouTube. It’s becoming a survival strategy. Buying a duplex, living in one side, and renting out the other is often the only way a young professional can justify a $4,000 monthly mortgage payment.

Actionable Steps for the Current Climate

So, what do you actually do? If you’re looking at the United States housing market and wondering if there’s a path forward, here is the reality of what works right now:

Focus on the Monthly Payment, Not the Price

Don't obsess over the $500,000 price tag. Obsess over the "all-in" monthly cost, including the new, higher insurance rates and property taxes. If you can’t make the math work at a 7% interest rate, you can’t afford the house. Do not count on "refinancing later." Marry the house, but don't just date the rate—assume you're stuck with that rate for at least five years.

Look at "Stale" Listings

Everyone wants the shiny new house that hit the market on Friday. Those get the bidding wars. Look for the house that has been sitting for 45 days. Maybe the photos are bad. Maybe it smells like a wet dog. These sellers are often tired and willing to negotiate on price or offer a credit for a rate buydown.

Explore Non-Traditional Financing

If you’re a veteran, the VA loan is your best friend—no down payment and usually better rates. If you’re looking in more rural areas (which are often just outside major suburbs), the USDA loan offers 0% down. Also, check for state-specific first-time homebuyer programs. Some states are literally giving away $10,000 to $20,000 in down payment assistance just to get people into homes.

Audit Your Insurance Options Early

Before you even put an offer in, get an insurance quote. In today’s market, a high-risk area can turn a "great deal" into a financial anchor. Knowing the insurance cost is just as important as the home inspection.

Expand the Search Radius

The "drive until you qualify" mantra is back. If your heart is set on a specific zip code, you’re going to pay a premium. Moving just 15 minutes further out can sometimes shave $50,000 off the price tag. With remote and hybrid work still being a thing for many, that extra commute time might be worth the hundreds of dollars saved every month.

The United States housing market is in a period of painful transition. We are moving away from the era of "free money" and into a period where housing is treated as the scarce, expensive resource it actually is. It isn't easy, and it isn't always fair, but understanding the underlying mechanics—the inventory gap, the rate lock, and the regional shifts—is the only way to navigate it without losing your mind.