You open your paycheck. You see the gross pay and feel a brief flash of pride. Then, your eyes wander down to the deductions. Federal tax is expected, sure, but that state withholding line? Sometimes it feels like a physical punch to the gut. If you live in a place like California or New York, you basically feel like a silent partner in a business where the government takes a massive cut without ever helping you move the furniture.

High taxes aren't just numbers on a spreadsheet. They’re the reason people pack U-Hauls. They’re the reason your neighbor suddenly decided to "retire" in Florida. But the truth about the highest state income taxes is actually more complicated than just one big percentage. It's a messy mix of brackets, credits, and cost-of-living adjustments that most people don't really bother to untangle until they’re already signing a lease in a different zip code.

The California King (and Not the Mattress Kind)

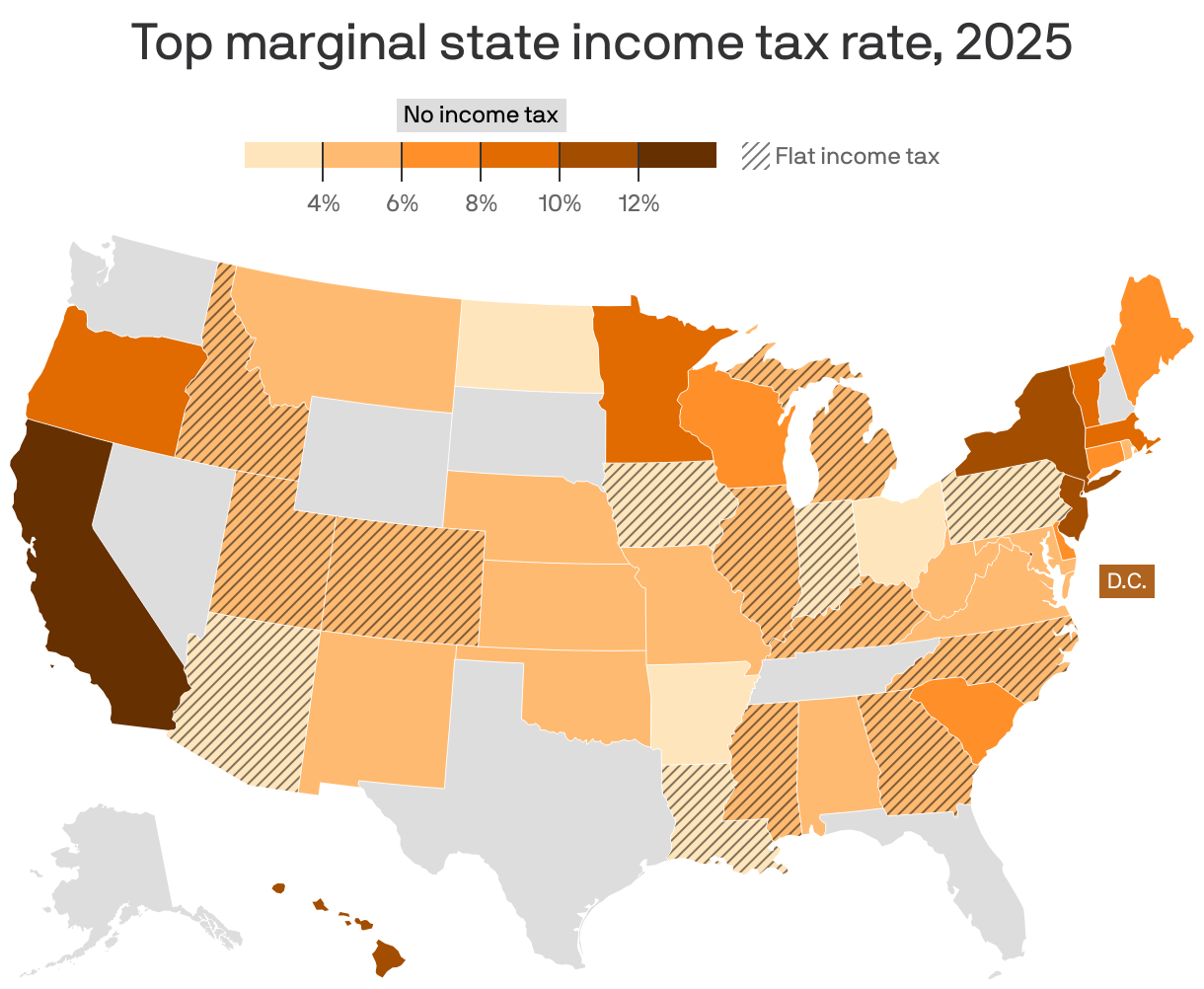

California is the heavy hitter. It's the one everyone talks about at dinner parties when the subject of "getting out" comes up. The top marginal rate hits a staggering 13.3%. That’s a lot. To be fair, that top rate includes a 1% mental health services tax on income over $1 million, so if you aren't clearing seven figures, you aren't paying the full freight.

But even for the middle class, it's aggressive. The state uses a progressive system with ten different brackets. It’s designed to squeeze the most out of high earners, which is why the state budget relies so heavily on the capital gains of a few tech billionaires. When the stock market dips in Silicon Valley, the whole state feels the shiver.

Honest talk: California’s high taxes are often a "sunshine tax." People pay it because they want the Pacific Ocean, the Sierra Nevadas, and the economic engine of the world's fifth-largest economy. But as remote work became the standard for many white-collar jobs, that trade-off started looking a lot less appealing. Why pay Sacramento 13% when you could work from a porch in Austin and pay 0%?

The Northeast Corridor: Wealth and Withholding

Then you have New York. It’s the classic rival. For a long time, New York’s top rate hovered around 8.82%, but recent hikes have pushed the top bracket for multi-millionaires up to 10.9%. If you live in New York City, you get hit with a "triple threat." You pay federal, you pay state, and then the city takes its own bite—up to another 3.876%.

Think about that. If you're a high-earning professional in Manhattan, over half of your next dollar earned is gone before you can even think about spending it. It's wild.

New Jersey isn't exactly a tax haven either. Its top rate is 10.75% for those making over $1 million. For years, New Jersey has had a bit of a tug-of-war with its wealthier residents. When David Tepper, a billionaire hedge fund manager, moved to Florida a few years ago, it actually caused a noticeable gap in the state's tax revenue projections. That’s how fragile these systems can be when they rely on a handful of "whales."

✨ Don't miss: Cuanto son 100 dolares en quetzales: Why the Bank Rate Isn't What You Actually Get

Hawaii: Paradise at a Premium

Most people forget about Hawaii in the tax conversation. They think about pineapples and surfing. But Hawaii has some of the highest state income taxes in the country, with a top rate of 11%.

Here’s the thing: Hawaii is expensive for everything. Shipping costs make groceries sky-high, electricity is pricey, and then the state takes a double-digit percentage of your income. They do this because they have a small land mass and a limited industrial base. They need the revenue to maintain infrastructure on a chain of islands. It’s a literal price of admission for living in the tropics.

The "Middle Class" Trap in High-Tax States

We focus on the top rates because they make for good headlines. "State Takes 13%!" sounds scary. But for someone making $75,000, the "effective" rate is what actually matters.

Take Oregon. Oregon has a top rate of 9.9%. That sounds lower than California, right? But Oregon hits that top rate much faster. In California, you don't hit the double digits until you’re making serious money. In Oregon, you reach high brackets relatively quickly. Plus, Oregon has no sales tax.

This is the trade-off.

State governments are going to get their money one way or another. If they don't get it from your paycheck, they’ll get it at the cash register (sales tax) or when you pay your mortgage (property tax).

- New Hampshire: No income tax on wages, but they have some of the highest property taxes in the nation.

- Texas: No income tax, but try looking at a property tax bill in a nice suburb of Dallas or Austin. It’ll make your hair stand on end.

- Washington: No state income tax, but they have a high sales tax and recently implemented a capital gains tax that has been tied up in legal battles.

Basically, there is no "free" state. There are just different ways to pay the piper.

🔗 Read more: Dealing With the IRS San Diego CA Office Without Losing Your Mind

Why Do These States Stay High?

You’d think everyone would just leave. Some do. But many stay. Why?

Services.

States with the highest state income taxes generally offer more robust social safety nets, better-funded public universities, and more extensive public transit. Massachusetts (often called "Taxachusetts," though its rates have actually become more competitive recently) has some of the best public schools in the world. Minnesota, with a top rate of 9.85%, consistently ranks at the top for quality of life and healthcare access.

You're buying a different version of society. If you live in a low-tax state, you might save $5,000 a year in income tax, but you might spend $6,000 on private school tuition because the local public school is struggling. Or you might spend more on tolls because the roads aren't funded by general tax revenue.

It’s a "pick your poison" scenario.

The Myth of the Flat Tax

Some states, like Illinois, have a flat tax. Everyone pays the same percentage regardless of whether they make $20,000 or $20 million. Illinois currently sits at 4.95%.

On paper, this sounds fair. In practice, it’s a massive point of political contention. Critics argue it places an unfair burden on the poor, who spend a larger percentage of their income on basic necessities. Proponents say it’s the only way to keep the state's business climate predictable. Illinois has struggled with massive pension debt for decades, which keeps the pressure on that "flat" rate to slowly creep upward.

💡 You might also like: Sands Casino Long Island: What Actually Happens Next at the Old Coliseum Site

Real-World Impact: The 2026 Shift

As we look at the data for 2026, we're seeing a trend. The gap between "high tax" and "low tax" states is widening, but the middle is hollowing out. States like North Carolina are aggressively cutting their rates to lure businesses away from the Northeast.

Meanwhile, high-tax states are doubling down on "wealth taxes" or "mansion taxes." They’re betting that the ultra-wealthy will stay for the culture, the networking, and the lifestyle, even if it costs them a few extra points on their tax return.

What You Should Actually Do

If you're looking at your state's tax rate and feeling grumpy, don't just look at the top number. Do the math on your "Total Tax Burden."

- Check the Brackets: Are you actually in the top bracket? Most people aren't.

- Look at Reciprocity: If you live in one state and work in another (common in the Philly/NJ or NYC/CT areas), make sure you aren't being double-taxed. Most states have agreements to prevent this, but you have to file the paperwork correctly.

- Factor in Sales and Property Tax: A 0% income tax state can be more expensive if you're buying a home or spending a lot on taxable goods.

- Consider Credits: Many high-tax states offer generous credits for childcare, education, or energy-efficient home improvements that can wipe out a big chunk of what you owe.

Actionable Steps for the Tax-Hate Crowd

Don't just complain. If the highest state income taxes are eating your lunch, take a look at your retirement contributions. Most states follow federal rules for 401(k) and IRA deductions. By maxing out your pre-tax retirement accounts, you lower your taxable income at both the federal and state levels.

Also, look into Health Savings Accounts (HSAs). They are one of the few "triple tax-advantaged" tools available. You put money in tax-free, it grows tax-free, and you take it out tax-free for medical expenses. In a high-tax state, this is like finding a legal cheat code.

Lastly, if you're a freelancer or small business owner, look into "Pass-Through Entity" (PTE) taxes. Many high-tax states created these as a workaround for the federal SALT (State and Local Tax) deduction cap. It allows the business to pay the state tax, which then becomes a deduction on your federal return. It’s complex, but it can save you thousands.

The bottom line? Taxes are the price we pay for a civilized society, but nobody said you have to leave a tip. Understand your state's specific rules, use the available deductions, and stop looking at the gross pay—it'll only break your heart.

Next Steps:

- Gather your last three pay stubs and calculate your actual effective state tax rate (Total State Tax Paid / Gross Income).

- Compare this number against the "Total Tax Burden" rankings from the Tax Foundation to see where your state truly ranks when property and sales taxes are included.

- Consult with a CPA if you’re considering a move; the "exit taxes" and residency audits in states like California and New York are notoriously aggressive.