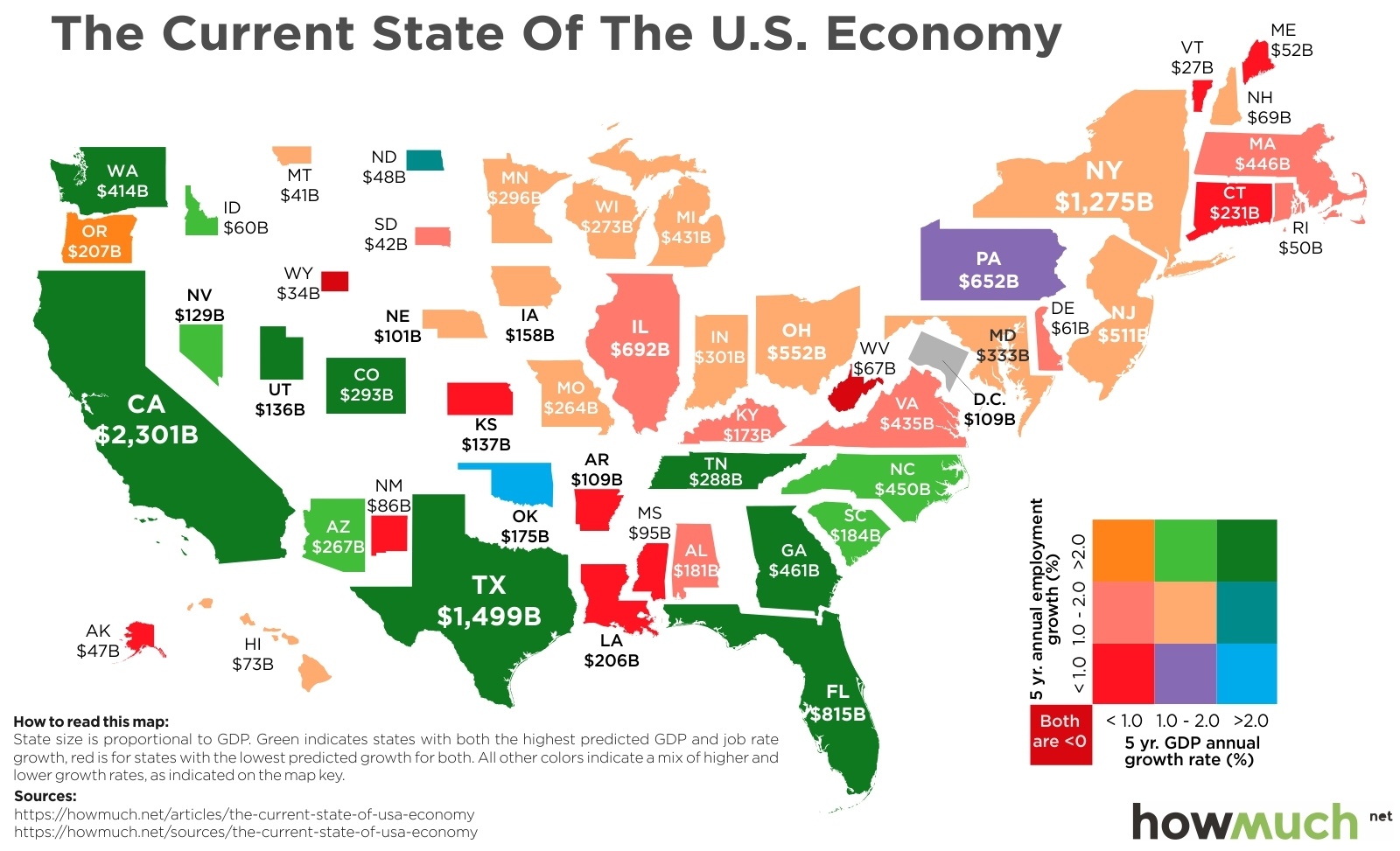

Economists love spreadsheets. They look at a 2.5% GDP growth rate or a 3.7% unemployment figure and decide everything is basically fine. But if you’ve been to a grocery store lately, or tried to get a quote for car insurance, you know those numbers don't tell the whole story. The state of the economy today is a weird, fragmented reality where the "macro" looks great and the "micro" feels like a constant squeeze. It's confusing. Honestly, it’s exhausting.

We are living through a "vibecession." That’s a term coined by analyst Kyla Scanlon to describe the massive gap between upbeat economic data and how people actually feel. In 2026, we aren't just dealing with the aftermath of the high-inflation era; we are dealing with a structural shift in what things cost.

The disconnect is real.

Think about it. The Federal Reserve spent years hiking interest rates to cool things down. They wanted to see a "soft landing." For the most part, Jerome Powell and the Fed actually pulled it off. We didn't see the mass layoffs everyone feared in 2023 or 2024. People have jobs. They’re spending money. But they’re also carrying record-high credit card debt, which topped $1.1 trillion recently according to the New York Fed. We’re working more, earning more, and somehow feeling like we’re falling behind.

Why the State of the Economy Today Feels So Fragile

If you ask a homeowner with a 3% mortgage how they feel, they’ll tell you they’re sitting on a goldmine. Ask a 26-year-old trying to buy their first condo, and they’ll tell you the American Dream is a scam. This "haves vs. have-nots" split is the defining feature of the state of the economy today.

Housing is the biggest culprit.

The inventory of existing homes is still stubbornly low. Why? Because nobody wants to trade their "free money" mortgage from 2020 for a 7% rate today. This has created a frozen market. According to Redfin, the median home price hasn't meaningfully dropped despite the high rates, because there just isn't enough supply. It’s a supply-demand nightmare that keeps young professionals trapped in the rental cycle, where prices are also rising, albeit slower than before.

The Shadow of "Sticky" Inflation

Inflation has slowed down. That is a fact. But "slowing inflation" does not mean "falling prices." It just means prices are rising more slowly. This is the biggest misconception people have about the state of the economy today. When the Bureau of Labor Statistics (BLS) reports a 2% or 3% CPI, they aren't saying your eggs are going back to $1.50. They’re saying those $5 eggs are just going to stay $5 for a while.

Some costs are "sticky."

✨ Don't miss: Rough Tax Return Calculator: How to Estimate Your Refund Without Losing Your Mind

- Insurance: Auto insurance premiums have spiked over 20% in some regions due to the high cost of repairs and specialized tech in EVs.

- Services: Going to a restaurant or getting a haircut costs way more because labor is expensive. Business owners have to pay more to keep staff, and they pass that to you.

- Electricity: Utility bills are climbing as the grid struggles with aging infrastructure and the massive power demands of AI data centers.

It’s a death by a thousand cuts. You might get a 4% raise at work, but if your rent goes up 5% and your car insurance goes up 15%, you've effectively taken a pay cut.

The Labor Market Paradox

We keep hearing about "Full Employment." It sounds like a victory. But look closer at the state of the economy today and you'll see a labor market that is shifting in ways that don't always favor the worker.

Yes, the unemployment rate is low. But "underemployment" and the "gigification" of the white-collar world are real trends. Companies aren't doing the massive, 10,000-person layoffs we saw in early 2023 as often, but they are "quiet cutting." They make roles so miserable that people quit, or they just don't backfill positions.

The tech sector is a prime example. The gold rush of 2021 is over. Now, it's about "efficiency." Mark Zuckerberg called it the "Year of Efficiency" at Meta, but that mindset has spread everywhere. If an AI tool can do 20% of a junior analyst's job, the company isn't hiring a new analyst. They’re just giving the current one more work.

Real Wages vs. The Grocery Receipt

Real wages—which is your pay adjusted for inflation—actually started to grow again recently. That’s good! It means, on paper, you’re winning.

But humans don't live on paper.

We live in a world where a bag of chips is $6 and a "family size" box of cereal is basically the size of a regular box from five years ago. This "shrinkflation" is a psychological tax. Even if you have the money, the feeling of being "ripped off" creates a sense of economic pessimism. This is why consumer sentiment surveys, like the one from the University of Michigan, often show people feeling gloomy even when the stock market is hitting all-time highs.

The AI Factor: A New Economic Engine or a Job Killer?

You can't talk about the state of the economy today without mentioning Artificial Intelligence. We are currently in the "infrastructure phase." Billions of dollars are being poured into Nvidia chips and massive data centers. This is propping up the S&P 500. A handful of stocks (the "Magnificent Seven") have been responsible for a huge chunk of the market's gains.

🔗 Read more: Replacement Walk In Cooler Doors: What Most People Get Wrong About Efficiency

But for the average worker, AI is a giant question mark.

Goldman Sachs research suggested that AI could eventually automate the equivalent of 300 million full-time jobs. That doesn't mean 300 million people will be unemployed, but it does mean their jobs will change radically. Right now, AI is a productivity booster. It helps coders write faster and marketers draft emails in seconds. The long-term impact on wages, however, is debated. If productivity goes up but the gains only go to the shareholders, the wealth gap will keep widening.

Debt: The Ticking Clock

Here’s the scary part. The US National Debt is over $34 trillion. Most people ignore this because it feels abstract. But in the state of the economy today, debt matters because the cost of servicing that debt has skyrocketed.

When interest rates were near zero, the government could borrow for basically nothing. Now, the US is spending hundreds of billions just on interest payments. This limits what the government can do. There’s less money for infrastructure, less for social programs, and more pressure to keep taxes high or even raise them.

On a personal level, consumers are feeling the same burn.

- Credit Cards: Average rates are hovering around 21%. If you carry a balance, you’re essentially flushing money down the toilet.

- Buy Now, Pay Later (BNPL): Services like Affirm and Klarna have exploded. They don't always show up in traditional debt stats, but they represent a huge "phantom debt" for Gen Z and Millennials.

- Auto Loans: The average monthly payment for a new car is now over $700. People are taking out 72-month or even 84-month loans just to afford a Toyota.

Is a Recession Coming?

This is the million-dollar question. For two years, experts have predicted a recession was "six months away." It hasn't happened. The US economy has been surprisingly resilient.

Why?

Mostly because of the American consumer. We just keep spending. Maybe it’s "doom spending"—the idea that since we can't afford a house anyway, we might as well buy a $1,200 concert ticket or a nice dinner. Whatever the reason, that spending keeps the wheels turning.

💡 You might also like: Share Market Today Closed: Why the Benchmarks Slipped and What You Should Do Now

However, the "excess savings" from the pandemic era have mostly dried up. The buffer is gone. If we see a sudden spike in unemployment, the state of the economy today could shift from "stagnant but okay" to "downward spiral" very quickly. Most analysts are leaning toward a "low growth" scenario rather than a total collapse, but "low growth" feels like a recession when you're used to a booming market.

Actionable Steps for Navigating This Economy

Since we can't control the Fed or global oil prices, we have to play the hand we’re dealt. The state of the economy today requires a defensive mindset mixed with some strategic aggression.

1. Audit Your "Sticky" Costs

Don't just complain about your insurance going up. Shop it. Every six months. Loyalty to a brand (insurance, internet, cell phone) is a tax you can't afford right now. Use tools like Jerry or Gabi to compare rates.

2. Attack High-Interest Debt First

If you have a credit card balance at 20%+, that is an emergency. It is a guaranteed -20% return on your money. Use the "Debt Avalanche" method: pay the minimum on everything but throw every extra dollar at the highest interest rate.

3. Cash is Actually Useful Again

For the first time in a decade, your savings account can actually make you money. If your bank is still paying you 0.01%, move your money to a High-Yield Savings Account (HYSA). You can easily find rates above 4% right now. It’s free money.

4. Upskill for the AI Shift

Don't ignore AI tools because they’re "scary" or "annoying." Learn to use them. Whether it’s ChatGPT for writing or Midjourney for design, being the person who knows how to "prompt" makes you more valuable than the person who is replaced by the tool.

5. Re-evaluate Your Housing Strategy

If you're a buyer, look at "rate buy-downs" where the seller pays to lower your interest rate for the first few years. If you're a renter, try to negotiate. With many new apartment buildings finally hitting the market in some cities, landlords are becoming slightly more flexible than they were two years ago.

The state of the economy today isn't a disaster, but it isn't a party either. It’s a period of "The Great Reset," where we are all relearning what things are actually worth. Staying informed and staying nimble is the only way to come out on top.

Immediate Next Steps:

- Check your credit card interest rates today; if they're above 18%, look into a balance transfer card or a personal loan to consolidate.

- Move your emergency fund to a High-Yield Savings Account to take advantage of the current interest rate environment.

- Review your recurring subscriptions—those "small" monthly charges are the fastest way to bleed money in a high-cost environment.

---