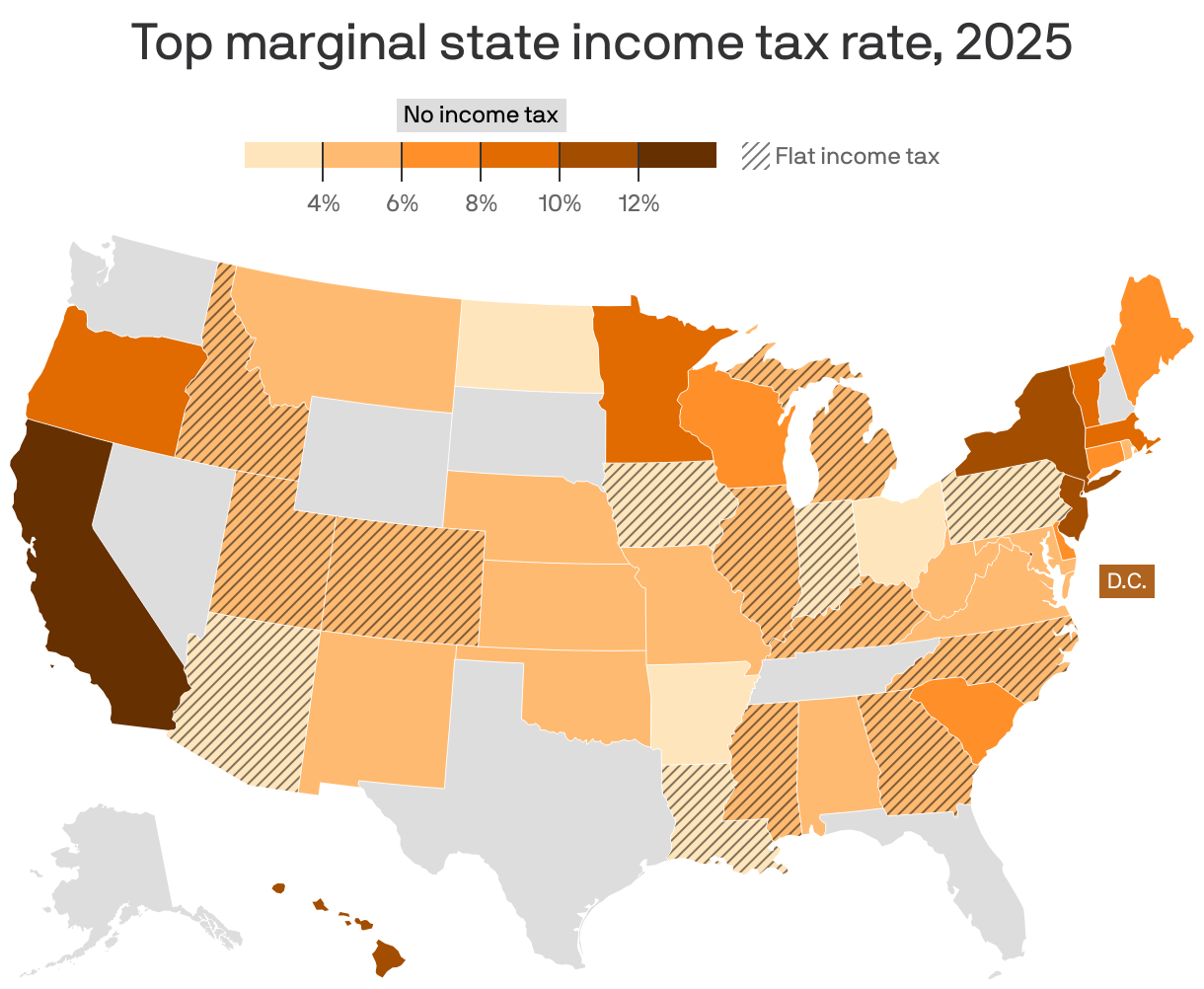

California's tax system is a beast. Honestly, there is no other way to put it. If you live in the Golden State, you’re dealing with a progressive tax structure that is among the most aggressive in the entire country. Most people just look at the california state income tax table and see a bunch of percentages, thinking they can just multiply their salary by one of those numbers and call it a day. It doesn't work like that. Not even close.

You’ve got to account for the mental gymnastics of brackets, inflation adjustments, and that "Millionaire's Tax" that kicks in way sooner than you'd expect.

The Franchise Tax Board (FTB) updates these numbers every year to account for the California Consumer Price Index. For the 2024 tax year (the ones you're likely filing now in early 2026), the brackets shifted slightly to prevent "bracket creep." This is when inflation raises your salary, but because the tax brackets don't move, you end up paying a higher percentage of your income even though your buying power stayed the same. It’s a stealthy way to lose money.

How the California State Income Tax Table Actually Functions

Most people think if they earn $100,000, they fall into one bracket and pay that rate on everything. Wrong. California uses a graduated system.

Think of it like a series of buckets. The first bucket holds about $10,000 and is taxed at a tiny 1%. Once that bucket overflows, the next chunk of your money goes into the 2% bucket. This keeps happening until you hit the top rates. By the time you’re a high earner, you’re looking at a 12.3% top rate, plus an extra 1% surcharge if you’re pulling in over seven figures for mental health services. That brings the total to 13.3%. It's a lot.

Let’s look at the actual breakdown for a single filer for the most recent data set.

If you're single, the first $10,412 of your taxable income is taxed at 1%. Pretty cheap. The next segment, from $10,413 up to $24,684, jumps to 2%. Then it hits 4% for the next $14,000 or so. By the time you hit $61,214 in taxable income, you are already at 8%. Just for comparison, some states don't even have an income tax. But California isn't "some states." We have high-speed rail projects to fund and massive social programs.

Why Filing Status Changes Everything

Your filing status is basically the "difficulty setting" of your tax return. If you’re Married Filing Jointly, the thresholds in the california state income tax table essentially double.

✨ Don't miss: Starting Pay for Target: What Most People Get Wrong

For a married couple, that 1% bracket covers the first $20,824. It provides a bit of a buffer, but once you both start earning decent salaries, you hit the "marriage penalty" territory where your combined income pushes you into those scary 9.3% or 10.3% brackets much faster than you’d anticipate.

The Mental Health Services Act Tax

You might have heard of the "Millionaire’s Tax." Formally, it’s the Mental Health Services Act, passed back in 2004 via Proposition 63. If your taxable income exceeds $1 million, California tacks on an additional 1% tax.

It’s not indexed for inflation.

This means as time goes on, more people get swept into this category. It’s a flat 1% on every dollar over that million-mark. While it sounds like a "rich person problem," it significantly impacts small business owners who file as S-corps or sole proprietors because that business income flows directly onto their personal tax return. One good year of sales can result in a massive, unexpected tax bill that eats into your operating capital.

The Standard Deduction and Personal Credits

Before you even look at the table, you have to subtract your standard deduction. For 2024/2025, that’s roughly $5,363 for individuals. It’s not much. Compared to the federal standard deduction, California’s is tiny.

However, California does something unique with personal exemption credits. Instead of reducing the income you are taxed on (like a deduction), a credit reduces the actual tax you owe, dollar for dollar. It’s usually around $144 per person. It’s a small consolation prize for living in one of the highest-taxed jurisdictions in the world.

Common Myths About California Taxes

I hear this all the time: "I don't want a raise because it will put me in a higher bracket and I'll take home less money."

🔗 Read more: Why the Old Spice Deodorant Advert Still Wins Over a Decade Later

That is mathematically impossible.

Because of how the california state income tax table is structured, only the dollars within that specific bracket are taxed at the higher rate. If you move from the 8% bracket to the 9.3% bracket because you earned an extra $1,000, only that $1,000 is taxed at 9.3%. The rest of your money stays taxed at the lower rates. Take the raise. Always.

Another misconception involves capital gains. In the federal system, if you hold an asset for more than a year, you get a "long-term capital gains" rate which is lower than your regular income tax. California does not care. To the FTB, a dollar is a dollar. Whether you worked 80 hours a week for it or sold a vintage surfboard for a profit, it’s all taxed at the same ordinary income rates from the table. This is a massive trap for people selling real estate or stocks.

Surprising Details for Remote Workers

Since 2020, the "sourcing" of income has become a legal battlefield. If you work for a California company but live in Austin, Texas, does California get a cut?

Usually, California taxes you based on where the work is performed. But they are aggressive about "California-source income." If you are a resident, you are taxed on everything you earn worldwide. If you are a non-resident, you are only taxed on what you earned while physically in the state.

The FTB is famous for tracking people down. They look at cell phone records, credit card swipes, and even where you walk your dog to prove you spent more than half the year in the state. If they decide you’re a resident, they apply the full california state income tax table to every cent you made that year, regardless of where the office was.

The Impact of Local Taxes

We’re focusing on the state table here, but remember that California doesn’t really allow local cities to tack on their own income taxes (unlike New York City or Philadelphia). The rate you see on the state table is generally what you pay, plus your federal taxes. The "hidden" local taxes in California usually come in the form of astronomical sales tax or specialized property tax assessments (Mello-Roos).

💡 You might also like: Palantir Alex Karp Stock Sale: Why the CEO is Actually Selling Now

How to Lower Your Effective Rate

Since the brackets are so steep, your goal is to lower your "Taxable Income" so you stay in the lower rungs of the table.

- Maximize 401(k) and 403(b) contributions: This money is taken off the top before the state even sees it.

- Health Savings Accounts (HSA): Be careful here. California is one of the few states that does not recognize HSAs as tax-exempt. You still pay state tax on those contributions.

- California 529 Plans: While there's no state tax deduction for putting money in, the growth is tax-free for education.

- Itemized Deductions: If you have a massive mortgage in a place like San Francisco or LA, your interest payments might exceed the standard deduction.

Real World Example: The $80k Earner

Let’s say you’re single and make $80,000 in taxable income. You don't just pay 9.3% on $80,000.

- You pay 1% on the first ~$10k.

- You pay 2% on the next ~$14k.

- You pay 4% on the next ~$14k.

- You pay 6% on the next ~$15k.

- You pay 8% on the next ~$15k.

- Finally, you pay 9.3% on the remaining ~$12k.

When you blend those all together, your "effective" tax rate is actually around 5-6%. That feels a lot better than 9.3%, doesn't it? But then you remember the federal government takes their 22% or 24%, and suddenly your paycheck looks a lot smaller.

Actionable Steps for Tax Season

Don't wait until April 15th to look at the california state income tax table. By then, it’s too late to change anything.

First, go pull your last pay stub. Look at the "Year to Date" California withholding. If that number doesn't look like at least 5% of your gross pay (for average earners) or 9% (for high earners), you are going to owe money. You can file a Form DE 4 with your employer to adjust your state withholding specifically. This is different from the federal W-4.

Second, if you're a freelancer, pay your estimated taxes quarterly. California’s underpayment penalty is no joke. They calculate it based on the interest rate they decide, and it compounds. If you wait until the end of the year to pay, you’re basically giving the state a high-interest loan.

Third, check for the California Earned Income Tax Credit (CalEITC). Even if you don't qualify for the federal version, California has lower income thresholds that might put a few hundred dollars back in your pocket if you earned less than $30,000.

Lastly, keep an eye on the "Young Child Tax Credit" if you have kids under age 6. It’s a refundable credit, meaning even if you owe zero taxes, the state will send you a check. It’s one of the few ways to actually "beat" the table.

California’s tax code is a living document. It changes with every election and every budget cycle. Stay on top of the brackets, adjust your withholdings early, and never assume that last year's math applies to this year's income.