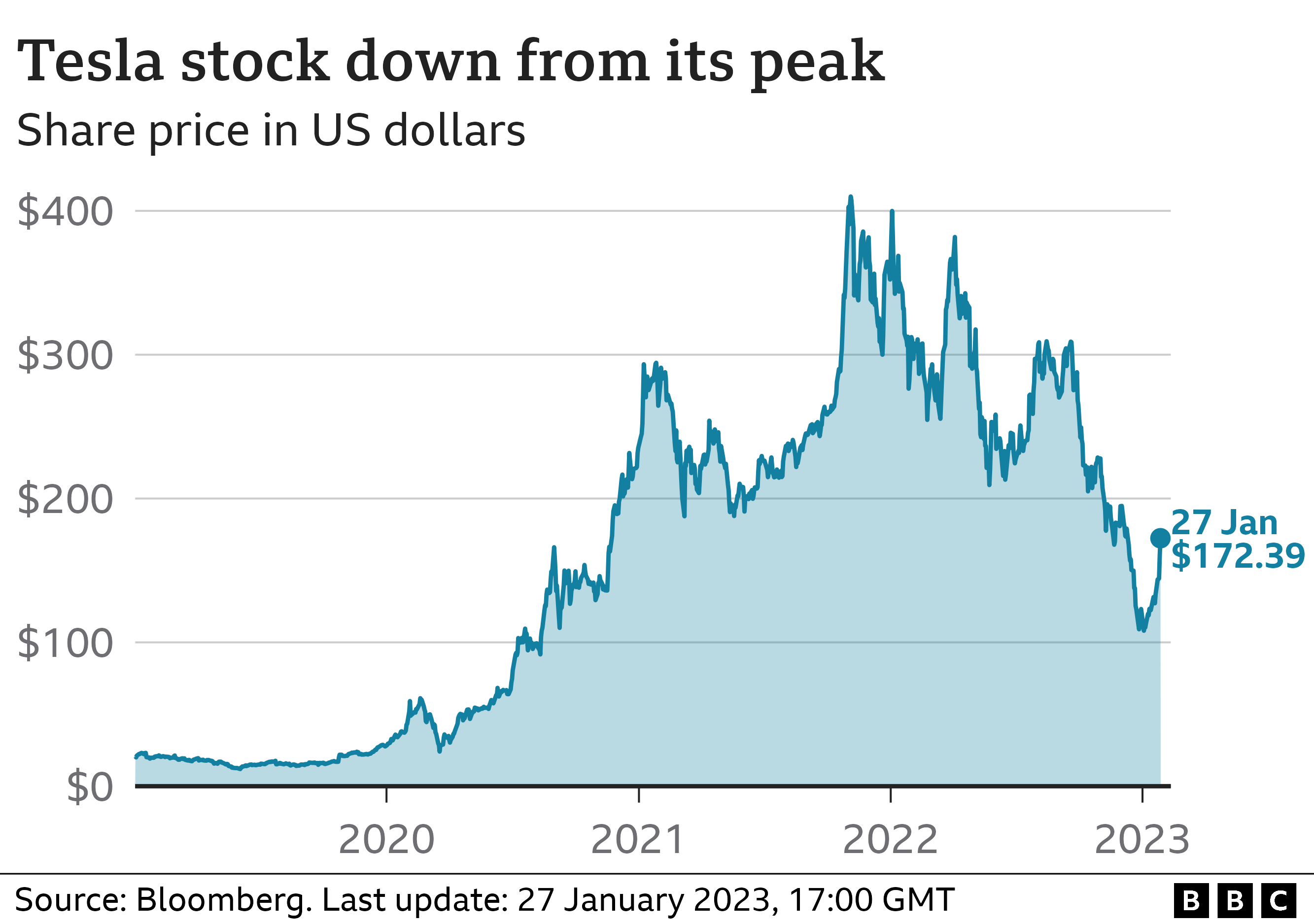

Honestly, trying to pin down Tesla stock is like trying to catch a greased pig in a thunderstorm. One day you're looking at a tech titan leading the AI revolution, and the next, it's just a car company struggling with delivery targets and razor-thin margins. As we kick off 2026, the vibe around TSLA is decidedly split. On one hand, you have the "Musk-eteers" betting the farm on robotaxis; on the other, the bears are growling about a 1.6 million vehicle delivery year in 2025 that actually saw a year-on-year drop.

It's messy.

💡 You might also like: Republica Dominicana Dollar Value: What Most People Get Wrong

If you’re looking for a simple "buy or sell" answer, you're probably in the wrong place. The reality is that Tesla is currently two different companies fighting for the same ticker symbol. There’s the legacy EV business, which is feeling the heat from BYD and a cooling global appetite for expensive EVs. Then there’s the "Everything Else" business—Megapacks, FSD subscriptions, and the Optimus pipe dream—that bulls say justifies a $1.1 trillion market cap.

The Numbers Nobody Wants to Talk About

Let's look at the cold, hard data from the January 2, 2026, delivery report. Tesla delivered roughly 1.636 million vehicles in 2025.

That’s an 8.6% dip from the previous year. For a company that used to brag about 50% compound annual growth, that's a tough pill to swallow. Net profit also took a hit, sliding about 12% as price cuts continued to gnaw at the bottom line.

But here is where it gets weird.

While the car business was "meh," the energy storage side went absolutely nuclear. Tesla deployed 46.7 GWh of energy storage in 2025. That’s nearly a 50% jump. We’re talking about Megapacks—those giant batteries that look like shipping containers—becoming a legitimate pillar of the company. In fact, for the first time, energy storage revenue is making up about 12% of the total pie, with gross margins north of 30%.

That is significantly higher than the 16% margins they’re pulling on cars right now.

Why the $25,000 Car Still Matters

You've probably heard the rumors. The "Model 2" or the "next-gen platform."

For a while, everyone thought Elon had killed the affordable Tesla in favor of the Cybercab. But as we head into 2026, the pressure to produce a high-volume, low-cost vehicle is reaching a fever pitch. Without it, Tesla is just a luxury brand in a world where people are tightening their belts.

- The Model Y Refresh: The 2026 "Juniper" update is finally hitting streets. It’s got the full-width light bar and the quieter cabin from the Model 3 "Highland" update.

- The Price Gap: Right now, a Model Y starts around $41,630. That’s still too much for the mass market.

- The Missing Link: A $25,000 car would change the math. It would give Tesla the "fleet" it needs to actually train the AI they keep talking about.

The FSD Gamble: Subscriptions vs. Sales

On January 14, 2026, Tesla made a move that annoyed a lot of people but made Wall Street perk up. They stopped selling Full Self-Driving (FSD) as a one-time $12,000 or $15,000 purchase.

💡 You might also like: Filing for Unemployment MI: What Usually Trips People Up

Now, it’s subscription only.

Basically, if you want your car to drive itself, you’re paying $99 a month (or whatever the "Musk-inflation" price is this week) forever. Elon’s logic? He needs 10 billion miles of training data to reach "unsupervised" autonomy. He’s currently at about 7.2 billion.

By forcing everyone into a subscription model, Tesla is trying to build a recurring revenue stream that looks more like Netflix than Ford. If they hit 10 million active FSD subscribers, the stock price could theoretically go to the moon. If they don't? Well, then it's just a very expensive cruise control system.

What Analysts Are Actually Saying

If you ask ten different analysts where Tesla stock is going in 2026, you’ll get twelve different answers. It’s hilarious, really.

- The Bulls (Wedbush/Dan Ives): They’re still pounding the table for a $600 price target. They see Tesla as the "most undervalued AI play in the world."

- The Middle Ground (Morgan Stanley): Adam Jonas and the team are sitting around $425. They love the AI and the robots, but they’re worried about the car business's execution.

- The Bears (GLJ Research): These guys are still calling for a crash to $25. They think the whole thing is a "meme coin" built on broken promises.

Honestly, the median target is hovering around $391. Given that the stock closed around $437 on January 16, 2026, the "smart money" is actually suggesting the stock might be a bit overextended right now.

The "X" Factors for 2026

We can't talk about Tesla without talking about the drama.

The Cybertruck is still a polarizing mess. Some people love the stainless steel triangle; others call it a "sales disaster" because it hasn't reached the mass-market volume promised in 2023. Then there’s the Cybercab. Production is supposedly starting in April 2026, but we’ve heard that song before.

And then there's the Optimus robot. Tesla has them walking around the factories now, mostly doing simple tasks like moving battery cells. Is it a product? Or is it a distraction? If Tesla can actually sell a functional humanoid robot to other factories in 2026, all the car delivery metrics won't even matter.

Actionable Insights for Investors

So, where does that leave you?

If you're holding Tesla stock, or thinking about jumping in, you've got to decide which narrative you believe. Are you buying a car company or an AI lab?

Watch the Energy Storage margins. If the automotive side continues to struggle, the Megapack growth needs to accelerate to pick up the slack. A 50% growth rate in energy is great, but 100% would be a game-changer.

🔗 Read more: Bitcoin Value in 2012: The Year Nobody Cared and Everyone Should Have

Keep an eye on the 10-billion-mile mark. Elon says that’s the magic number for FSD. We’re at 7.2 billion now. At the current rate of data collection, they should hit that milestone sometime in late 2026. If FSD doesn't become "unsupervised" by then, the "AI company" narrative might start to fray.

Mind the technicals. As of mid-January 2026, the stock is trading below its 10-day and 50-day moving averages. It’s consolidating. A break above $492 would be a massive bullish signal, but a slide below $415 could see it testing the 200-day average down at $363.

Don't bet more than you can afford to lose. Tesla is a high-beta stock for a reason. It moves fast, it breaks things, and it rarely does what the "experts" expect.

Next Steps for Your Portfolio:

- Check your exposure: Ensure Tesla doesn't represent more than 5-10% of your total portfolio unless you have a very high risk tolerance.

- Monitor Q4 earnings: The official 2025 financial results drop on January 28, 2026. Watch for the specific "Auto Gross Margin" figure—anything below 15% will likely trigger a sell-off.

- Audit the Energy Segment: Look for updates on the Lathrop Megafactory's throughput. If they can't scale production to meet the 15 GWh contracts (like the Intersect Power deal), the growth story hits a wall.